Today, the US launched Project Freedom, deploying 15,000 service members and over 100 aircraft to escort stranded commercial vessels through the Strait of Hormuz. The first two US-flagged merchant tankers were successfully escorted this morning. However, Iran struck the UAE's Fujairah energy hub and a UAE oil tanker and damaged residential areas in Oman. US forces destroyed six Iranian small boats and intercepted multiple missiles and drones. Tehran claimed to have struck a US warship, a claim the Pentagon flatly dismissed.

Diplomatically, the two sides remain deadlocked. Trump rejected Iran's latest 14-point peace proposal, which sought an end to the blockade of Iran's ports in exchange for reopening the Strait.

Four scenarios are now in play. There could be a prolonged stalemate, with the Strait remaining closed, while the US blockades Iran's ports. That could lead to a second scenario in which the two sides negotiate a deal. That's not very likely given the intransigence on both sides about whether Iran should be allowed to keep its nuclear program. The third alternative is that US forces open the Strait militarily, while continuing to blockade Iran. This could quickly lead to a fourth scenario in which a full-scale war restarts, causing much more damage to energy infrastructure around the Persian Gulf and resumed oil-price climbs.

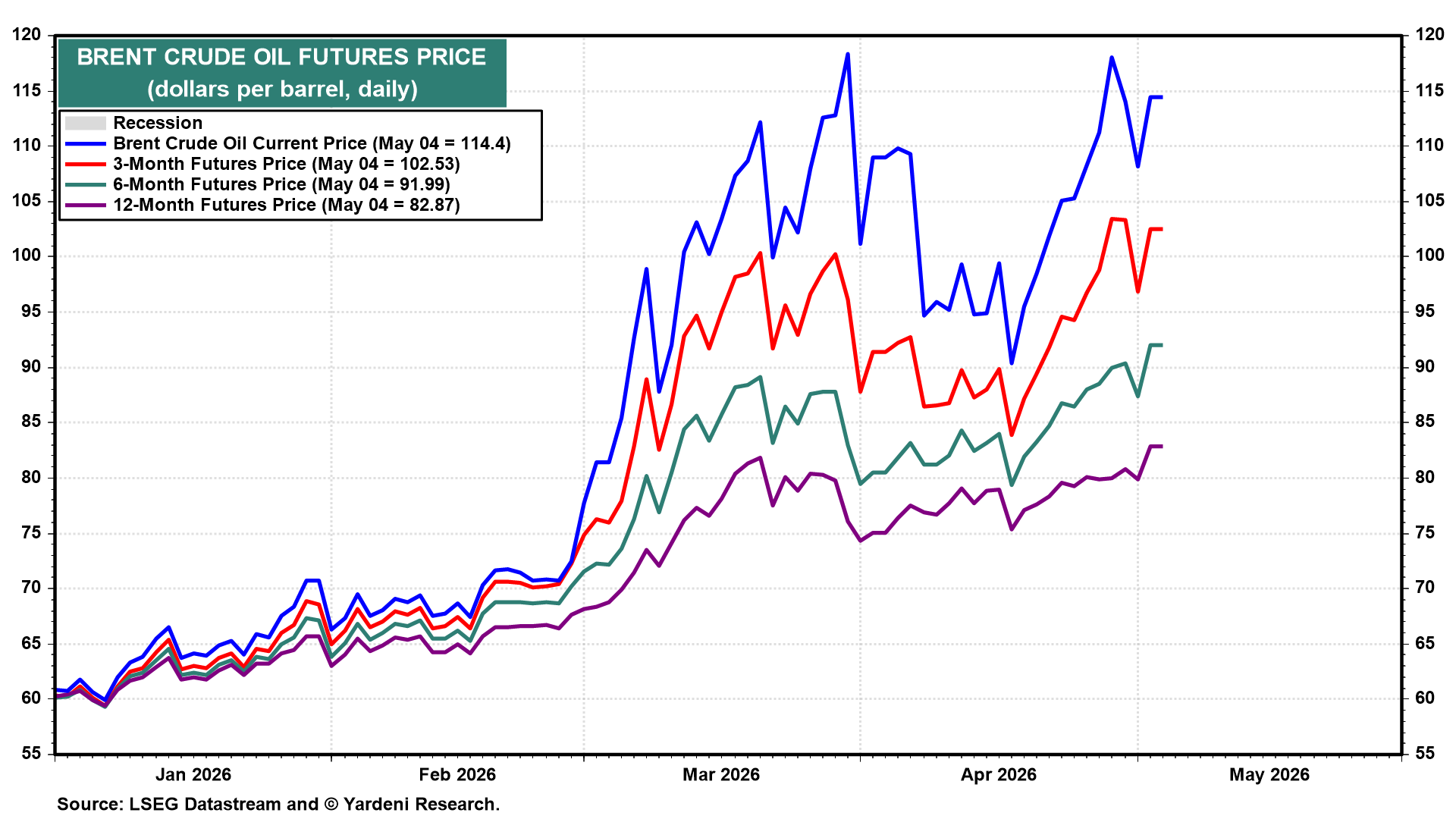

The launch of Project Freedom sent the price of Brent crude as high as $114 a barrel today (chart). That weighed on both the stock and bond markets today.

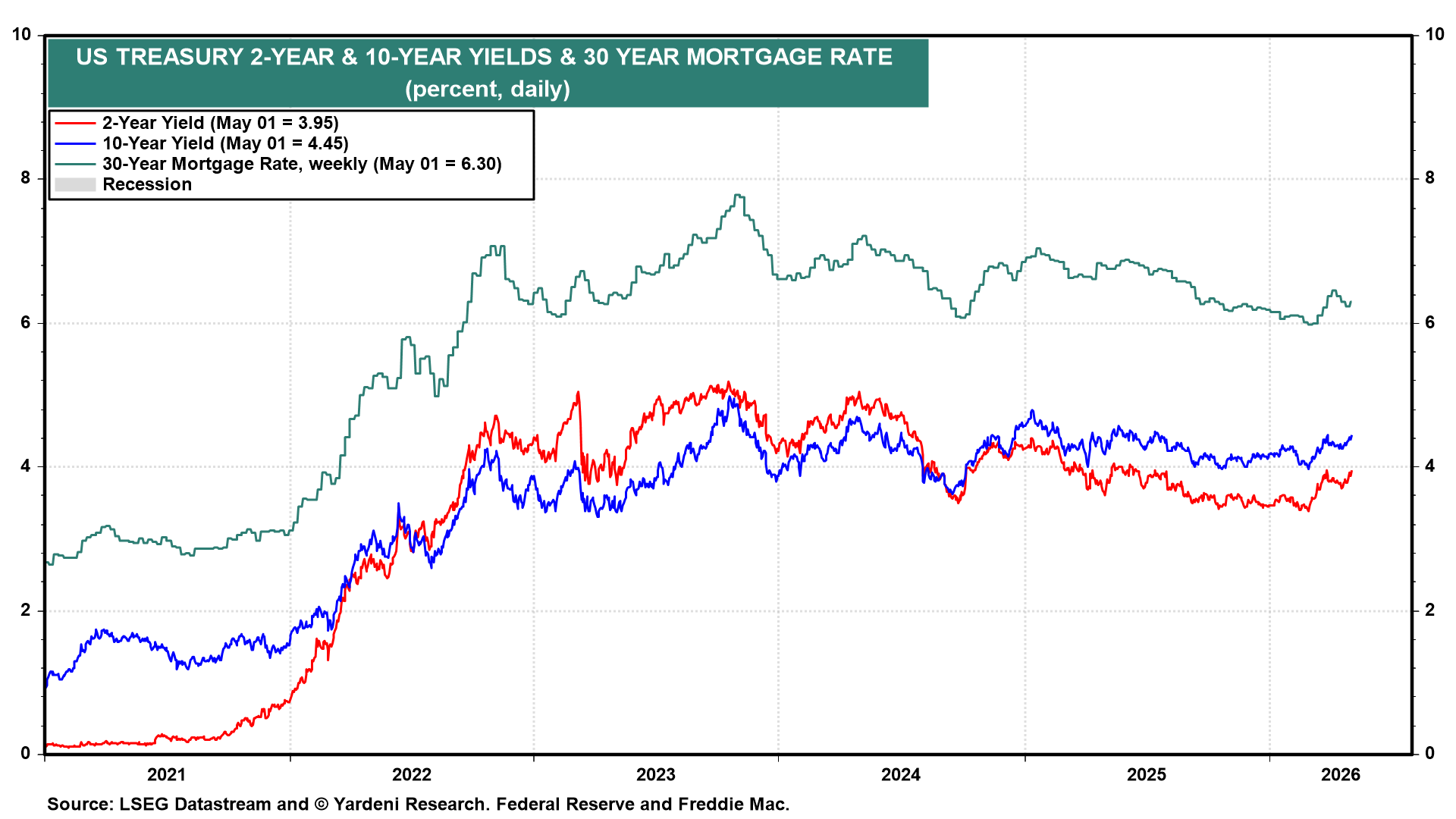

US Treasury yields and mortgage rates have been rising amid the jump in oil prices since the start of the war (chart).

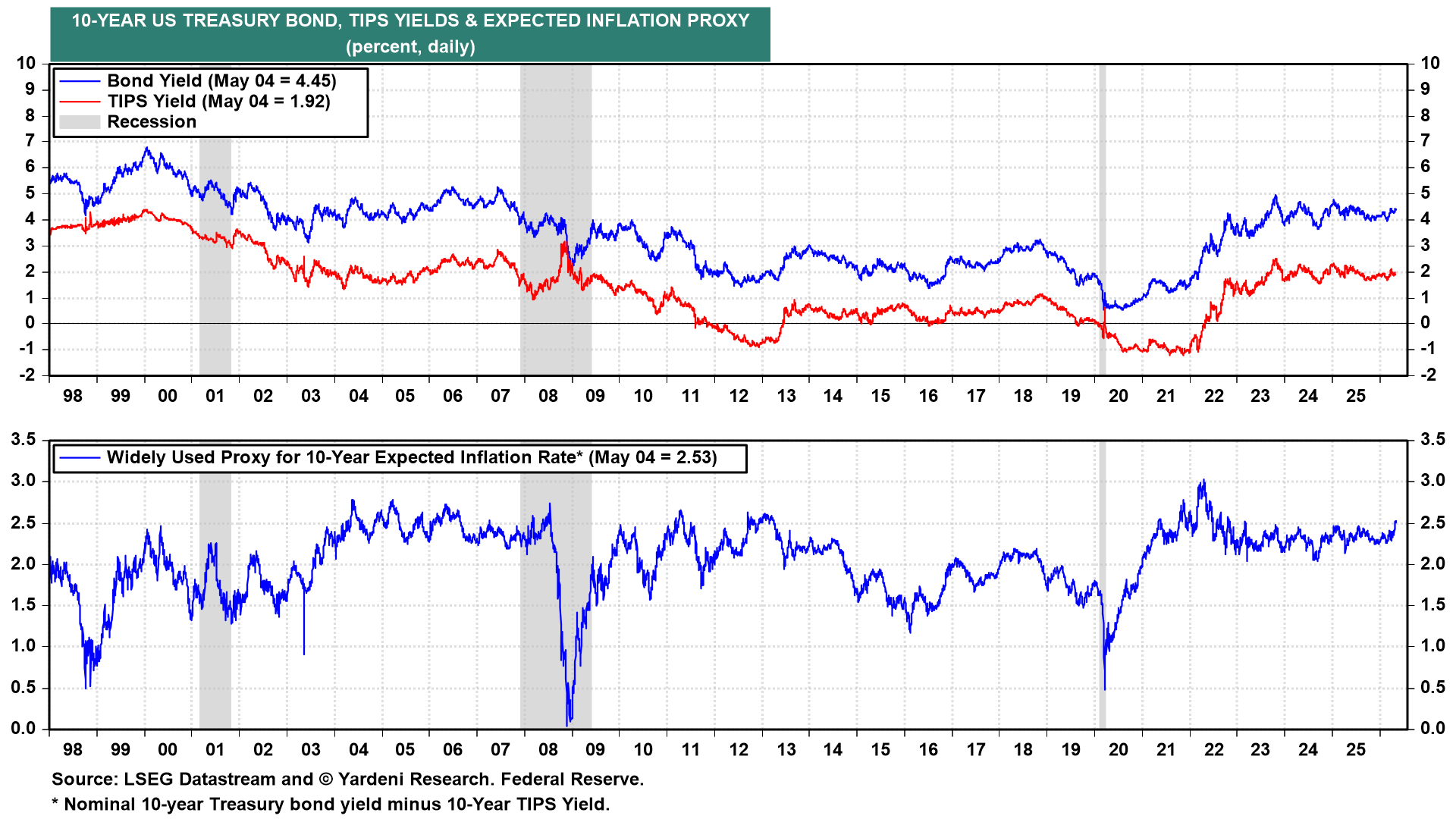

The nominal 10-year Treasury bond yield has been pushed higher by the expected inflation rate embedded in the spread between it and the 10-year TIPS yield (chart).

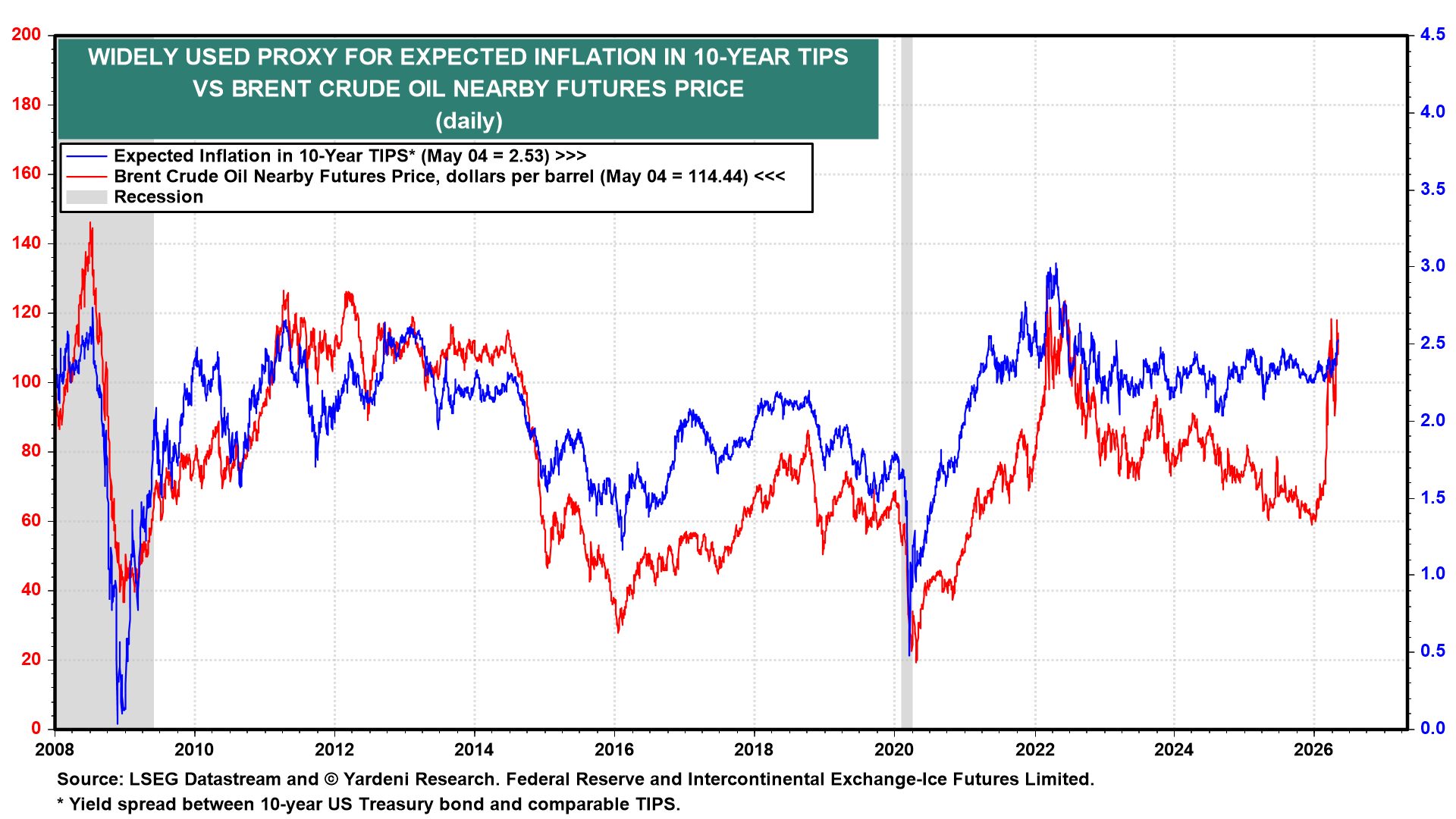

Not surprisingly, the 10-year expected inflation rate is highly correlated with the price of crude oil since this price is a significant cost of doing business and therefore has a strong influence on the overall inflation rate (chart).

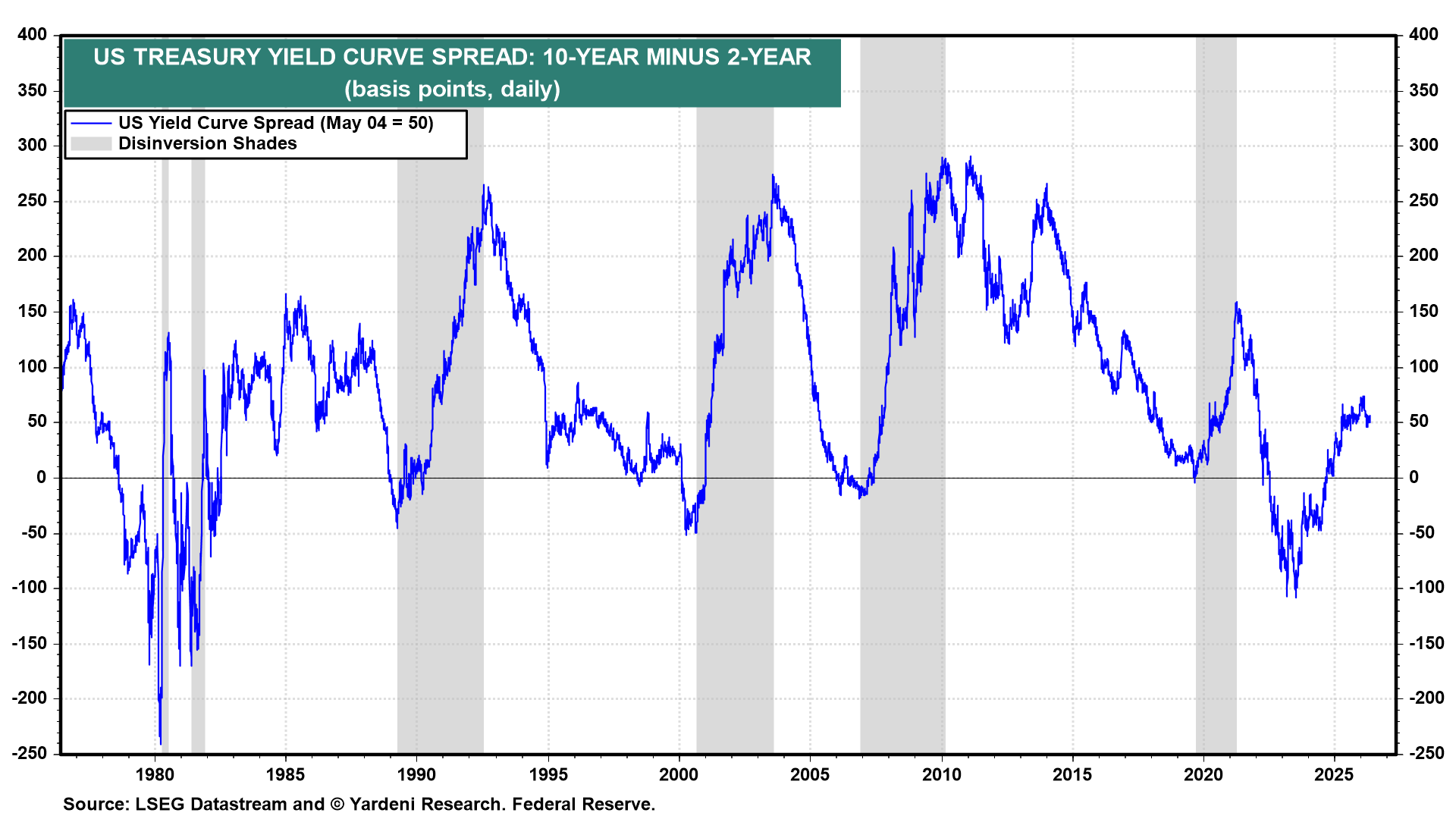

The yield curve has bear-flattened since the start of the conflict (chart). The bond market is discounting higher inflation and a Fed that stays on hold or may even have to tighten.

Indeed, the 2-year Treasury yield rose above the federal funds rate (FFR) around mid-March, when the war was raging (chart). It remains above the FFR.