The S&P 500 closed Friday at 7,575.39, up 1.2% on the week, while the Nasdaq rose 1.7% last week. The dominant story was a sharp re-escalation of the war between the US and Iran. Trump declared the ceasefire "over" on Wednesday after Iranian strikes on commercial vessels in the Strait of Hormuz, and the US carried out fresh airstrikes Wednesday night and again on Thursday, with Iran retaliating against US-allied Gulf states. The price of Brent crude oil spiked as high as $78.19 per barrel before easing back toward $76.01 by Friday (chart).

Semiconductor stocks whipsawed all week. Samsung's record 19-fold y/y profit jump last quarter, reported on Tuesday, still missed elevated Wall Street expectations. Micron's $250 billion US investment pledge sparked a sharp Thursday rebound. SK Hynix made a $26.5 billion Nasdaq debut on Friday, the largest-ever US listing by a foreign company; its stock rose 13% that day.

The calendar is unusually crowded this week. Q2 bank earnings kick off Tuesday with JPMorgan, Bank of America, Citigroup, and Wells Fargo. Fedspeak is constant: Waller (Mon), Goolsbee (Tue), Williams and Musalem (Wed), Logan and Jefferson (Thu) all appear, while new Fed Chair Kevin Warsh delivers his first Humphrey-Hawkins testimony on Tuesday and Wednesday. All this happens against the backdrop of June's FOMC minutes, which showed nine of 18 officials now penciling in at least one Fed rate hike this year.

Internationally, Tuesday brings a full slate out of Beijing (Q2 GDP, industrial production, retail sales, and the urban unemployment rate), with the consensus looking for GDP growth to slow to around 4.4%-4.7% y/y from Q1's 5.0%, while the Bank of Canada meets Wednesday and is widely expected to hold at 2.25% for a sixth straight meeting.

With that said, here are the key economic releases most likely to shape investors' thinking this week:

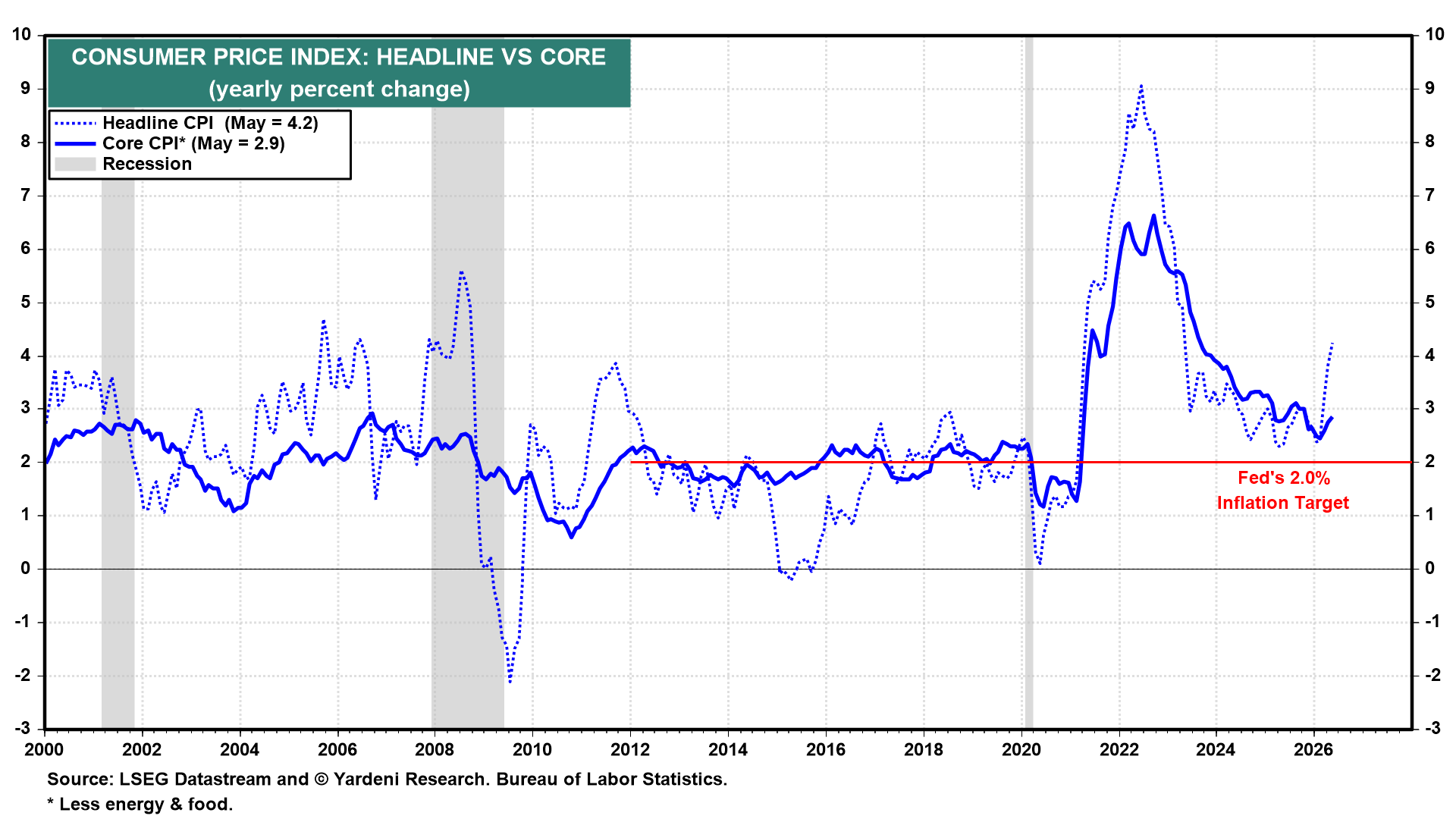

(1) Inflation. June's CPI (Tue) follows a hot May print, with headline and core inflation rates at 4.2% y/y and 2.9% (chart). The Cleveland Fed's Inflation Nowcasting projects June's comparable rates at 3.9% and 2.9%. The projected m/m rates are 0.0% and 0.2%.

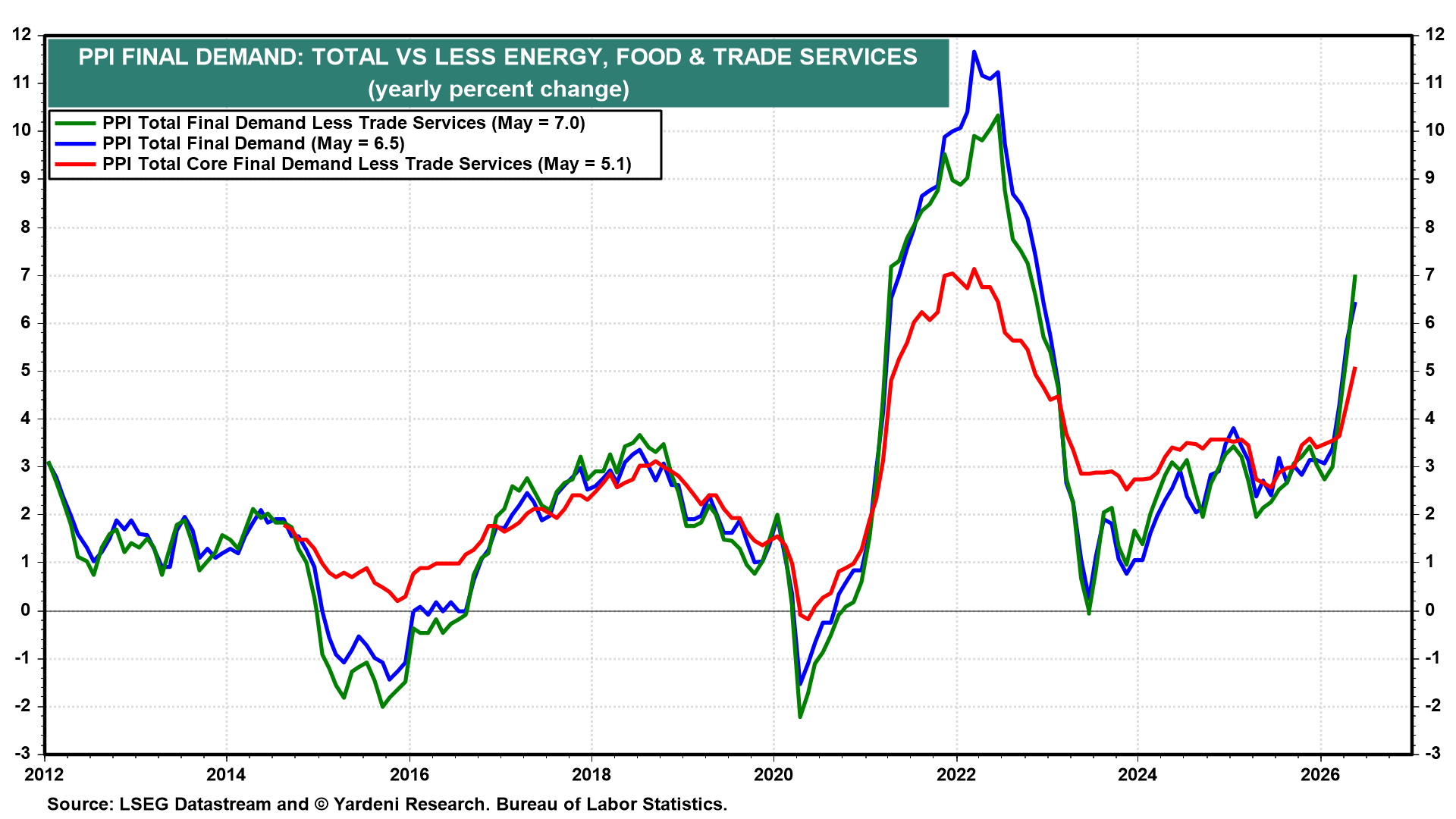

June's PPI (Wed) follows an elevated May reading of 6.5% y/y, the fastest pace since November 2022 (chart). The rapid drop in oil prices last month should show up in lower PPI inflation.

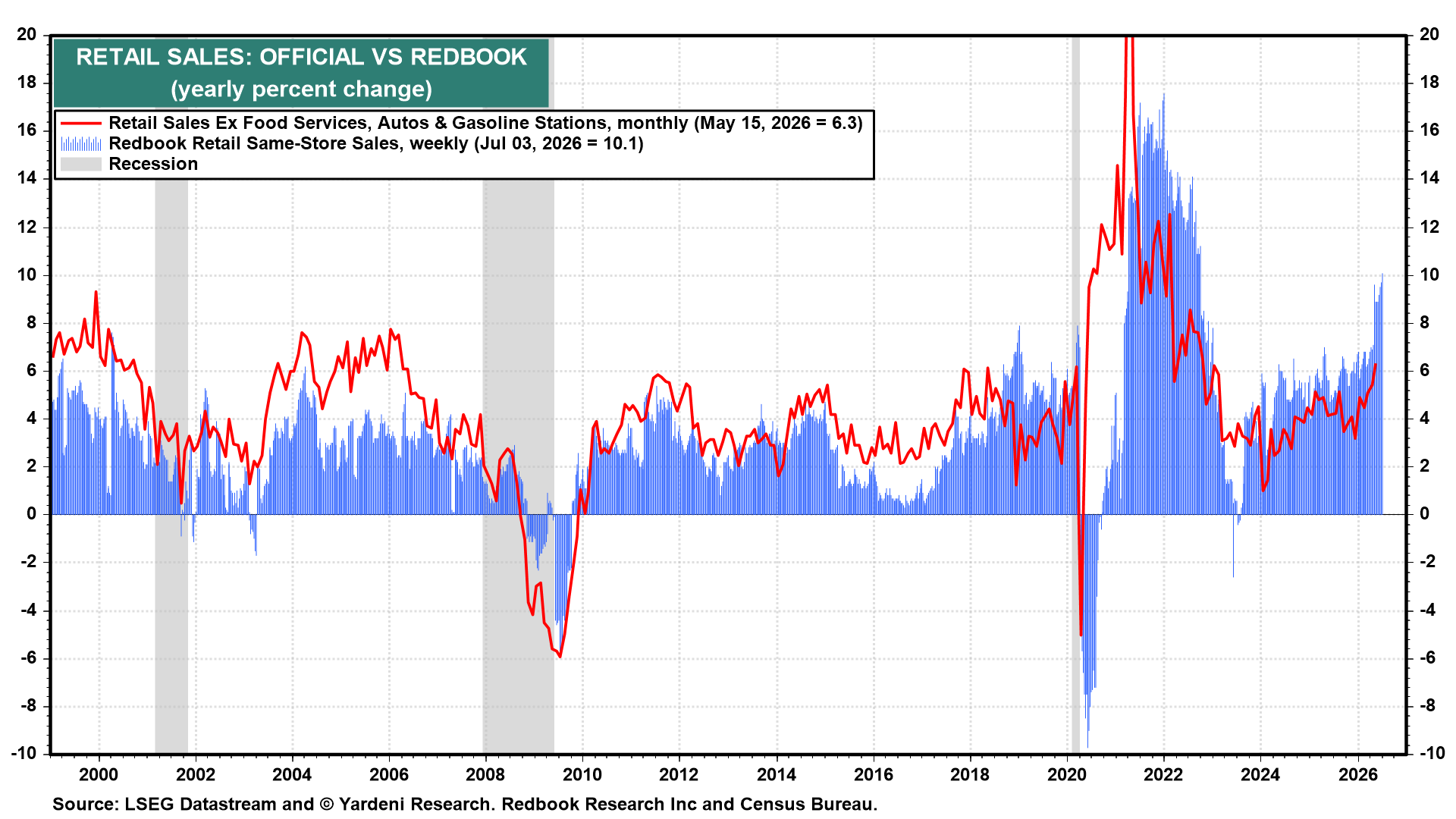

(2) Retail Sales. June's report (Thu) follows a strong May, when advance sales rose 0.9% m/m and 6.9% y/y (chart). The weekly Redbook same-store sales index has been running even hotter, rising to 10.1% y/y for the week of July 3, a multi-year high, confirming that consumer spending has stayed robust even as headline jobs growth has slowed recently.

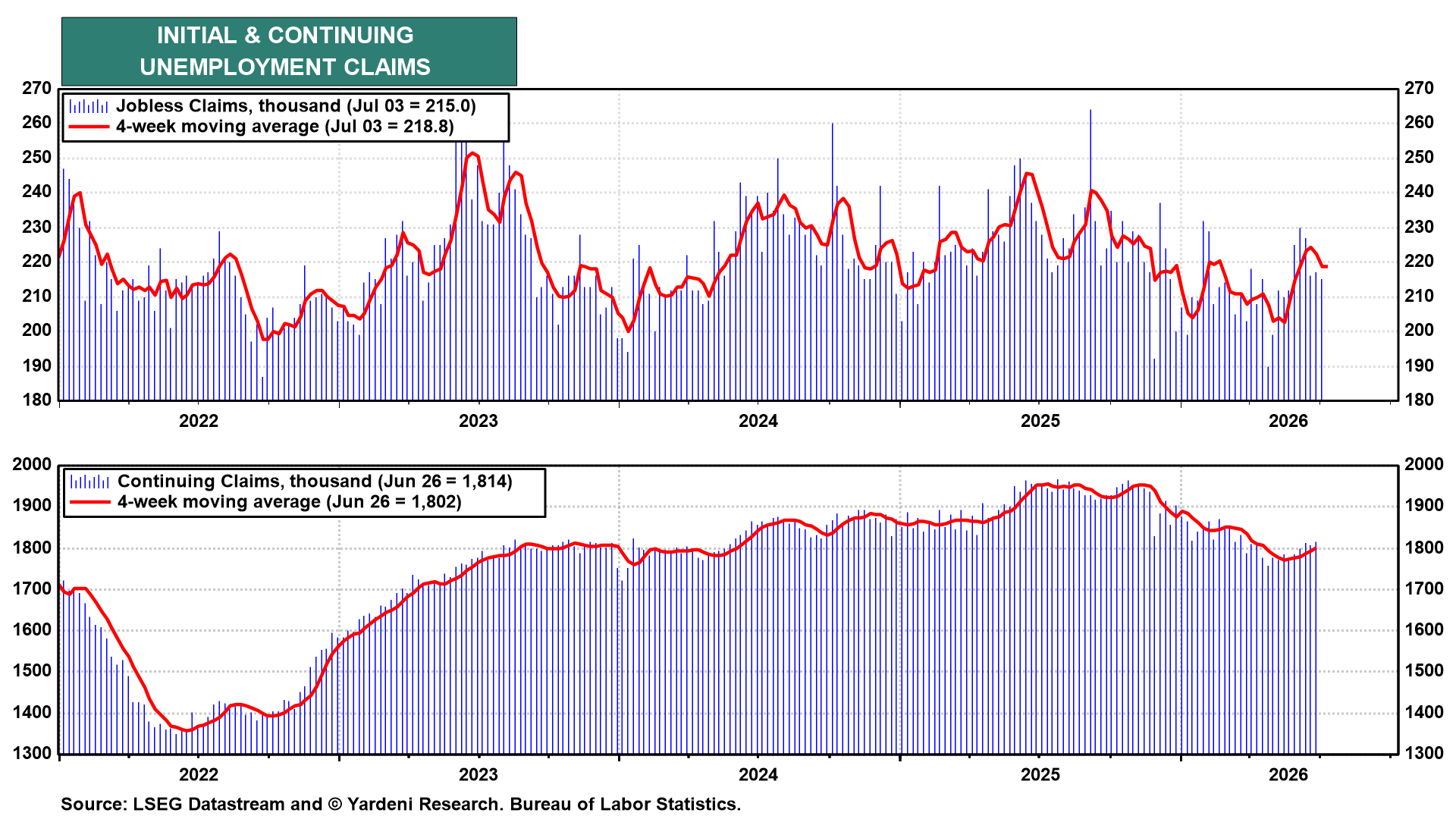

(3) Employment. Initial unemployment insurance claims for the week of July 4 fell to 215,000, with the 4-week average trending down to 218,750, both still consistent with low layoffs.

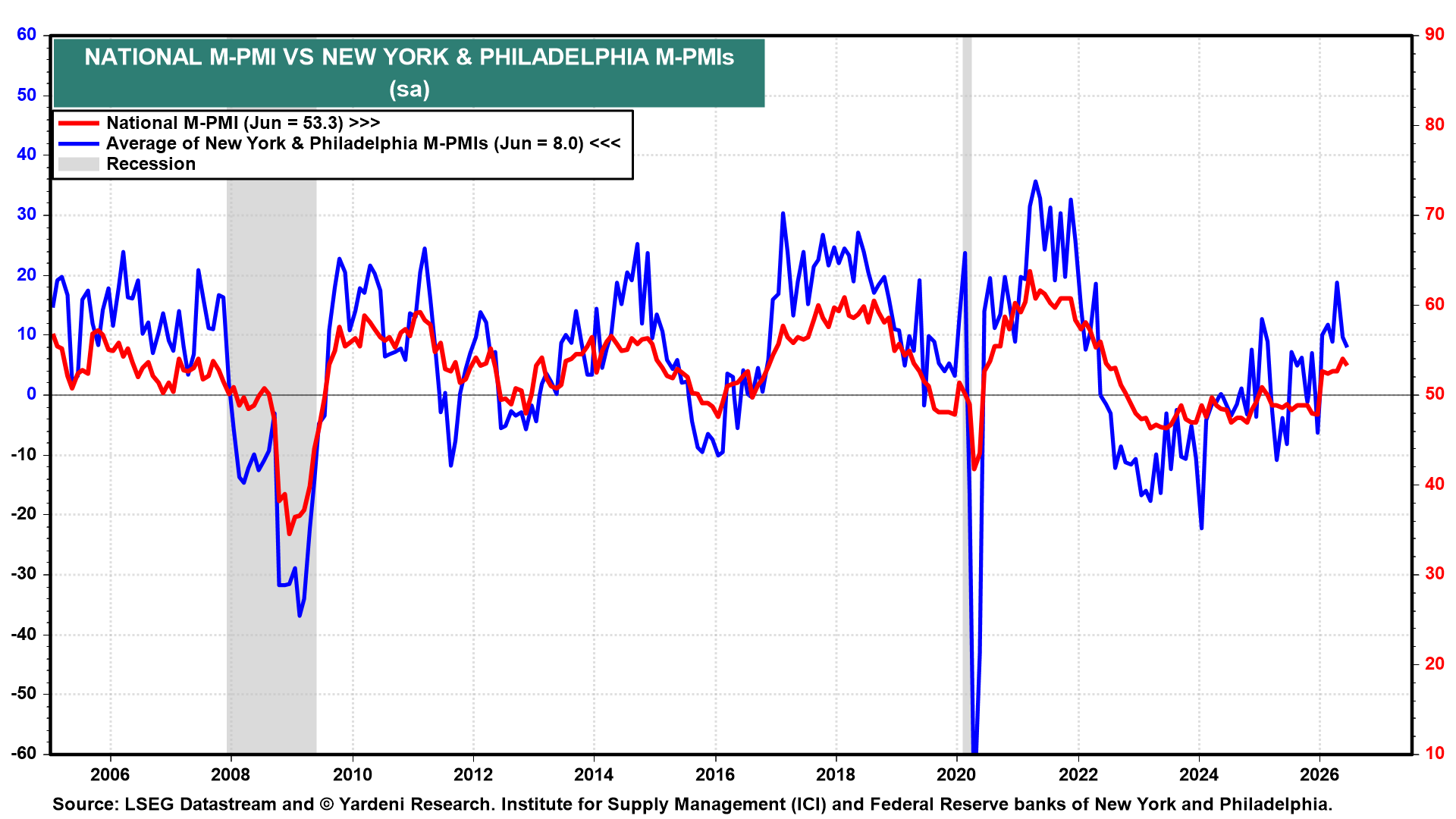

(4) Manufacturing. July's regional business surveys conducted by the NY (Wed) and Philly (Thu) Feds should confirm that business activity is still expanding (chart).

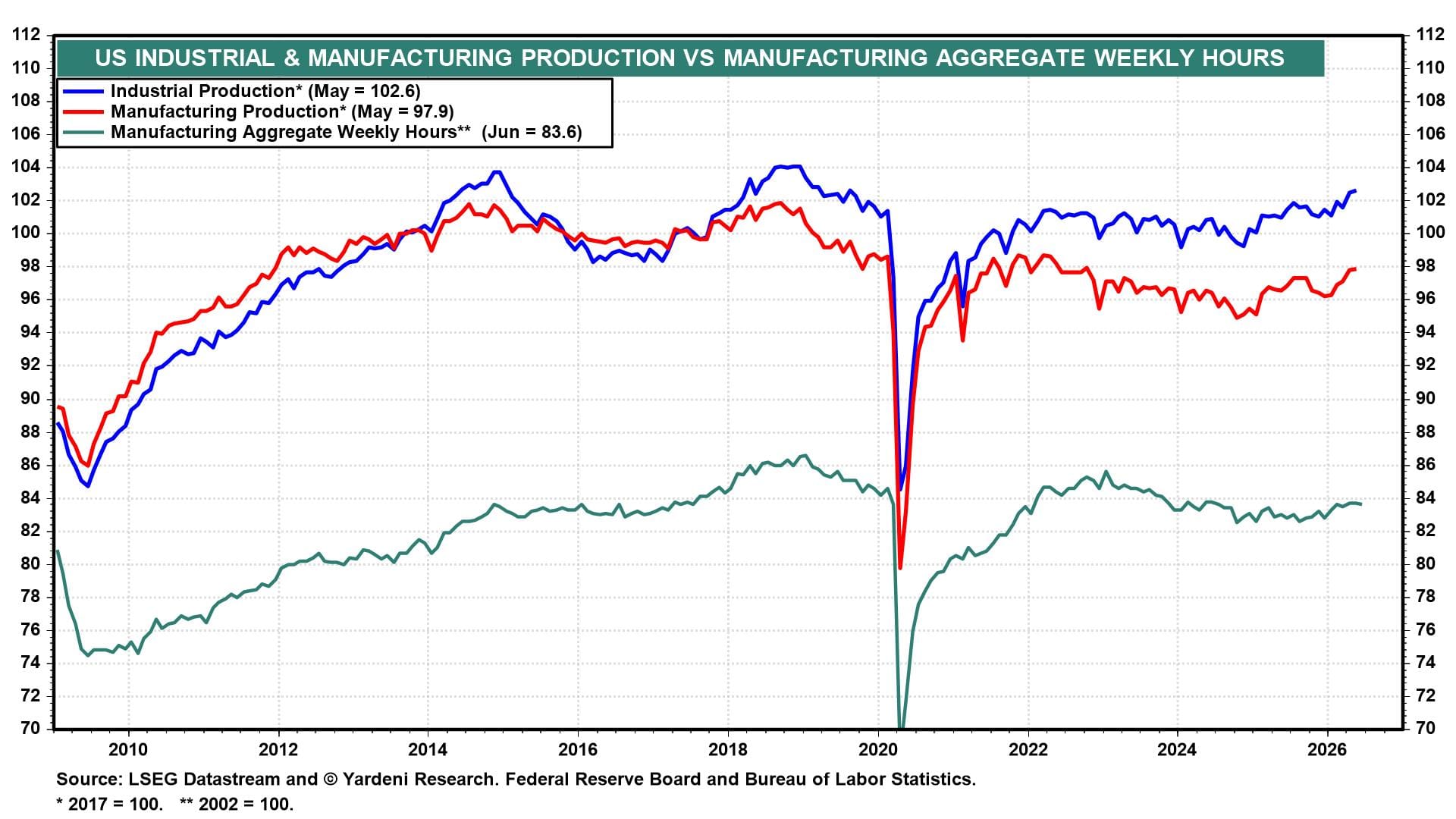

(5) Industrial Production. June's industrial production (Fri) should show a modest uptick, though manufacturing aggregate weekly hours edged down during the month (chart).