The week ahead is dominated by the Fed. Kevin Warsh delivers his first press conference as Fed chair on Wednesday, right after the FOMC releases its policy statement and its Summary of Economic Projections (SEP), which includes the Dot Plot showing meeting participants’ forecasts for the federal funds rate. We expect the Fed to abandon its easing bias and pivot toward a tightening bias.

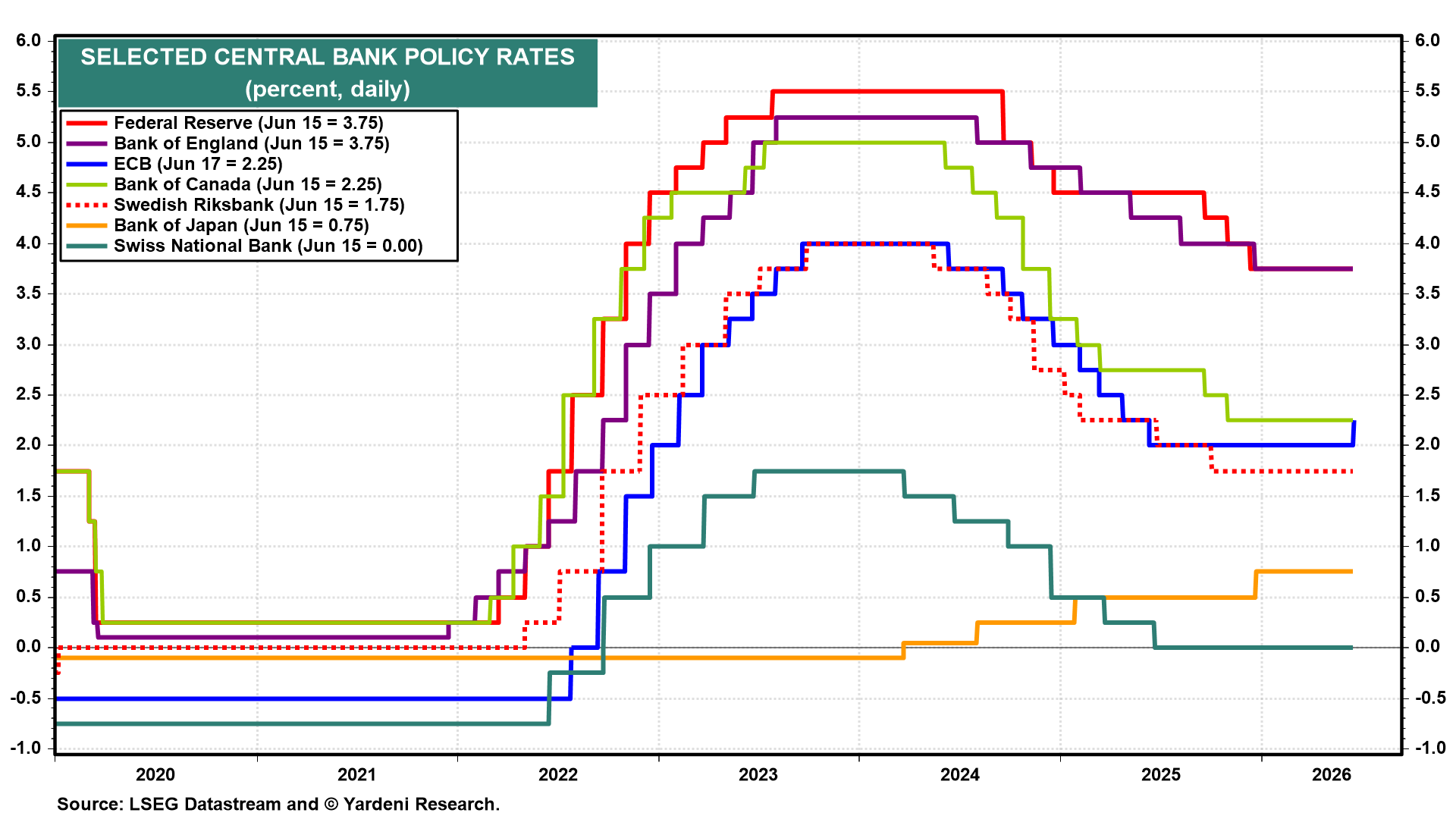

The ECB raised its official rate by 25bps last week (chart). The Bank of Japan is set to lift its short-term policy rate from 0.75% to 1.00% on Tuesday, the highest level since 1995. The Reserve Bank of Australia and the Bank of England round out the global central bank docket, though no rate changes are expected.

The S&P 500 closed Friday at 7,431.46, comfortably above its 50-day moving average at 7,282.00 and its 200-dma at 6,902.33. The uptrend is intact heading into the meeting. SpaceX began trading on Friday and will continue to dominate headlines this week alongside Warsh's debut. Options on the stock go live on Tuesday. Keep in mind, US markets will be closed on Friday for Juneteenth.

Here are the key releases most likely to shape investors' thinking this week:

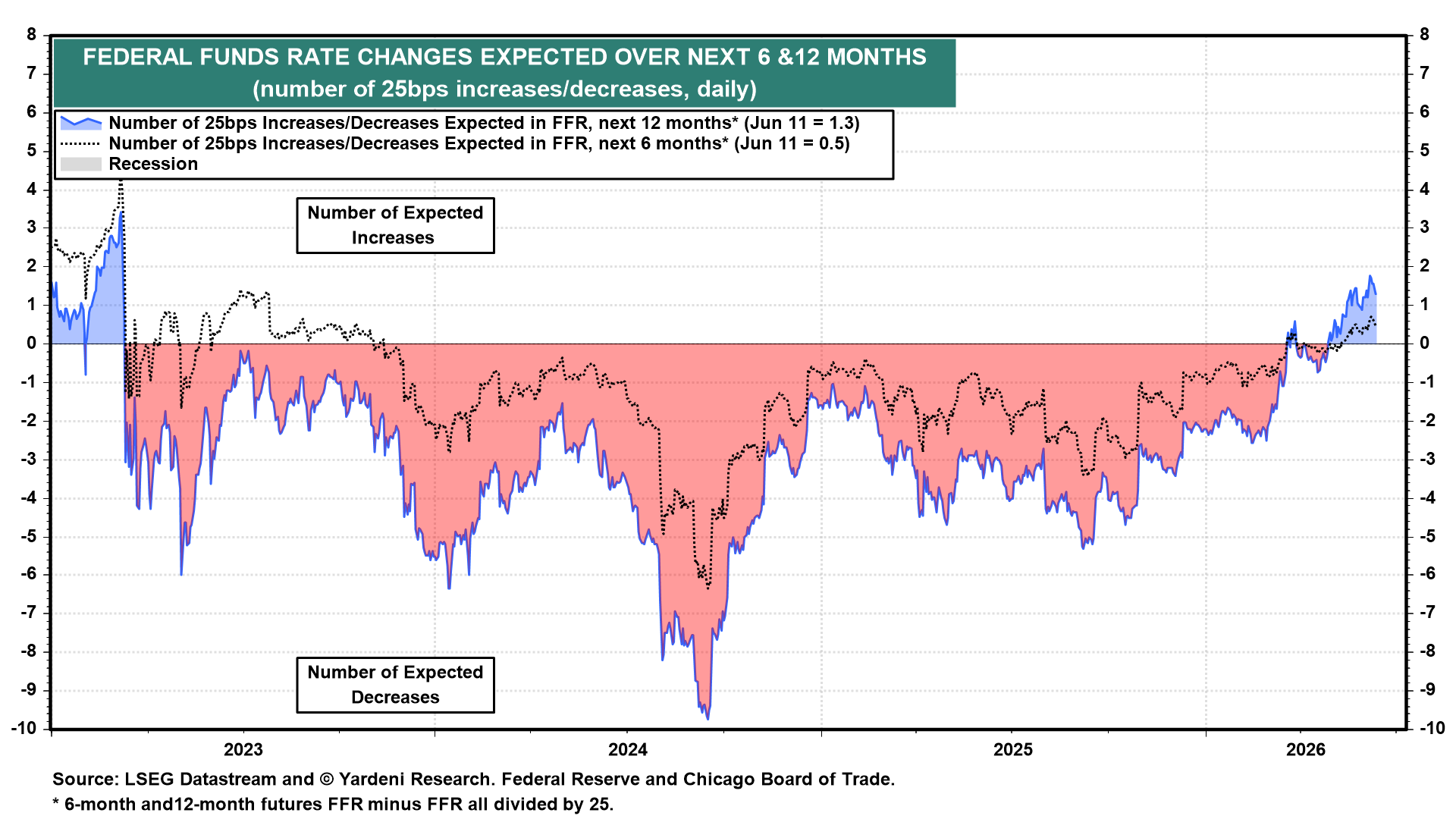

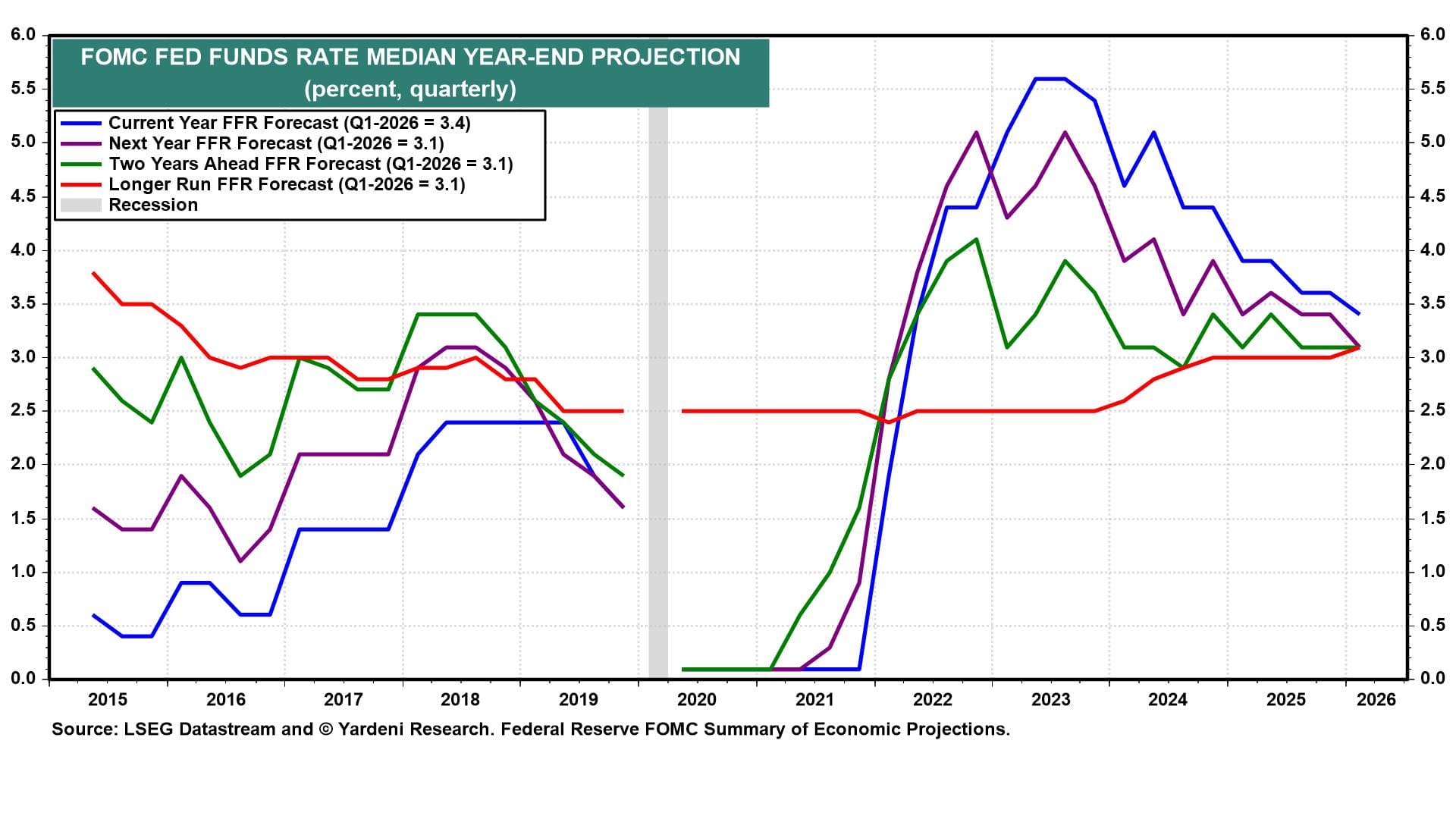

(1) FOMC and the SEP. In recent months, markets have flipped from pricing in Fed rate cuts to pricing in rate hikes, which are expected to start either later this year or early next year (chart). No one expects a rate hike on Wednesday. The only issue is whether the FOMC adopts a neutral or tightening stance. We are in the latter camp since inflation risks are higher than unemployment risks. We admittedly are in the minority.

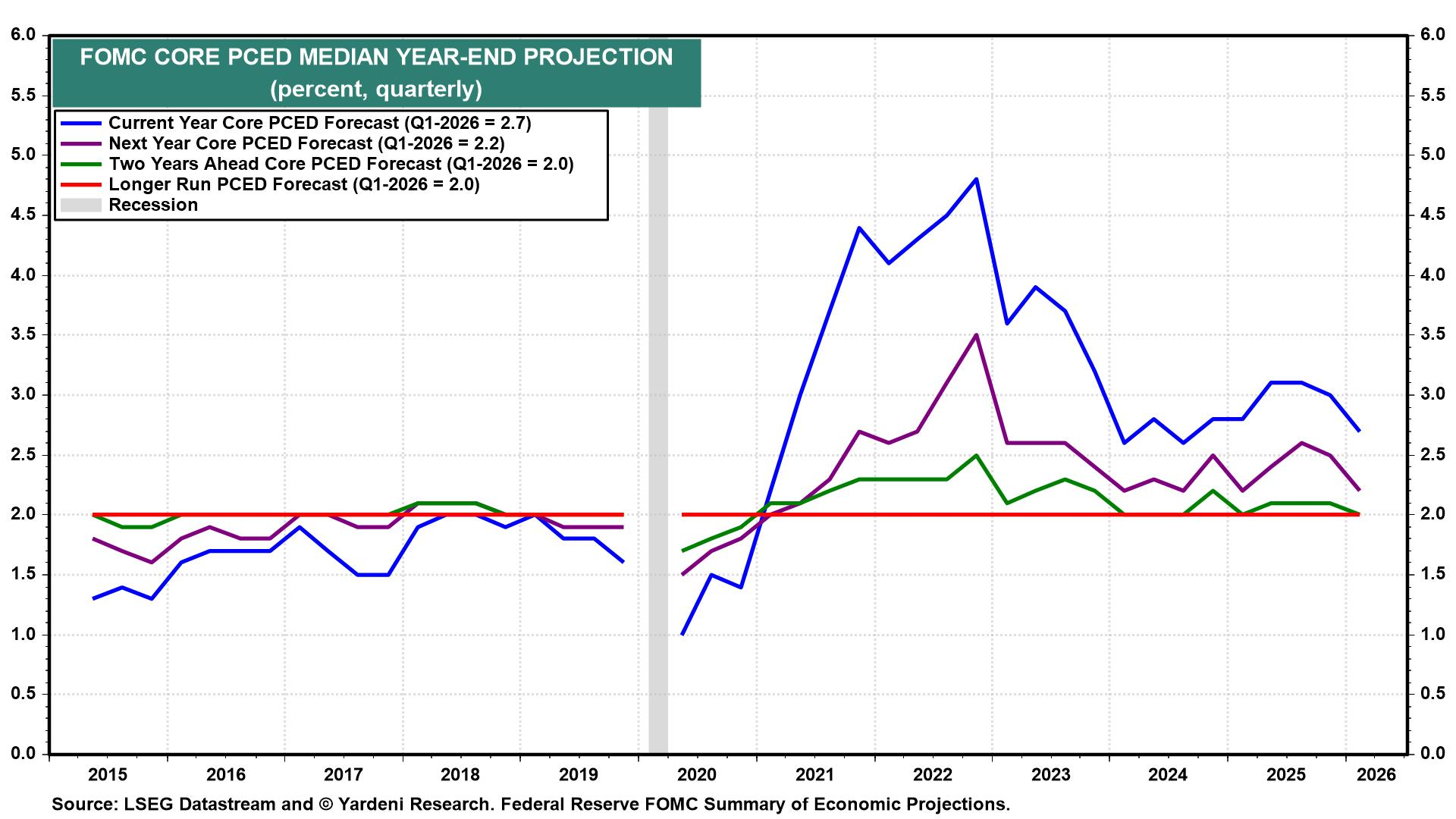

March's SEP had core PCED easing from 2.7% this year to 2.2% next year and 2.0% by 2028 (chart). With recent inflation readings running hot, that glide path looks optimistic.

June's SEP will likely show less optimistic projections for the federal funds rate (FFR) over the course of this year and next year compared to March's SEP (chart). June's Dot Plot is also likely to show higher for longer FFR projections than it did in March.

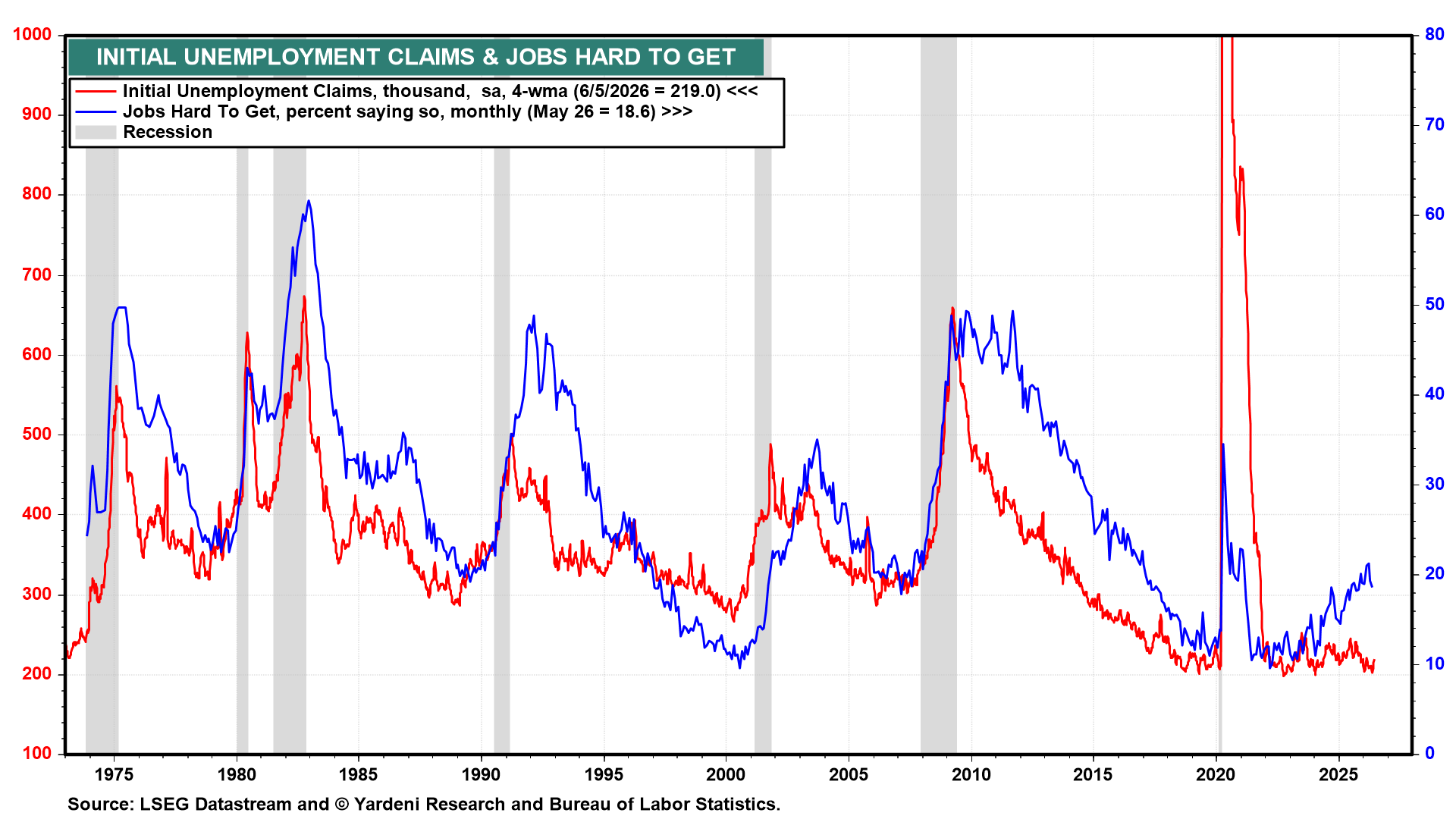

(2) Unemployment. Initial jobless claims (Thu) have drifted higher over the past month. The four-week moving average has climbed to 219,000, with the latest week (June 5) at 229,000. Continuing claims were at 1,795,000 with the four-week average at 1,777,000. The recent uptrend in jobless claims is worth monitoring, though it remains well below levels that would signal labor-market stress or an increase in the unemployment rate (chart).

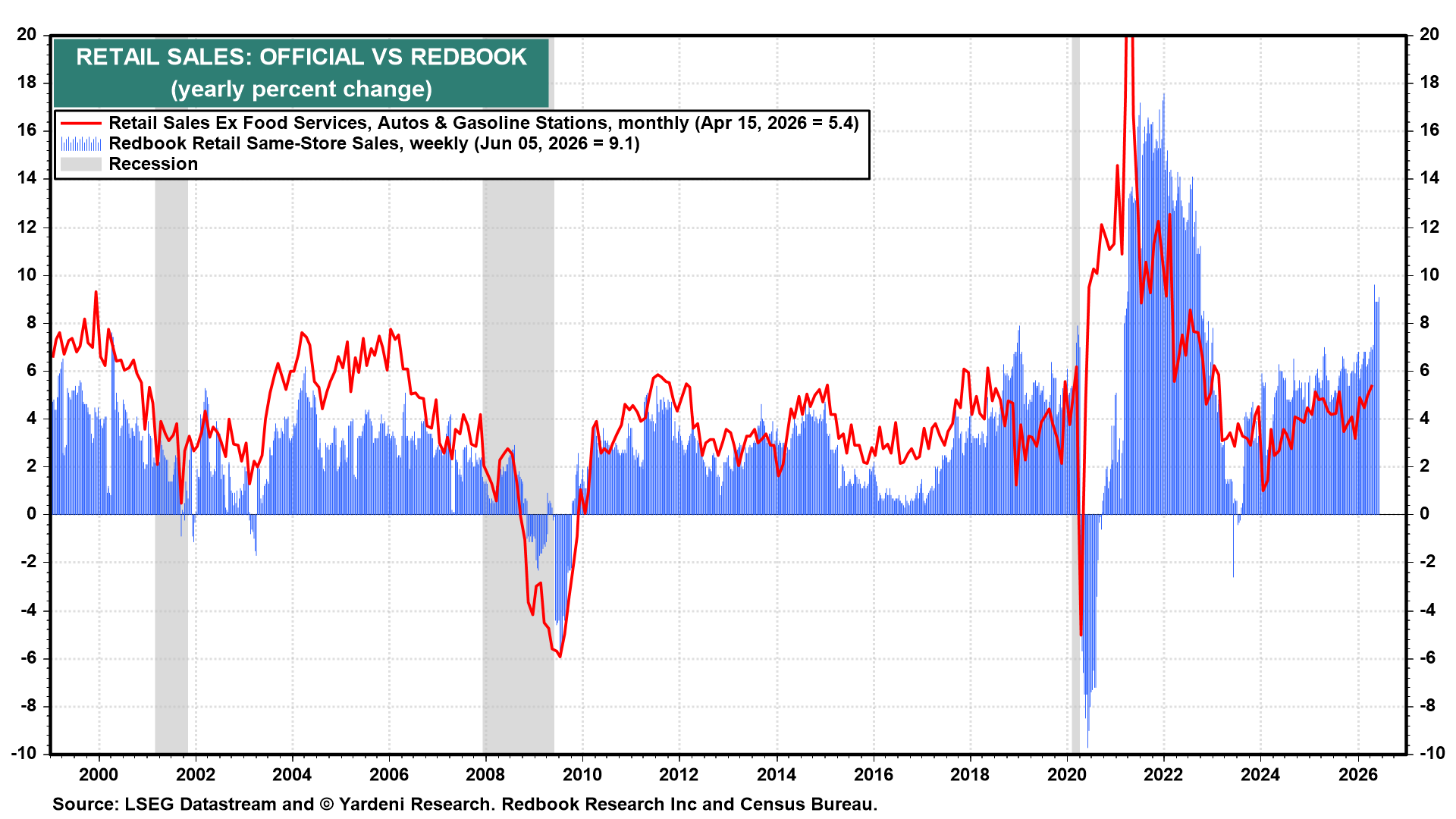

(3) Retail sales. May retail sales (Wed) should be strong. The Redbook same-store gauge rose 9.1% y/y for the week of June 5, well above the 5.4% y/y reading for official retail sales excluding food services, gasoline, and autos in April (chart).

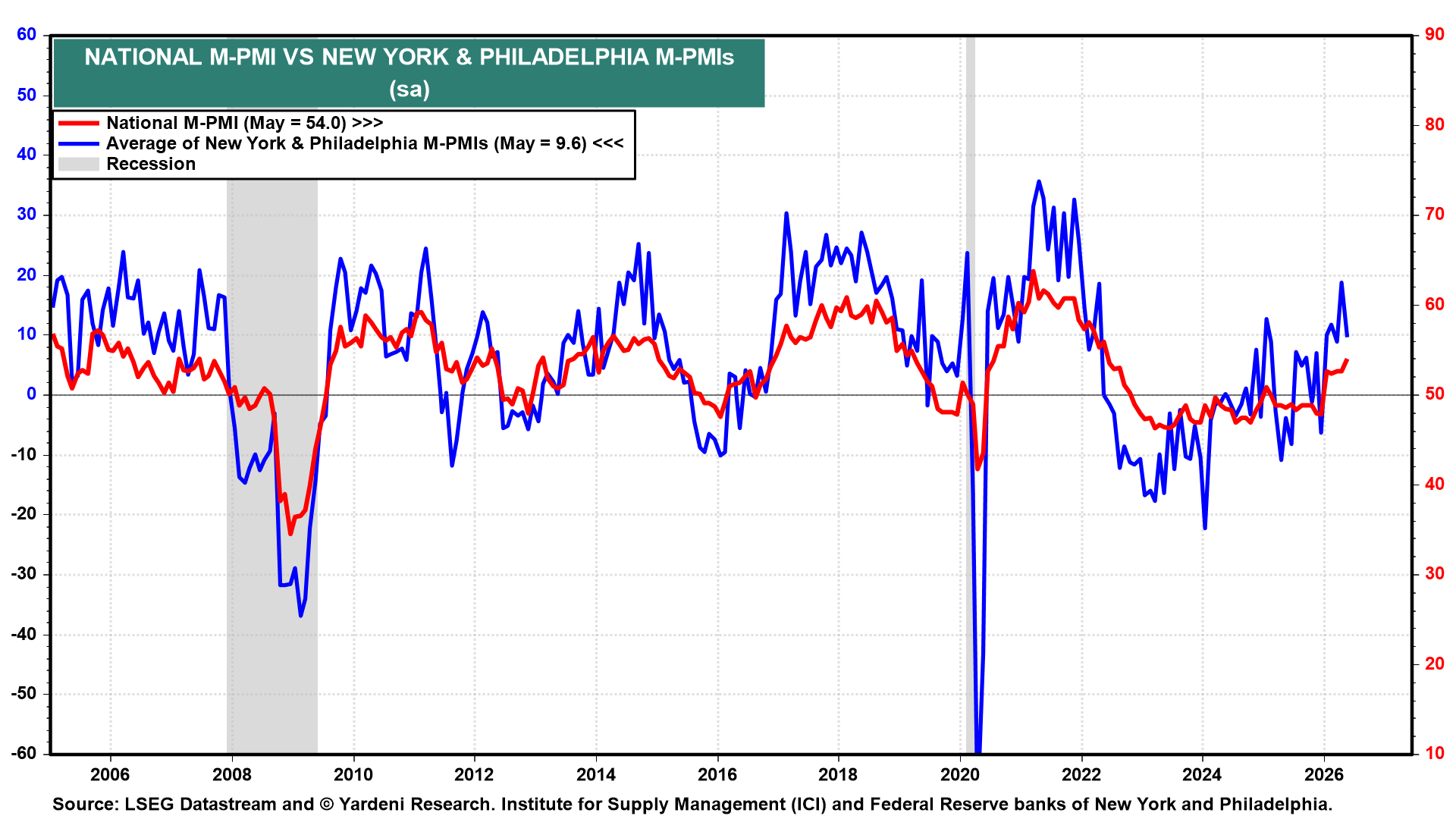

(4) Business surveys. The June regional business surveys conducted by the New York Fed (Mon) and Philly Fed (Thu) are the early reads on what June's national M-PMI might be (chart). They should continue to show the economy and manufacturing expanding nicely.

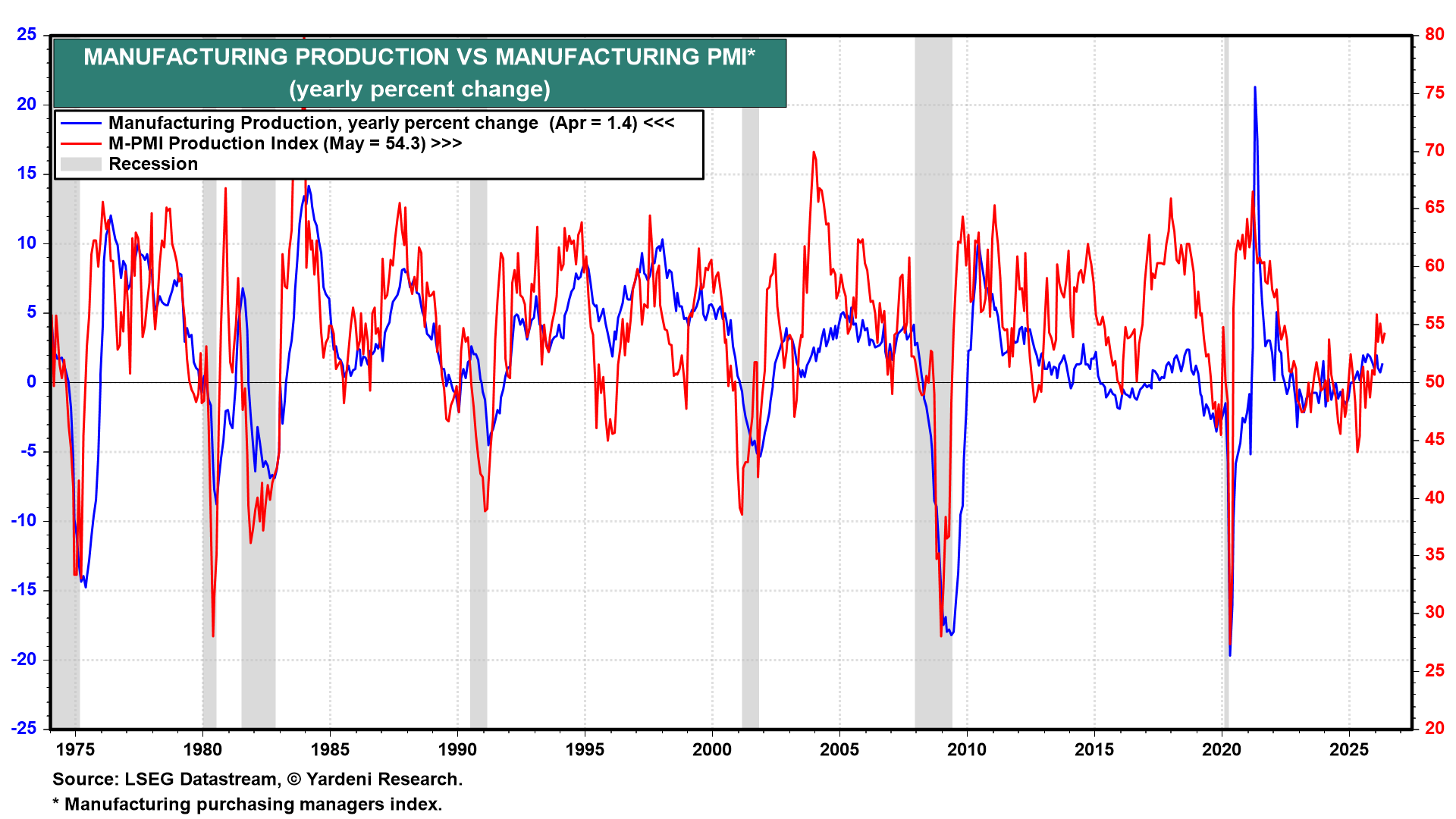

(5) Industrial production. Industrial production (Mon) probably rose solidly in May, given the upbeat reading of May's M-PMI (chart).