I. Sentiment

The S&P 500 first rose above 7,500 on May 14. It has continued to fluctuate around there since then. This may be a sign that investors are a bit fatigued from all the commotion about the Strait of Hormuz, AI, earnings, Warsh, the Magnificent-7, semiconductors, FOMO, and FEMO so far this year. The market might continue to fluctuate around 7,500 over the rest of the summer as more market participants head off to the beach for a rest.

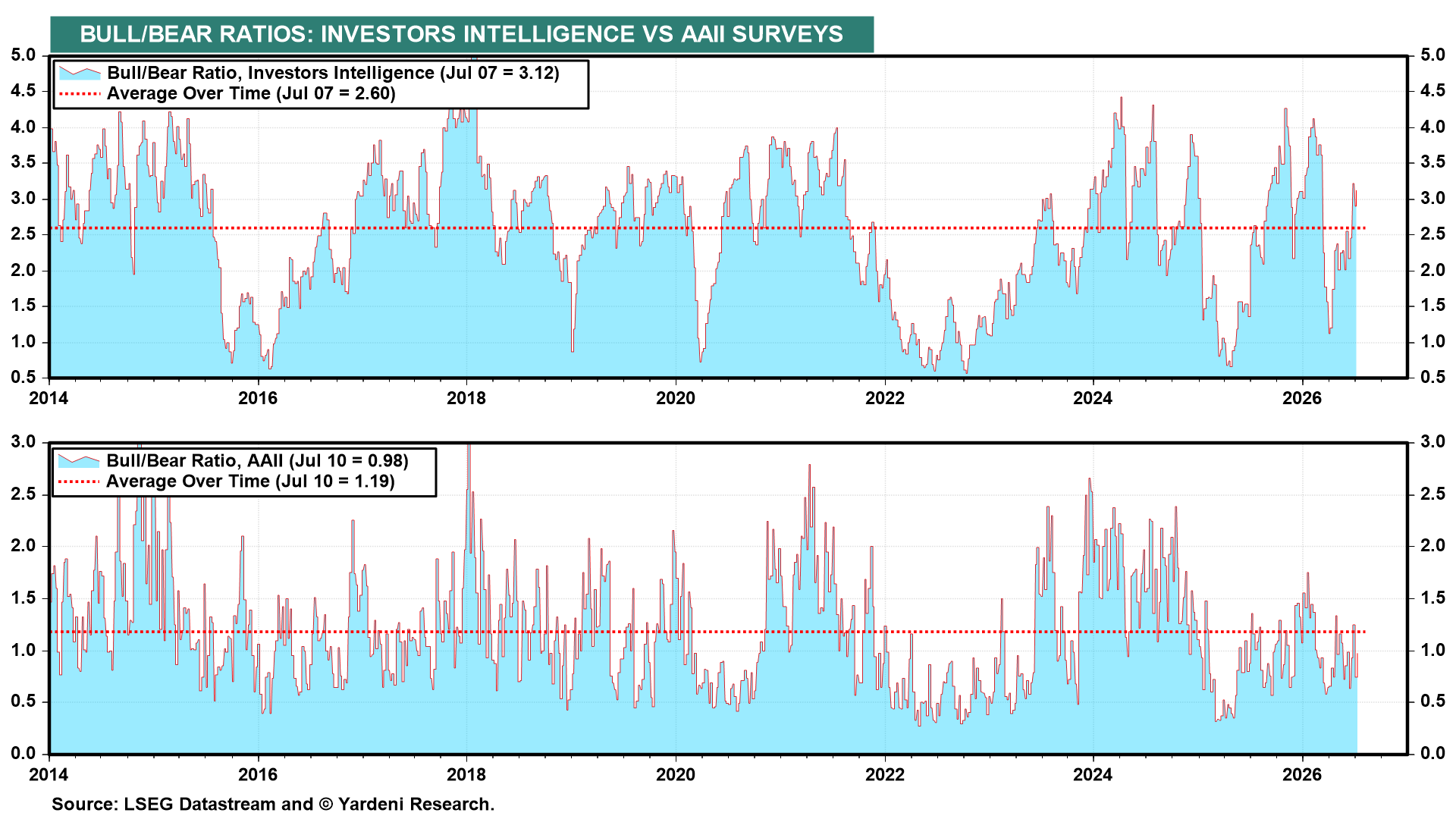

The bull-bear ratios we track show that sentiment is neither too bullish (which would be bearish) nor too bearish (which would be bullish) (chart). Ho-hum.

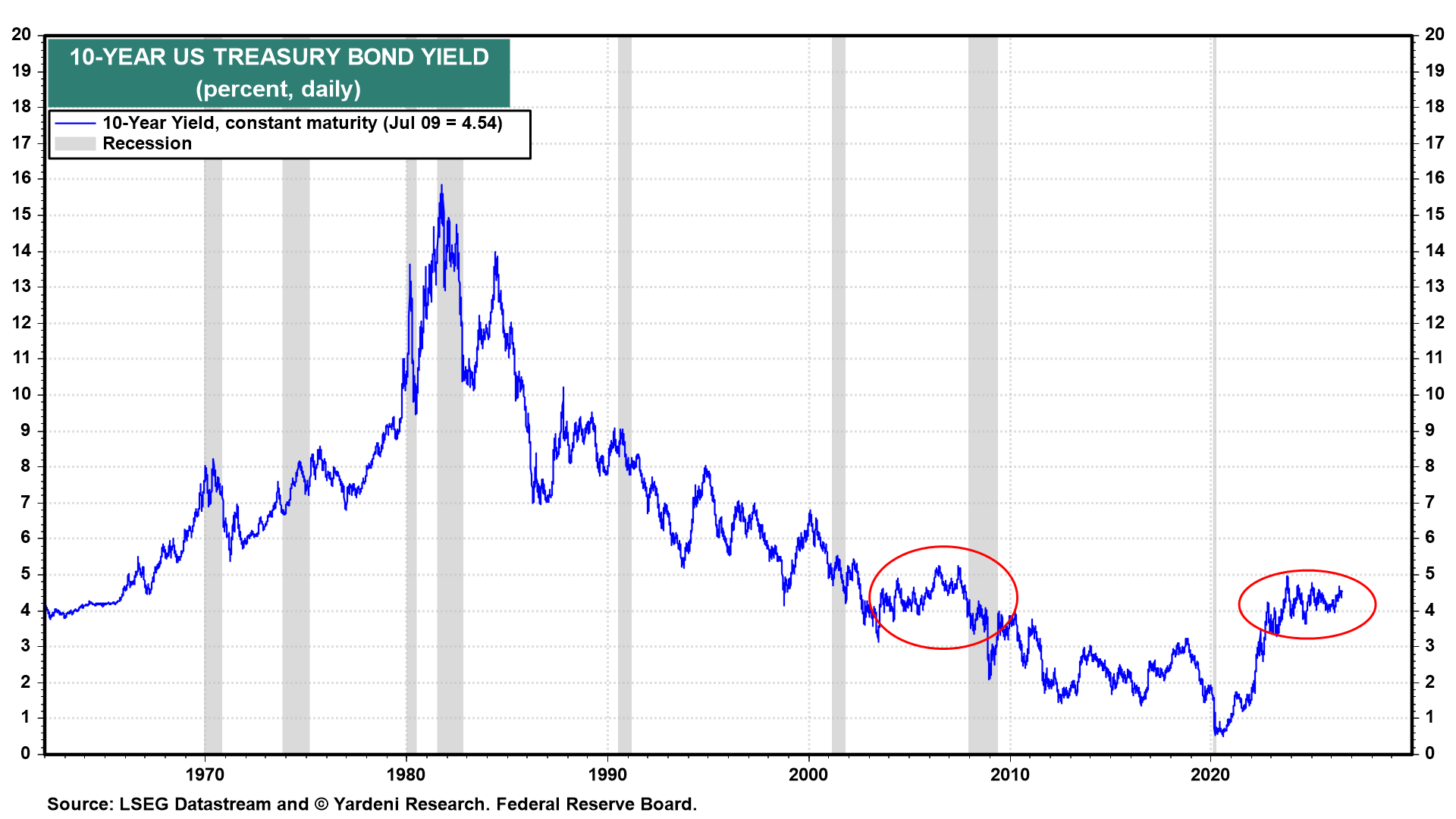

By the way, the 10-year Treasury bond yield has been range-bound since mid-2023 between roughly 4.00% and 5.00%, as we've been projecting (chart). For now, we expect more of the same through next year.

II. The Fed

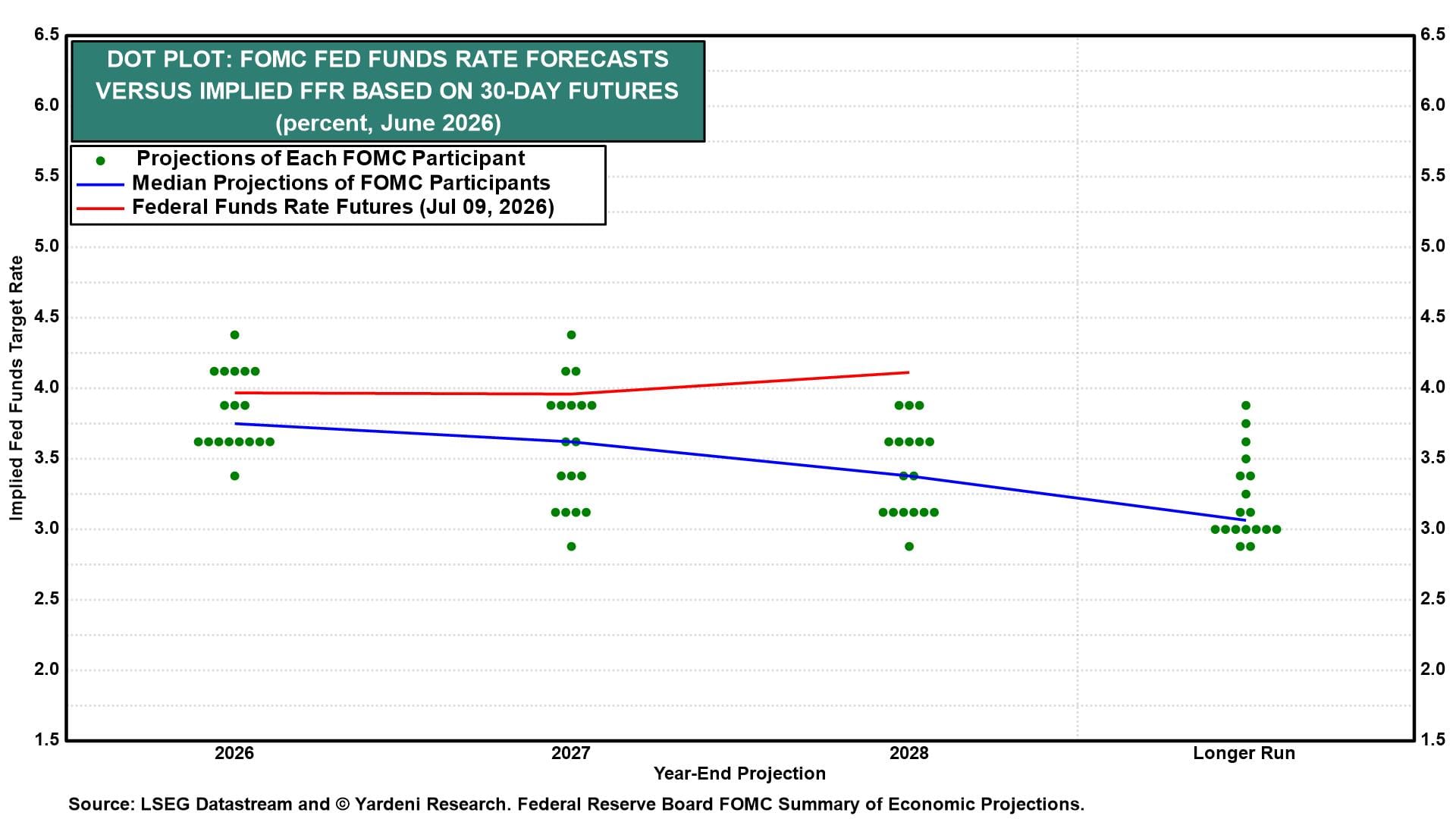

Back in May, we anticipated that the FOMC would pivot from April's easing bias to a tightening bias at the June meeting of the Fed's policy-setting committee. Sure enough, June's Dot Plot reflected that shift, with the median participant projecting no federal funds rate (FFR) cuts this year and nine officials penciling in one or two hikes (chart). Even Fed Chair Kevin Warsh was hawkish at his press conference after the latest meeting, though he chose to be dotless.

The June FOMC meeting minutes, released yesterday, underscore just how hawkish that meeting was, and the recent economic data confirm that the Fed has no reason to remove its tightening bias.

Here's more:

(1) The Pivot. The committee shifted from debating eventual easing to whether additional tightening might be necessary. Indeed, a few FOMC participants explicitly argued for raising rates in June, while many others indicated the appropriate FFR by year-end would be above the current 3.50%-3.75% target range.

(2) Labor market. Most importantly, policymakers concluded that downside risks to maximum employment had moderated, allowing greater focus on inflation risks.

(3) Economic growth. The minutes describe an economy expanding at a solid pace, with real final sales to private domestic purchasers likely to accelerate in Q2-2026 and to grow faster than GDP. Participants expected solid consumer spending and strong business investment (led by the AI buildout) to support growth through year-end.

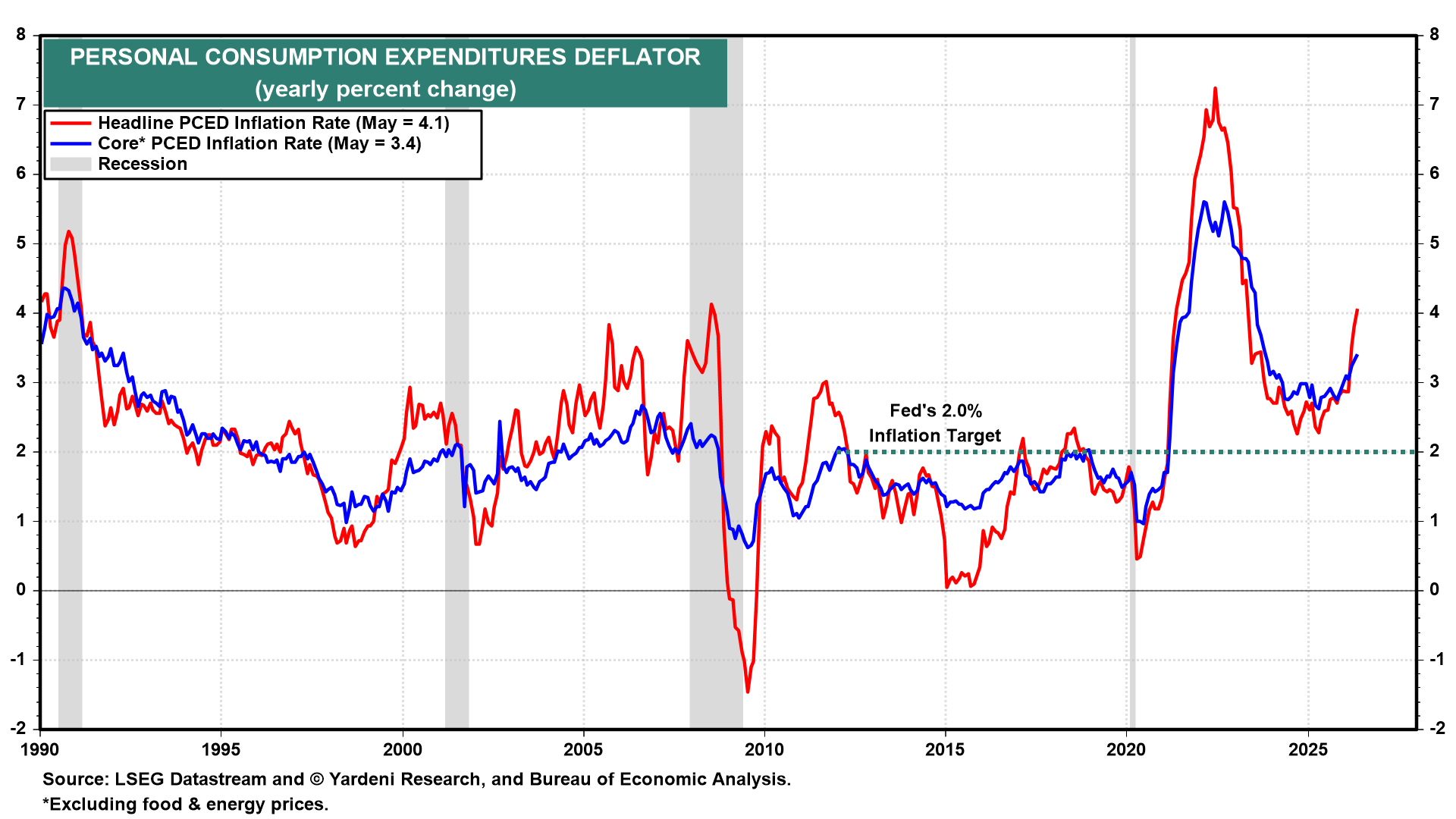

(4) Inflation. Headline and core PCED inflation rates rose to 4.1% and 3.4% in May, well above the Fed's 2.0% target (chart). Participants attributed persistent inflation to tariffs, AI-driven demand, and Middle East-related supply disruptions, noting that price pressures had become increasingly broad-based. After more than five years of above-target inflation, further overshoots remained "a salient risk," and risks to the inflation outlook "were still tilted to the upside."

(5) Policy stance. Several participants did not view the current policy stance as restrictive, which helps explain why a few already saw a case for raising rates at the June meeting.

(6) AI assessment. AI was mentioned 21 times in the minutes, up from eight in April, and the context was overwhelmingly hawkish. Participants noted AI continues to drive investment in data centers and high-tech equipment with no sign of slowing. Many also noted that strong AI-related demand will keep upward pressure on technology and electricity prices. In short, the minutes suggest the Fed shares our view that AI is boosting economic growth, bolstering labor market conditions, adding to inflationary pressures, and raising the neutral rate of interest.

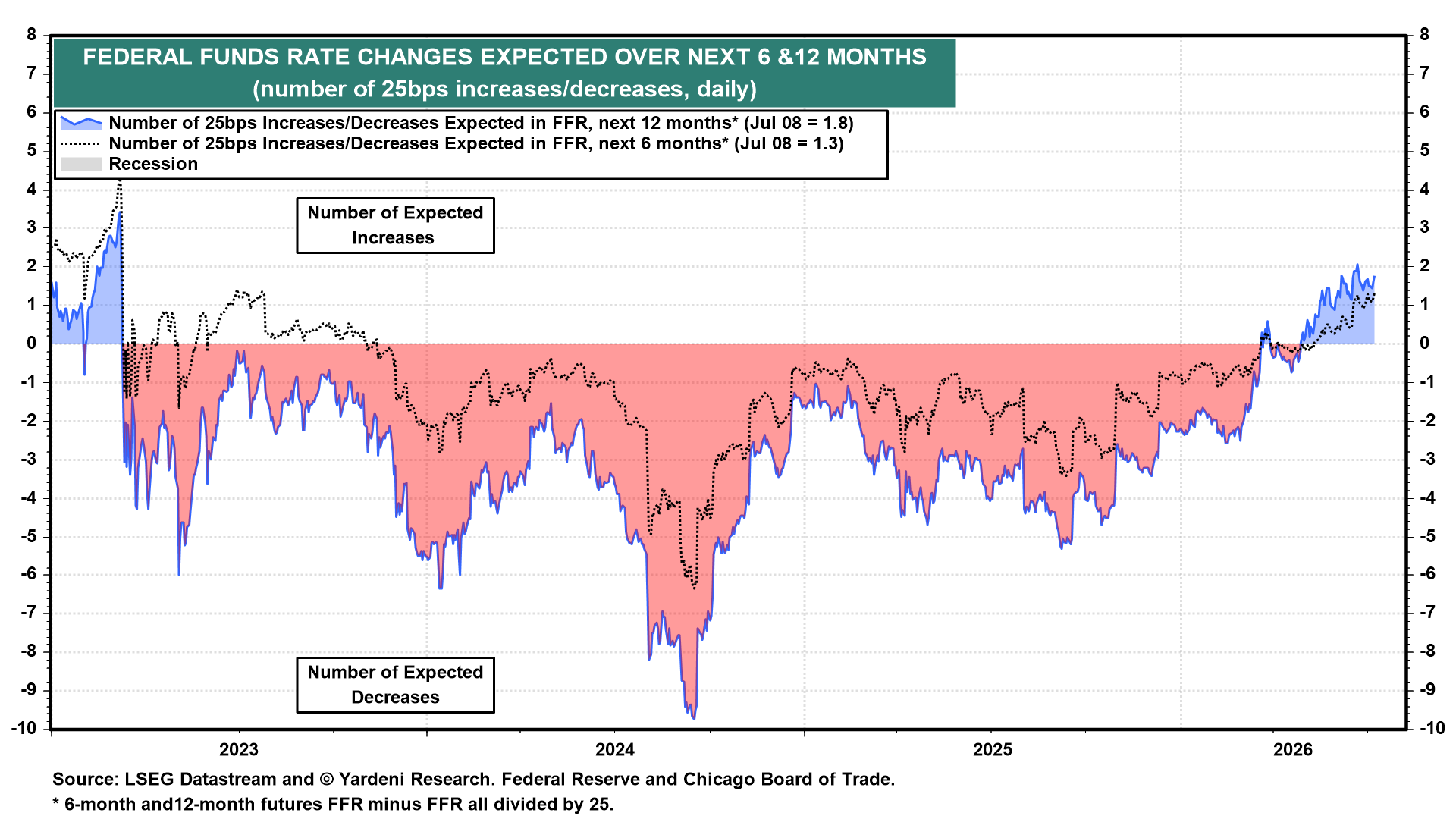

(7) Bottom line. Upside risks to inflation continue to outweigh downside risks to employment, and inflation risks extend well beyond oil prices. That explains why, despite a sharp decline in oil prices, FFR futures continue to signal one to two FFR hikes over the next 12 months (chart).

III. Consumer Credit

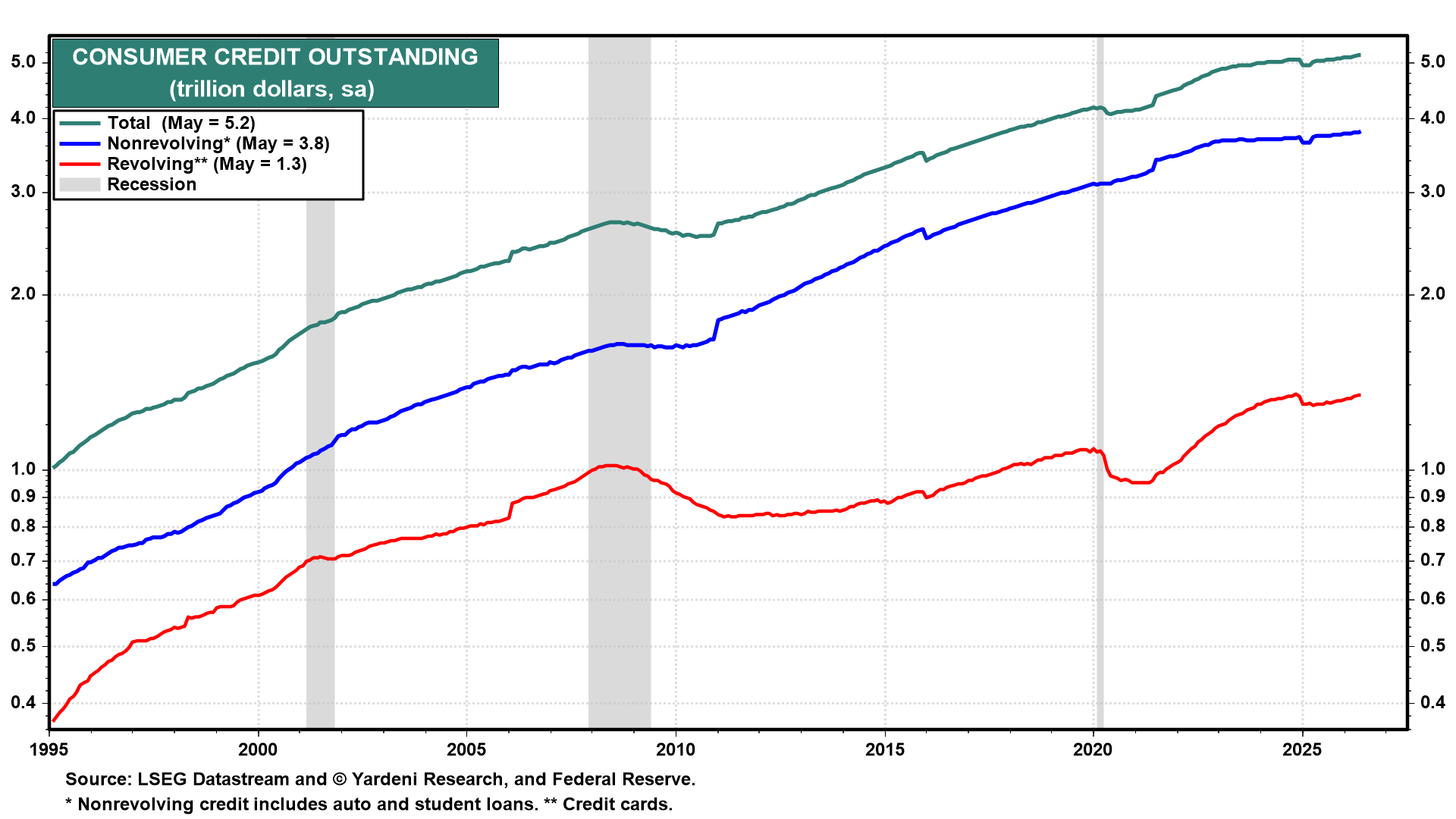

Total consumer credit rose 2.1% y/y in May to a record $5.2 trillion (chart). Revolving credit rose 3.4% y/y and nonrevolving credit rose 1.6% y/y.

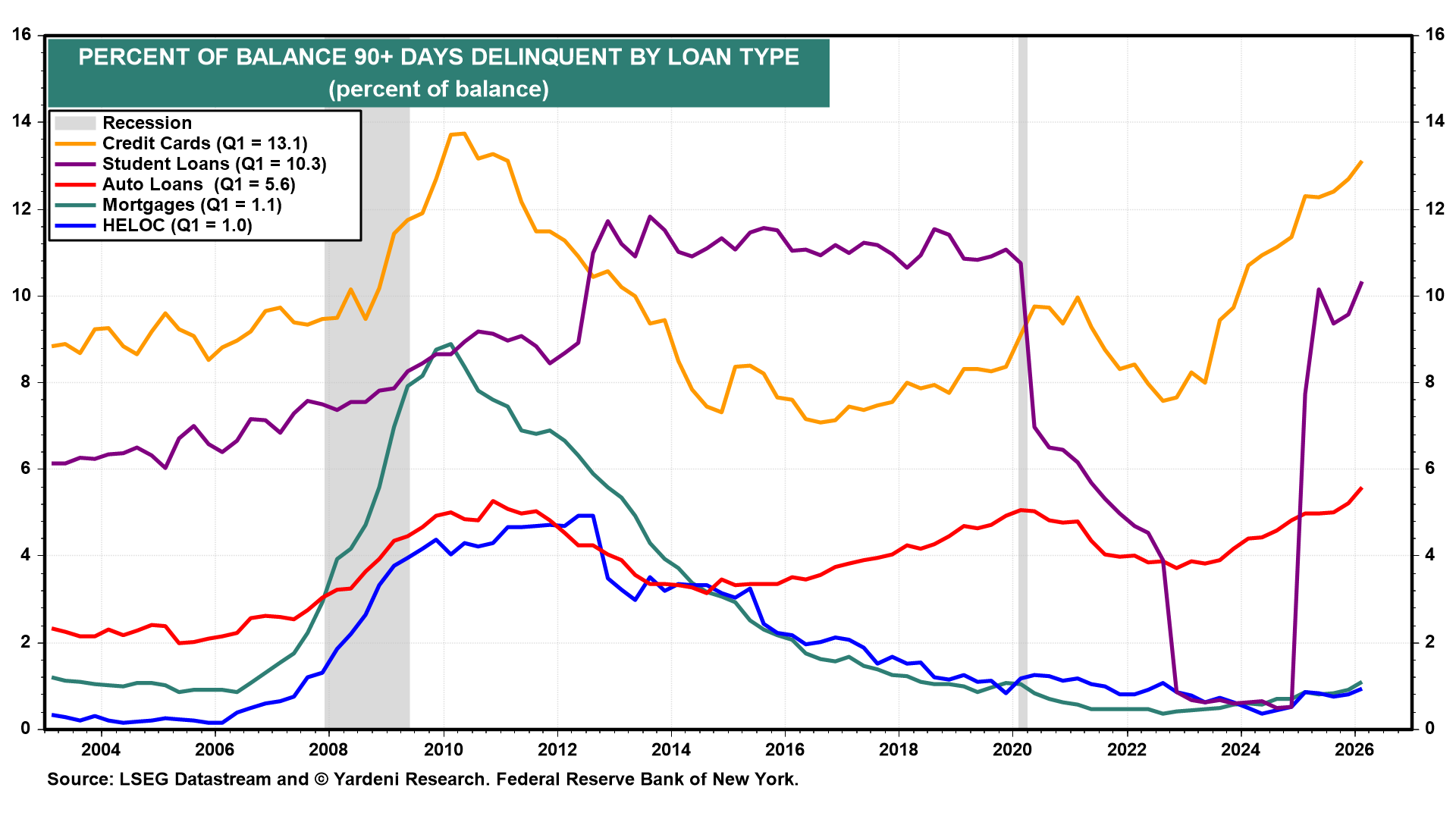

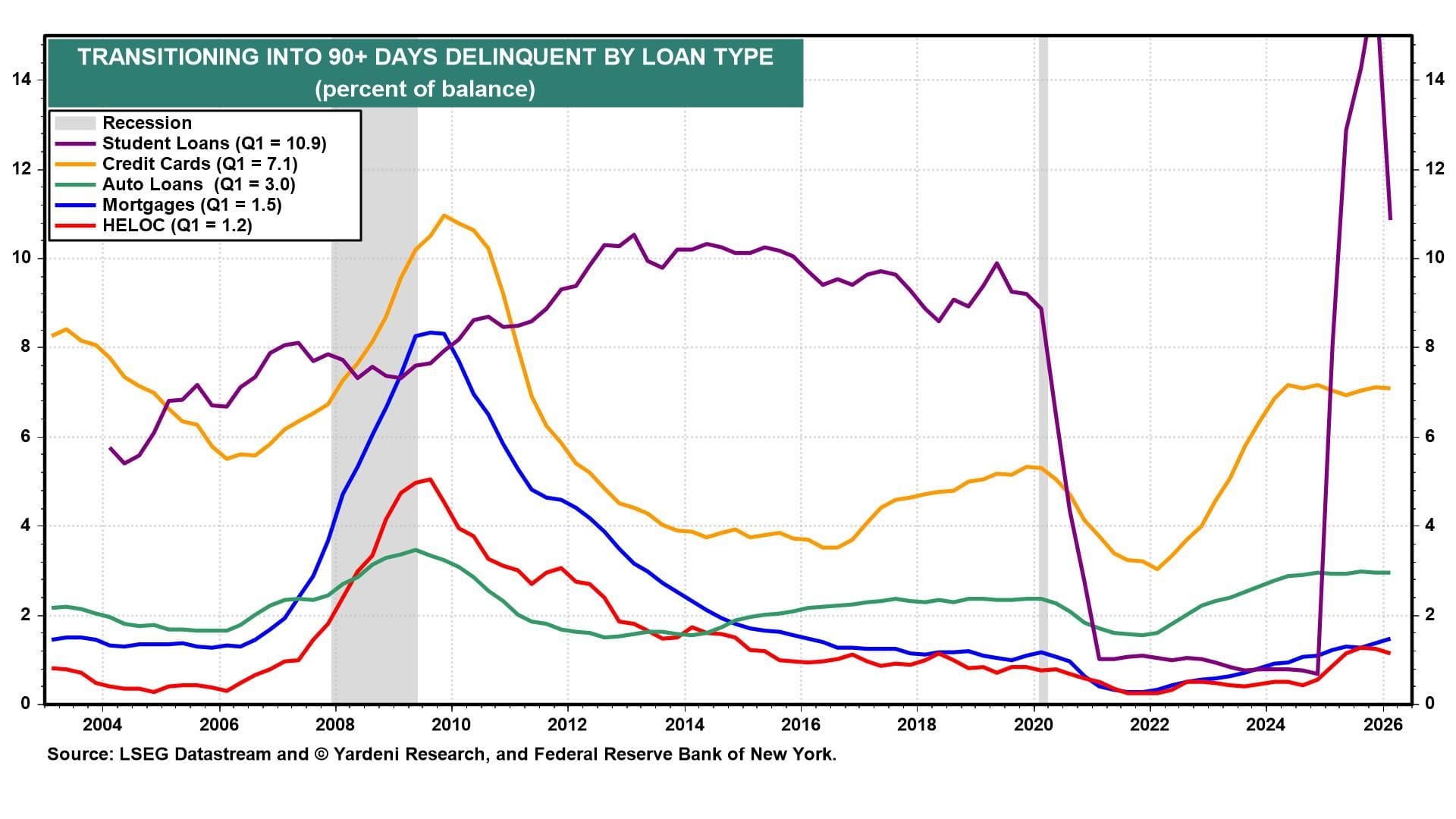

The New York Fed’s Household Debt and Credit Report shows 90-plus-day credit card delinquencies at 13.1% in Q1-2026, near the 13.7% peak during Q2-2010, when the Great Financial Crisis (GFC) was still weighing on consumers (chart).

That isn't as alarming as it seems, according to our colleague Jackie Doherty. The NY Fed measure includes balances banks have already charged off, inflating the the delinquency rate. The 90-day delinquency transition rate for credit cards, which captures balances newly entering serious delinquency, has been stable around 7.0% since 2023 and well below GFC levels (chart).

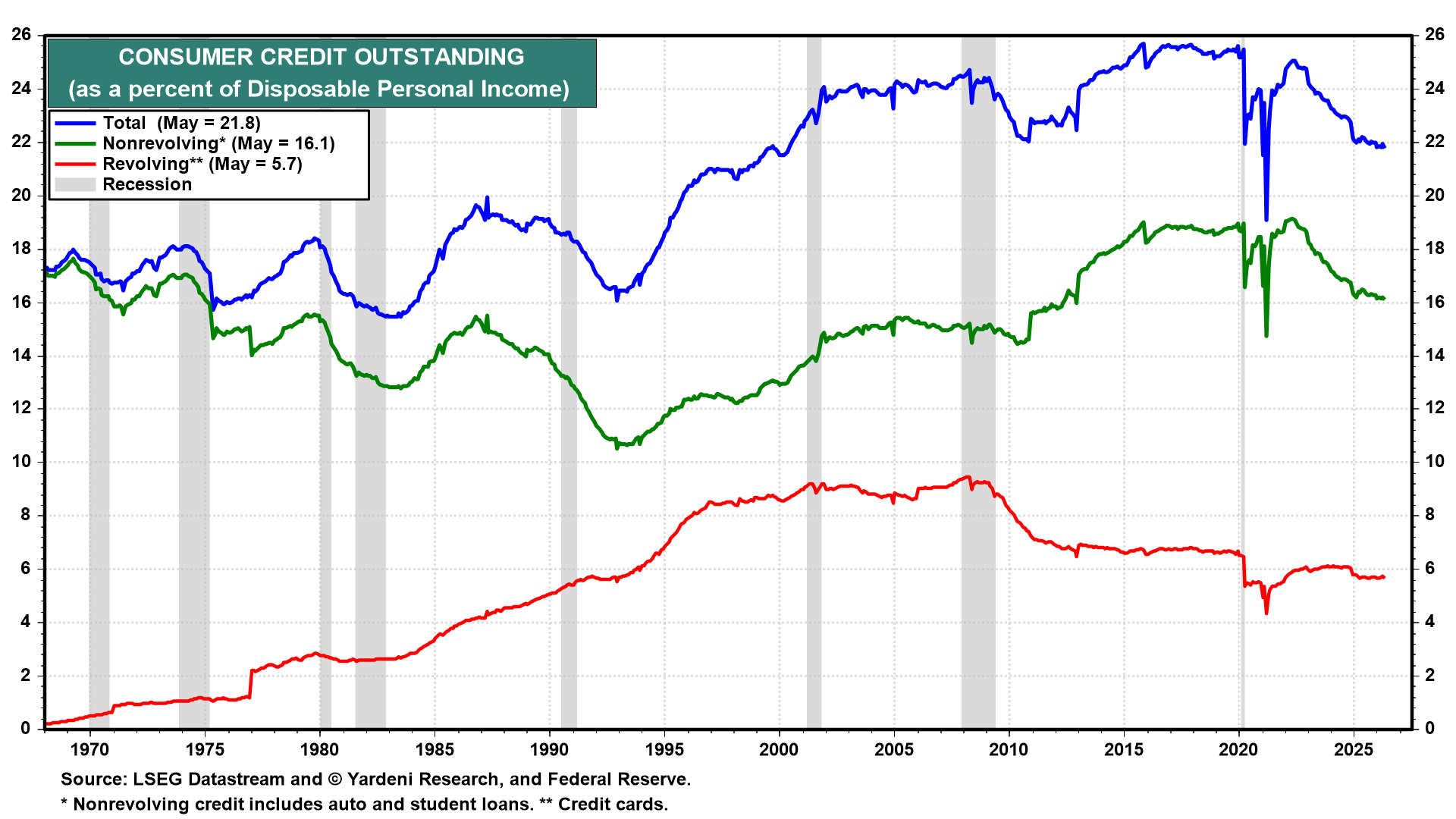

Relative to disposable personal income, credit usage remains measured and broadly in a downward trend (chart).