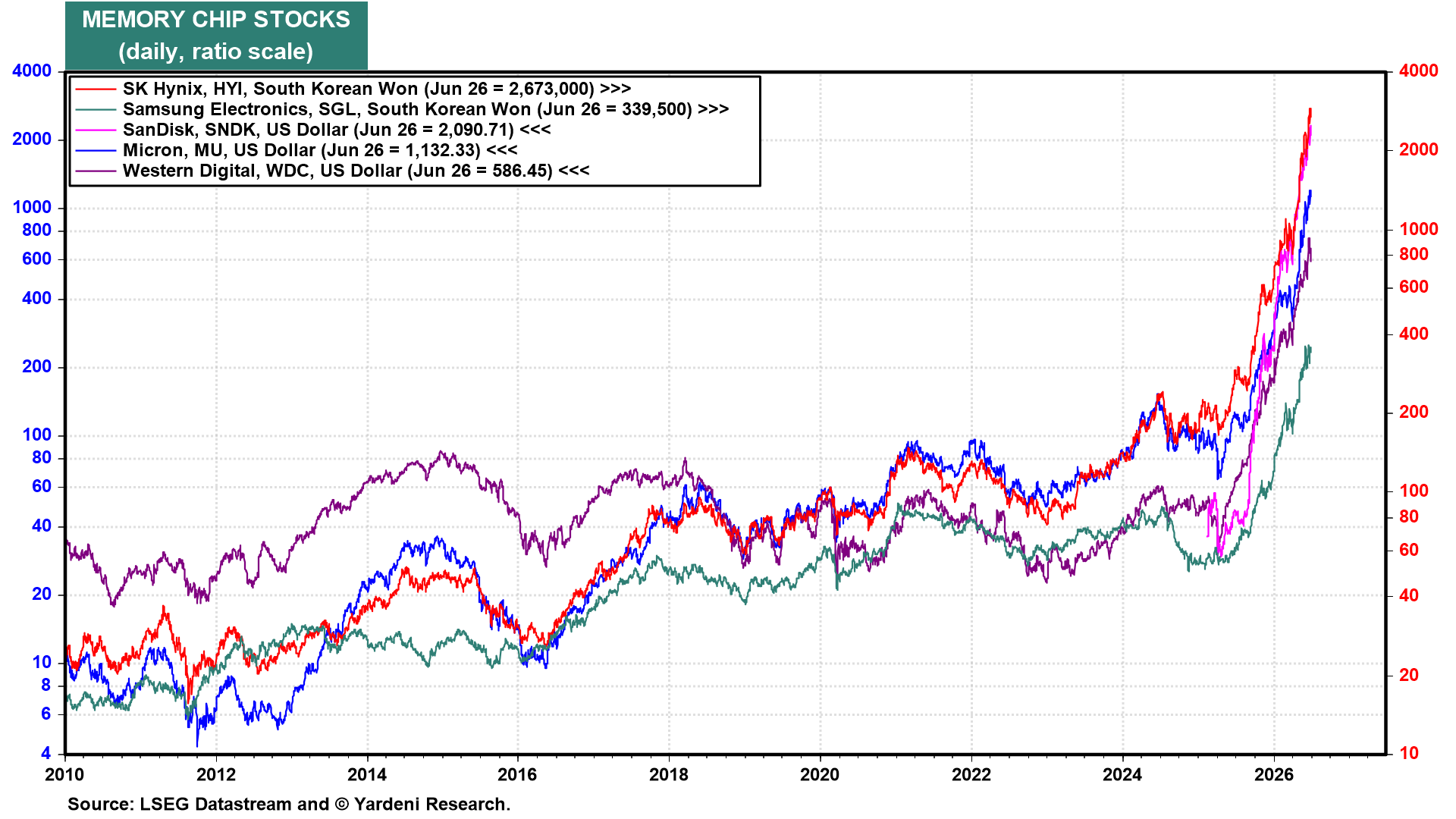

The S&P 500 closed Friday at 7,354.02, down 2.0% on the week, while the Nasdaq fell 4.5%. Apple and Microsoft raised their consumer product prices on Thursday, citing memory and storage chip costs that have more than doubled since last fall and are expected to double again by late 2027. The driver is demand for DRAM and NAND from AI data centers. Memory chip stocks have gone parabolic, extending their rally after Micron’s blowout earnings report on Wednesday (chart).

The price of a barrel of WTI crude oil fell to $69.23 on Friday, down 9% on the week and marking the lowest weekly close since February 27. Strait of Hormuz traffic continues to pick up, with Persian Gulf exports back to roughly 75% of prewar levels.

President Trump accused Iran of violating the ceasefire after drones struck a vessel in the strait on Friday. US Central Command (CENTCOM) executed retaliatory airstrikes. US aircraft targeted and destroyed Iranian coastal radar stations as well as missile and drone storage facilities. In retaliation for the US airstrikes, the IRGC launched a wave of attack drones targeting Bahrain, home to the US Navy's 5th Fleet. Just another day in paradise.

US financial markets are closed on Friday for Independence Day, and June's employment report has been pulled forward to Thursday. The ECB Sintra Forum runs Monday-Wednesday, with Kevin Warsh making his first international appearance as Fed chair on a policy panel Wednesday.

Here are the key economic releases most likely to shape investors' thinking this week:

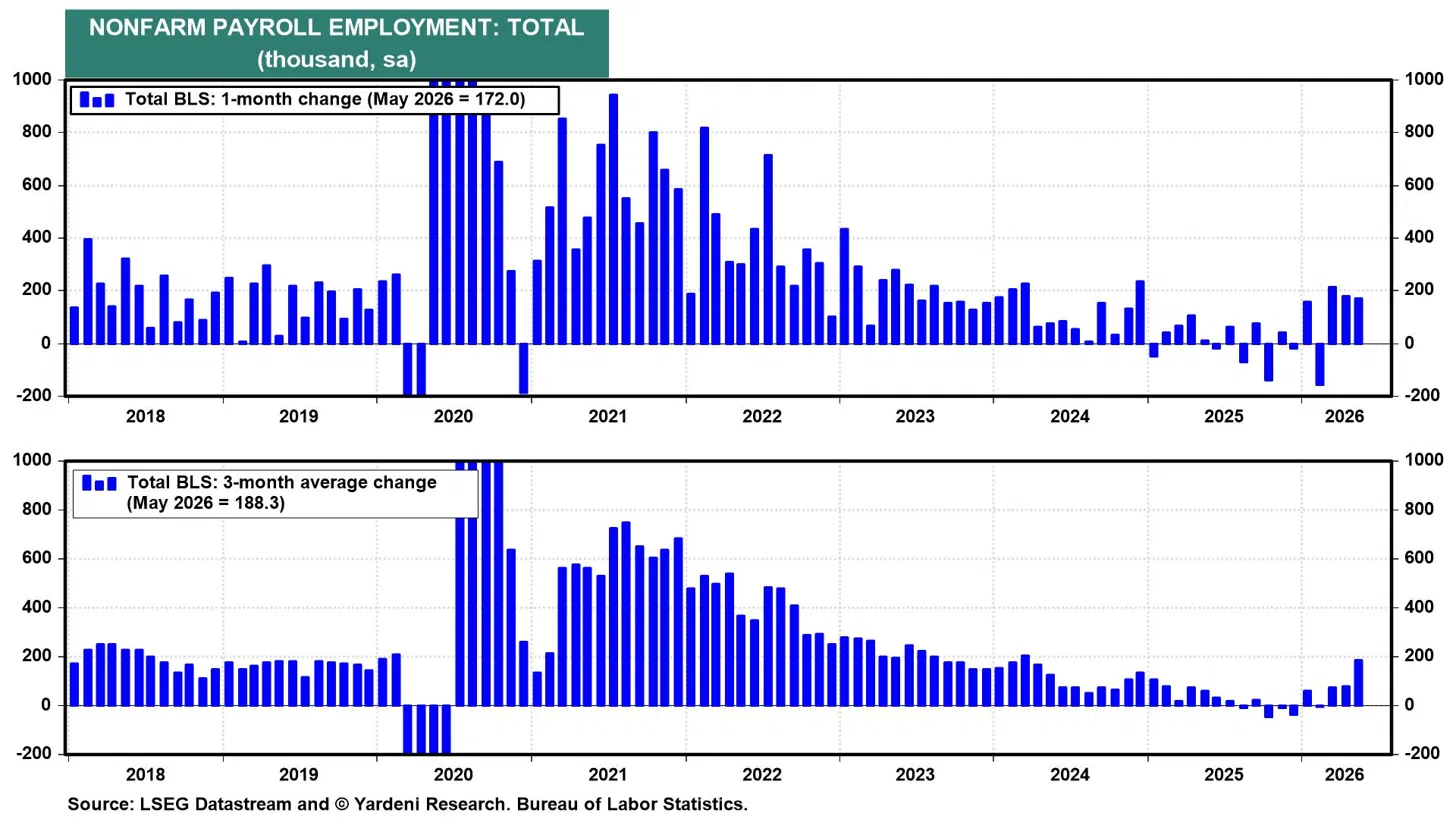

(1) Employment. June’s employment report (Thu) is the headliner. Labor-market data have shown strength in recent months: May payrolls rose 172,000, lifting the three-month average to 188,300 after revisions added 93,000 to March and April combined (chart). The question is whether that strength is sustainable, with average hourly earnings the key indicator of whether wage inflation is stabilizing or still easing.

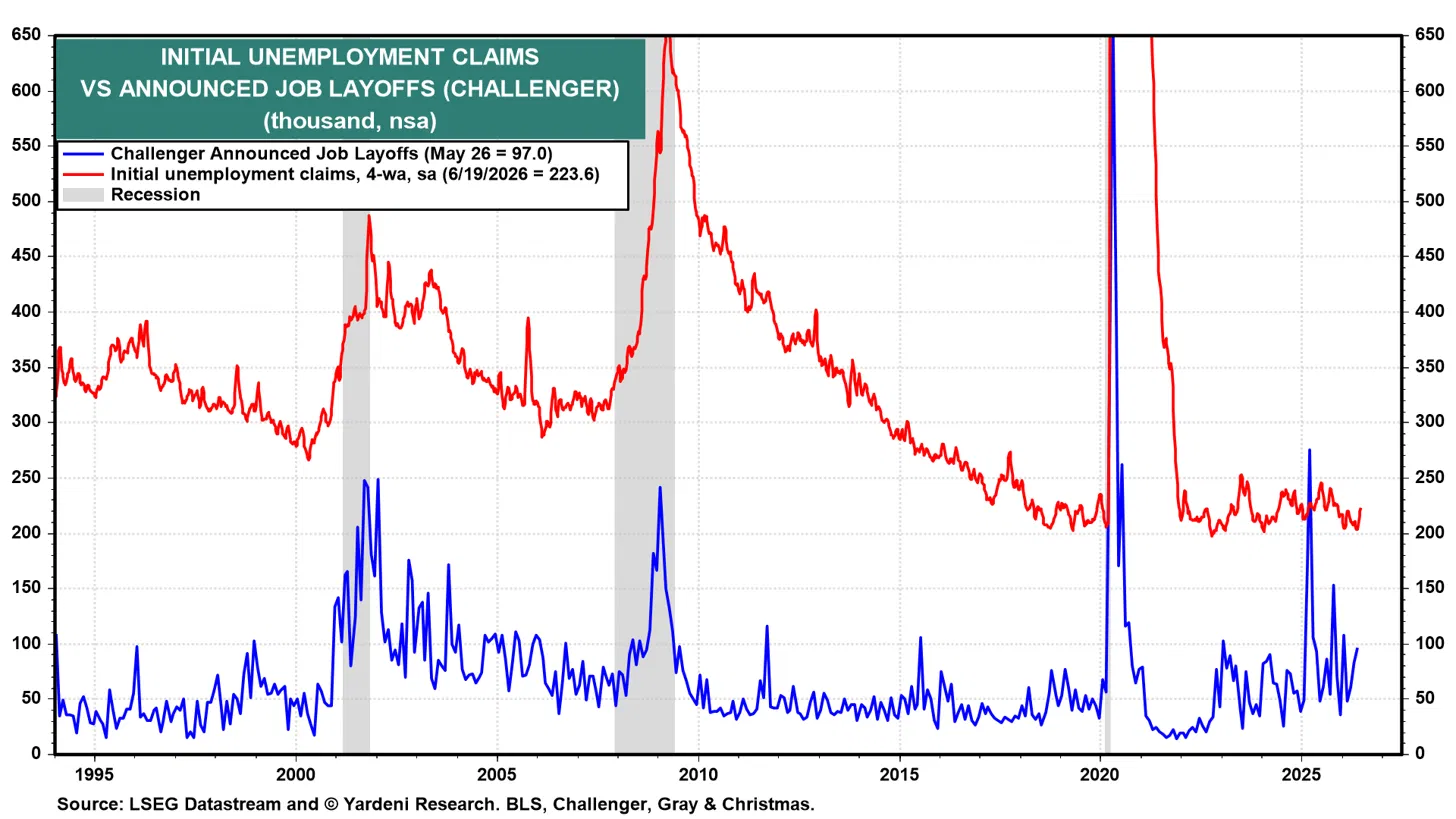

So far this year, Challenger layoff announcements (Wed) have been volatile but relatively subdued. June's number probably remained low, with AI likely cited as the main reason for job cuts, particularly in the technology industry (chart).

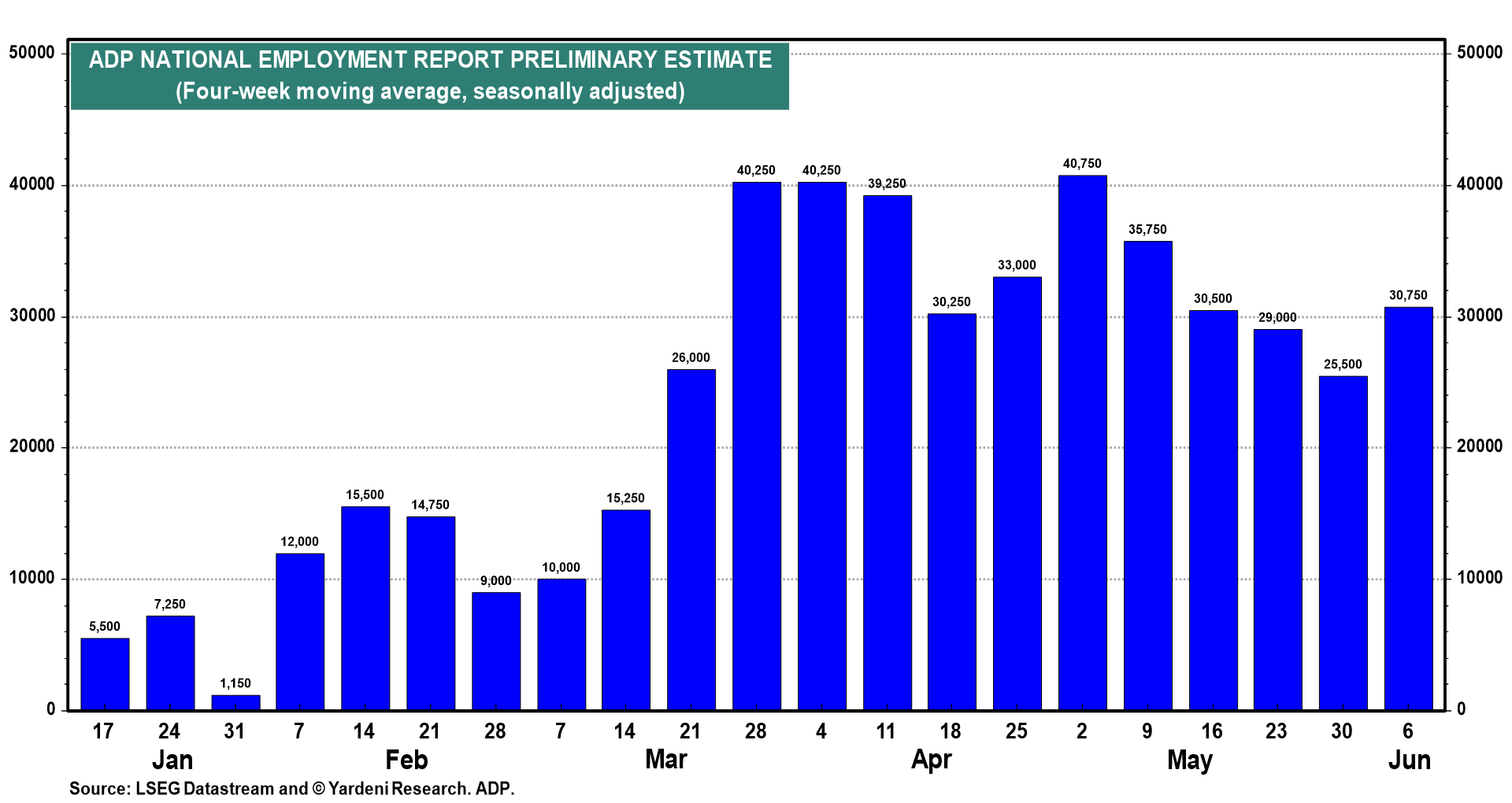

May's ADP private payrolls rose 122,000, the strongest monthly total since January 2025, and broad-based, with eight of 10 sectors yielding monthly gains. Education & Health Services led with 57,000. June's ADP report (Wed) should show more of the same, given ADP's recent strong weekly readings (chart).

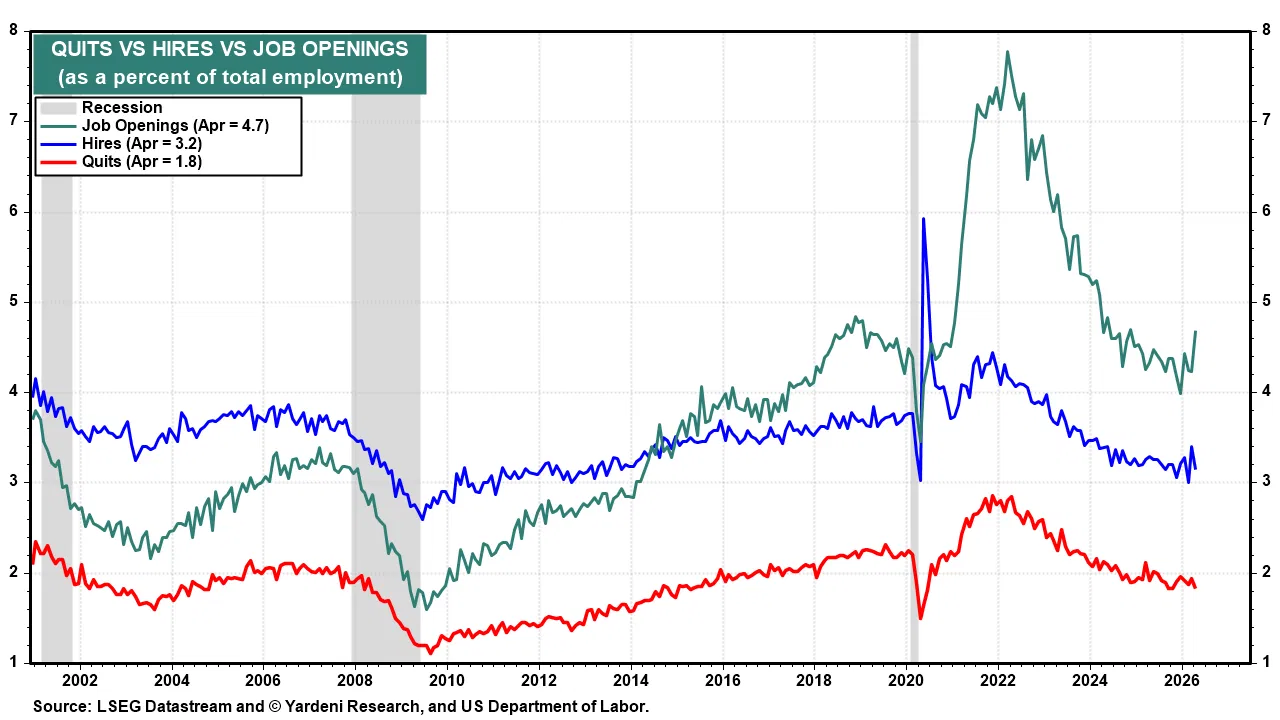

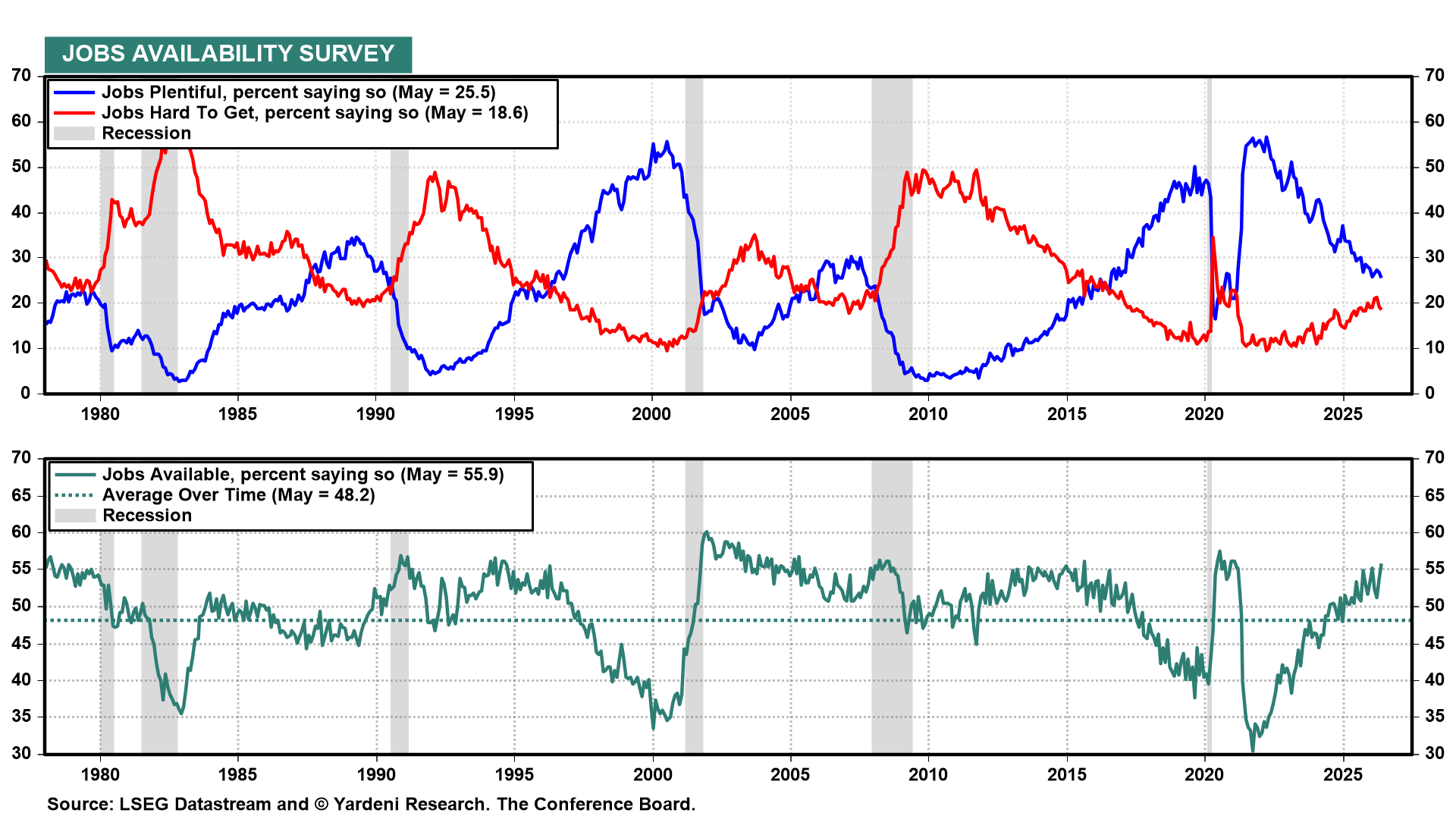

May’s JOLTS data will also be reported on Tuesday. April’s job openings rate suggests this series is bottoming (chart).

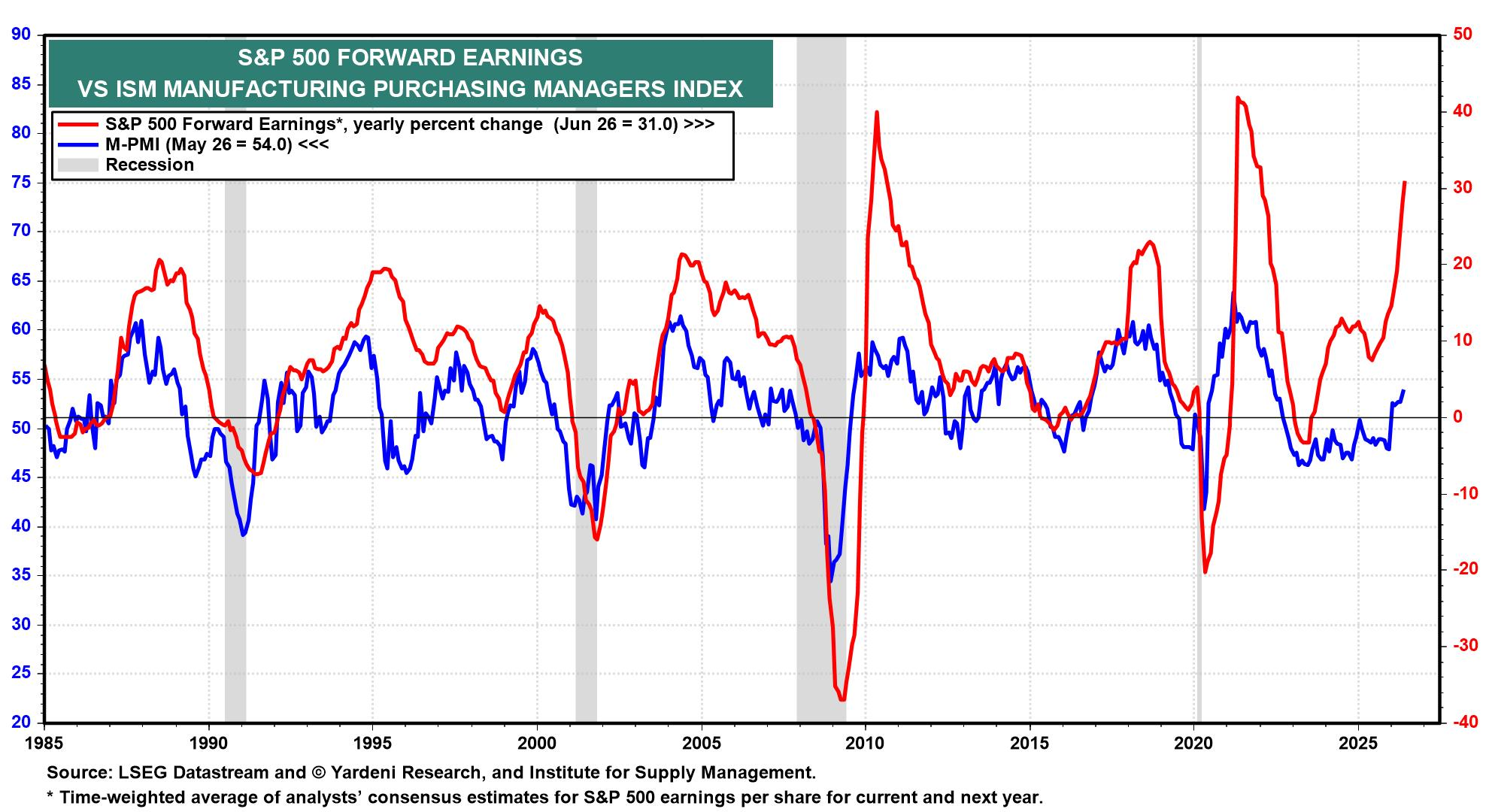

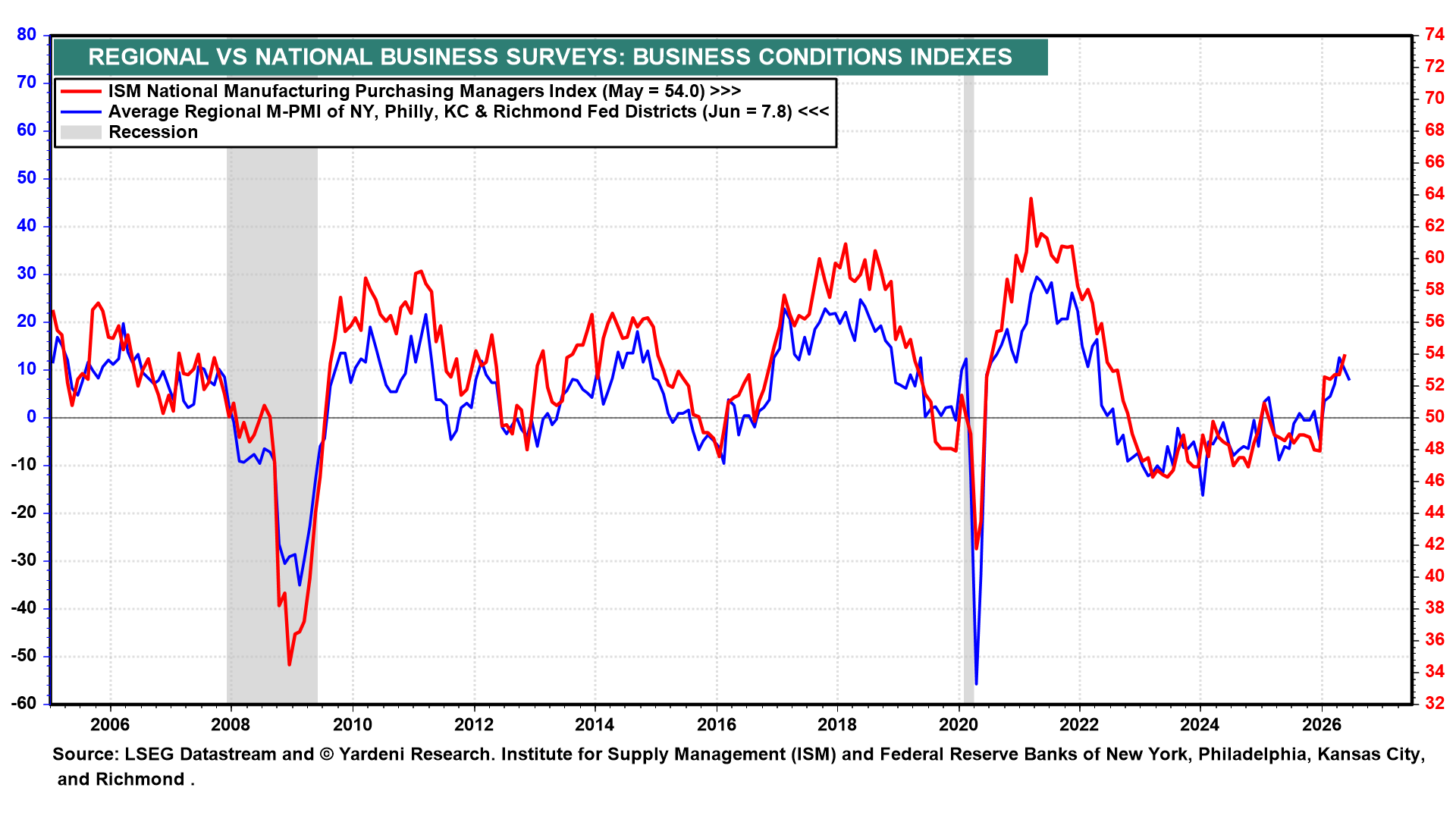

(2) Manufacturing Surveys. ISM's M-PMI (Wed) was 54.0 in May, its fourth straight expansionary month (chart). Recent FEMO (Fabulous Earnings Momentum) points to further upside for June's M-PMI.

The Dallas Fed's June regional business survey (Mon), along with the four other regional surveys already released, should confirm that June's M-PMI remained above 50.0 (chart).

(3) Consumer Confidence. June's Consumer Confidence Index survey should confirm that the labor market remains stable (chart).

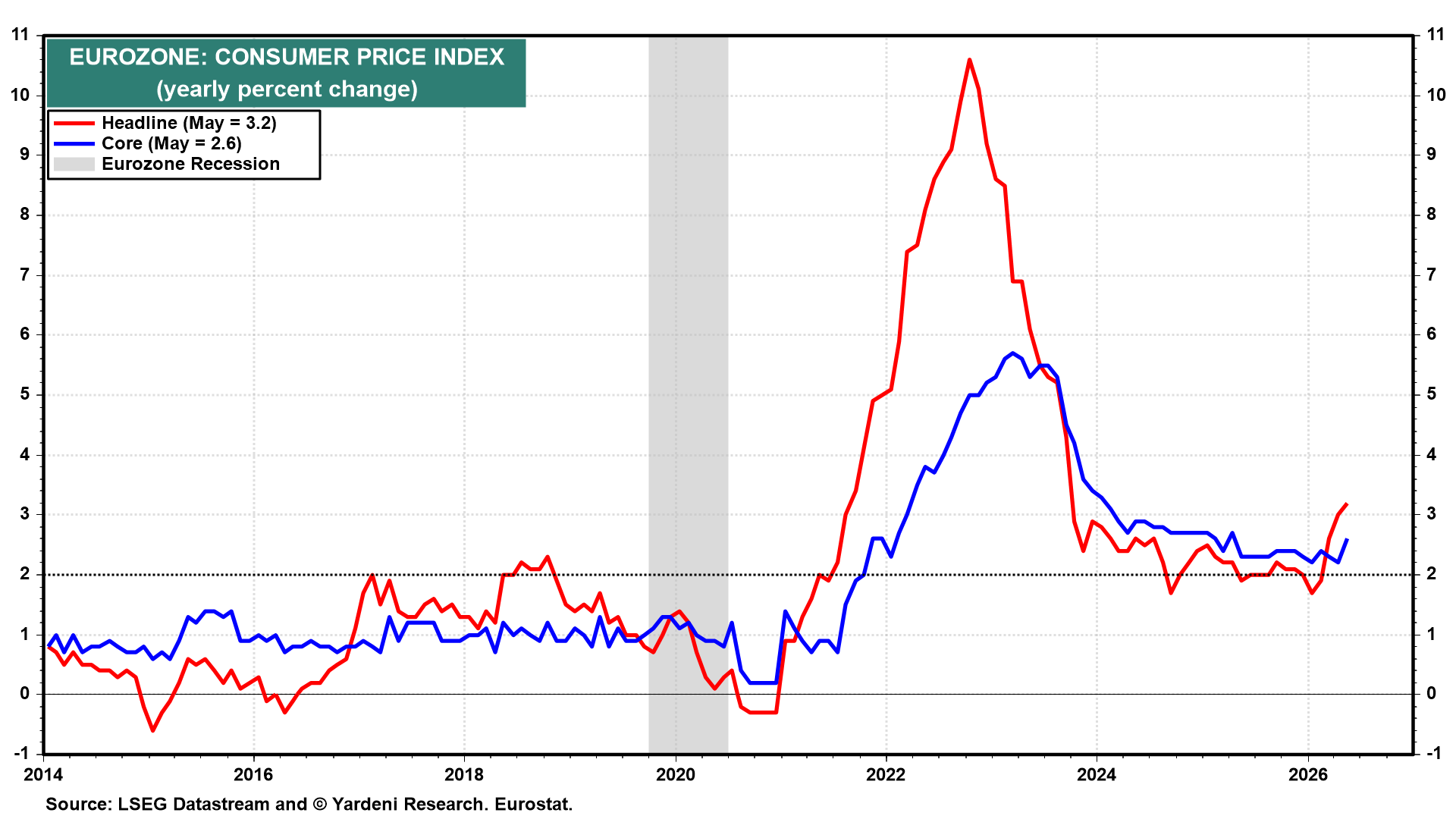

(4) Eurozone Inflation. The Eurozone headline and core CPI inflation rates (Wed) for June should show the former easing, alongside energy prices (chart). The core inflation rate should determine whether the ECB continues to raise interest rates.