The mega IPOs are coming. SpaceX is set to go public on June 12, raising $75 billion to $80 billion at a market valuation of up to $1.8 trillion. It will be the largest equity offering in history. Then, Anthropic and OpenAI are expected to go public with market capitalizations of $1 trillion to $1.75 trillion each. Fears are mounting that the "AI-3" IPOs will suck the oxygen out of the rest of the stock market. We aren't as concerned.

The combined market value of these three companies is widely expected to total $4 trillion to $5 trillion once they go public. The capital being raised is around $200 billion. To raise so much money, Wall Street's investment bankers are planning to give retail investors the opportunity to participate in these IPOs. We expect that they will respond enthusiastically.

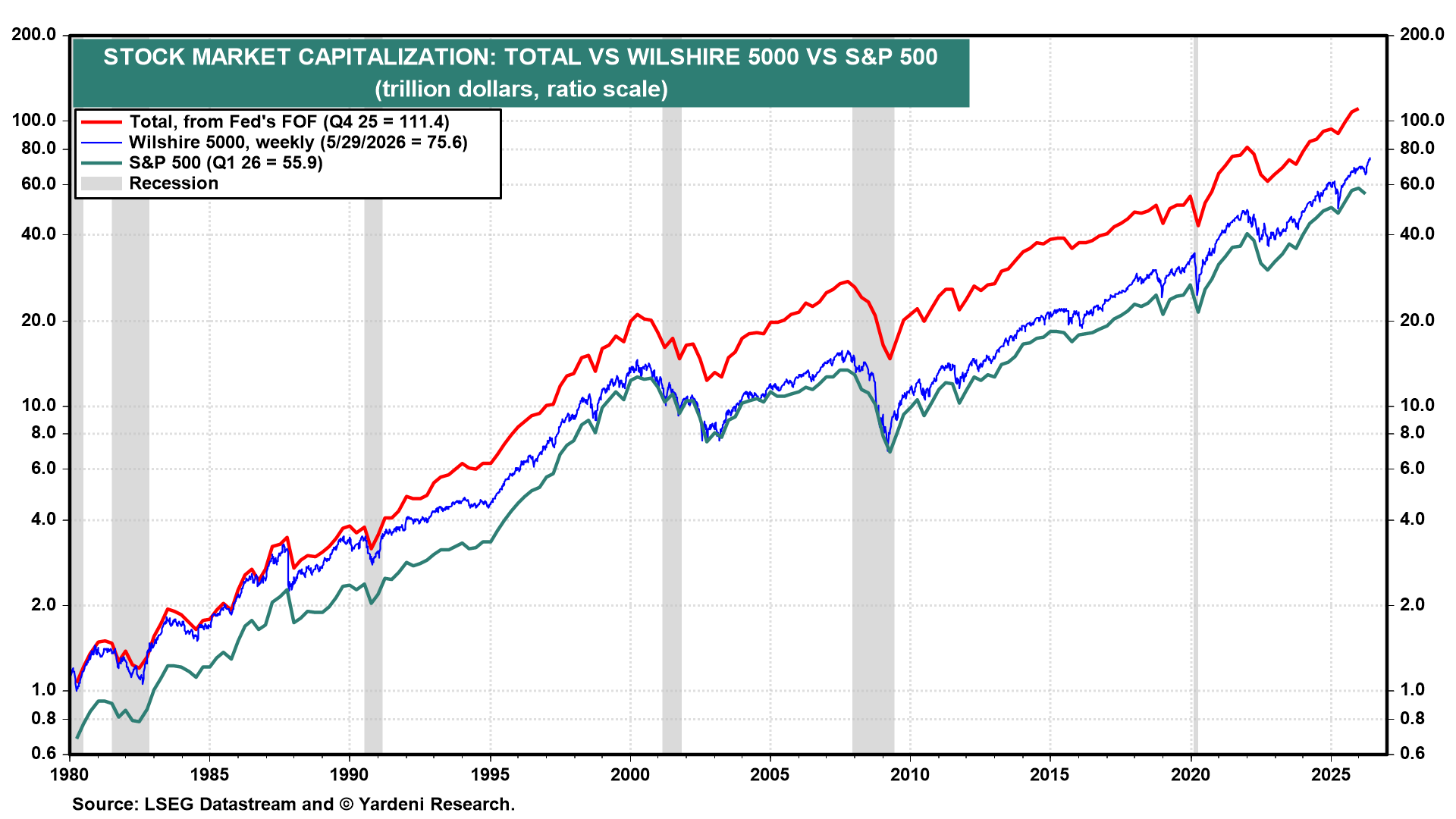

The market capitalization of the Wilshire 5000 is $75.6 trillion (chart). It is close to $60.0 trillion for the S&P 500. Will these measures increase by $4 trillion to $5 trillion when the AI-3 go public? Not based on free float, i.e., the shares that are available for the pubic to trade (excluding closely held shares, insider holdings, and government stakes). SpaceX is only floating roughly 4.3% of its shares to the public. The other two AI-3 are also likely to provide relatively puny free float.

Here's more:

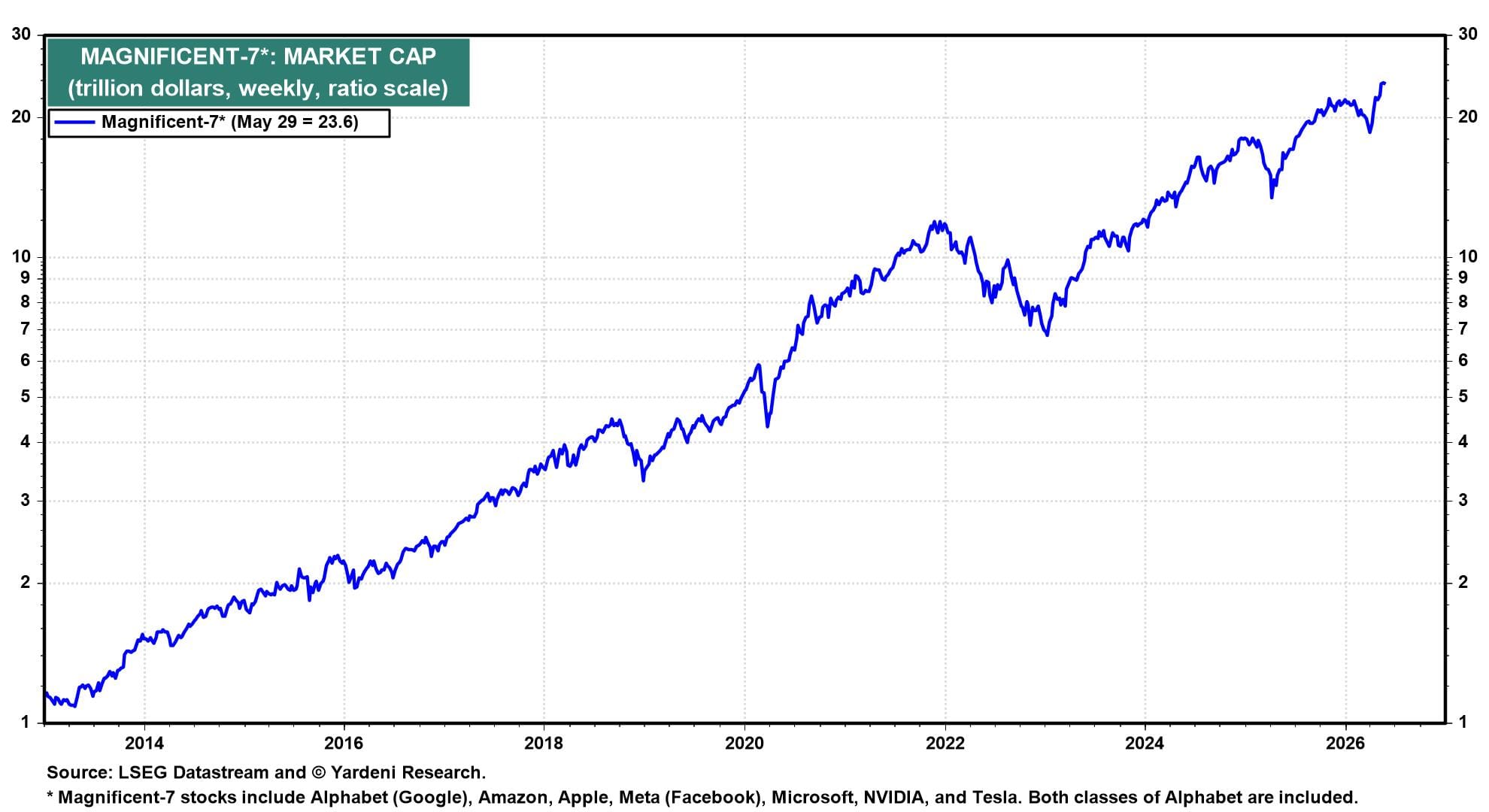

(1) AI-3 vs Mag-7. The Magnificent-7 currently have a total market capitalization of $24 trillion (chart). They have remarkably high public ownership, ranging between 81% and 98%.

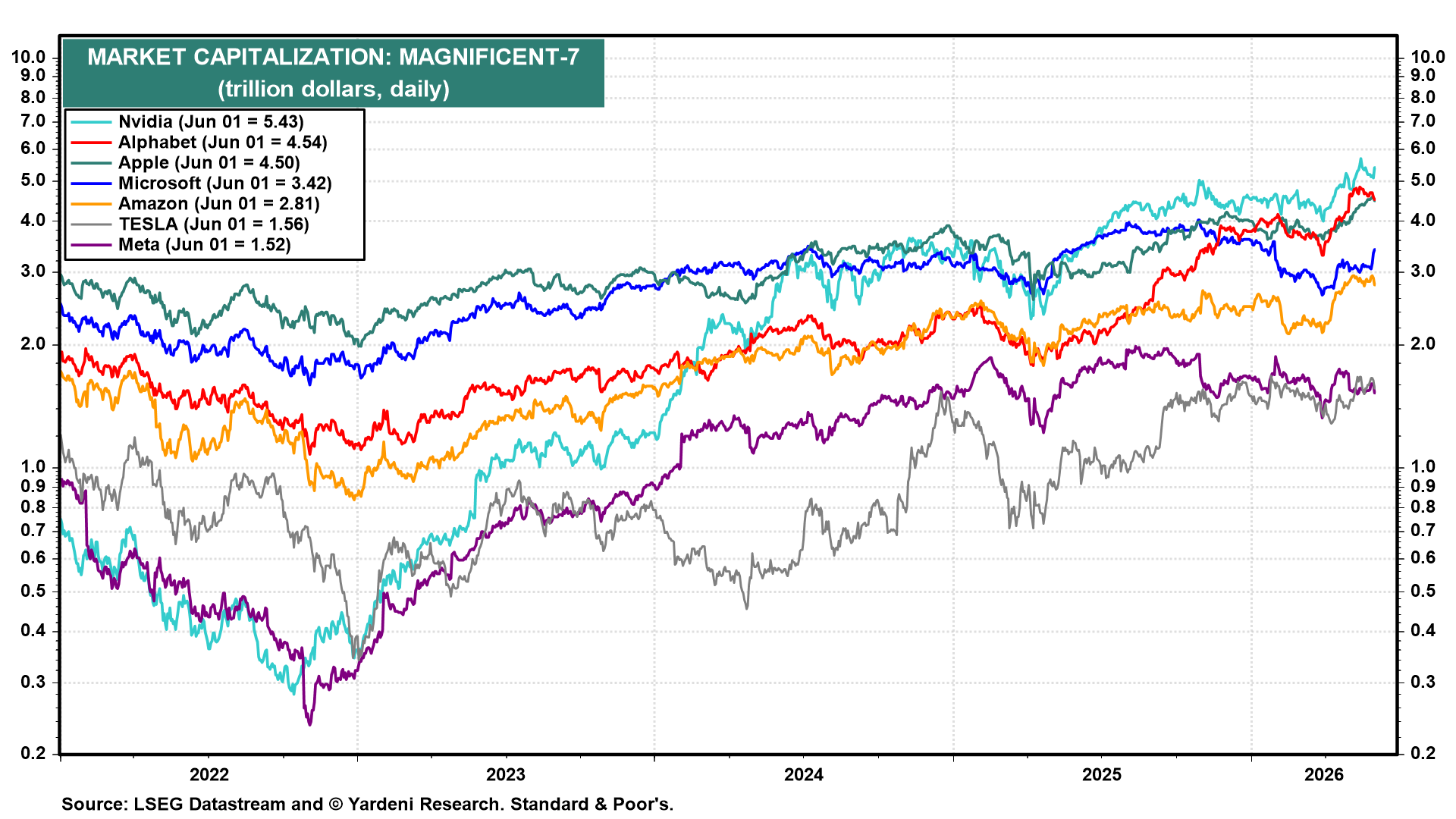

The Mag-7 have total market capitalizations ranging from $1.5 trillion to $5.4 trillion (chart). The AI-3 won't be in the same league, given how tiny their free float will be initially.

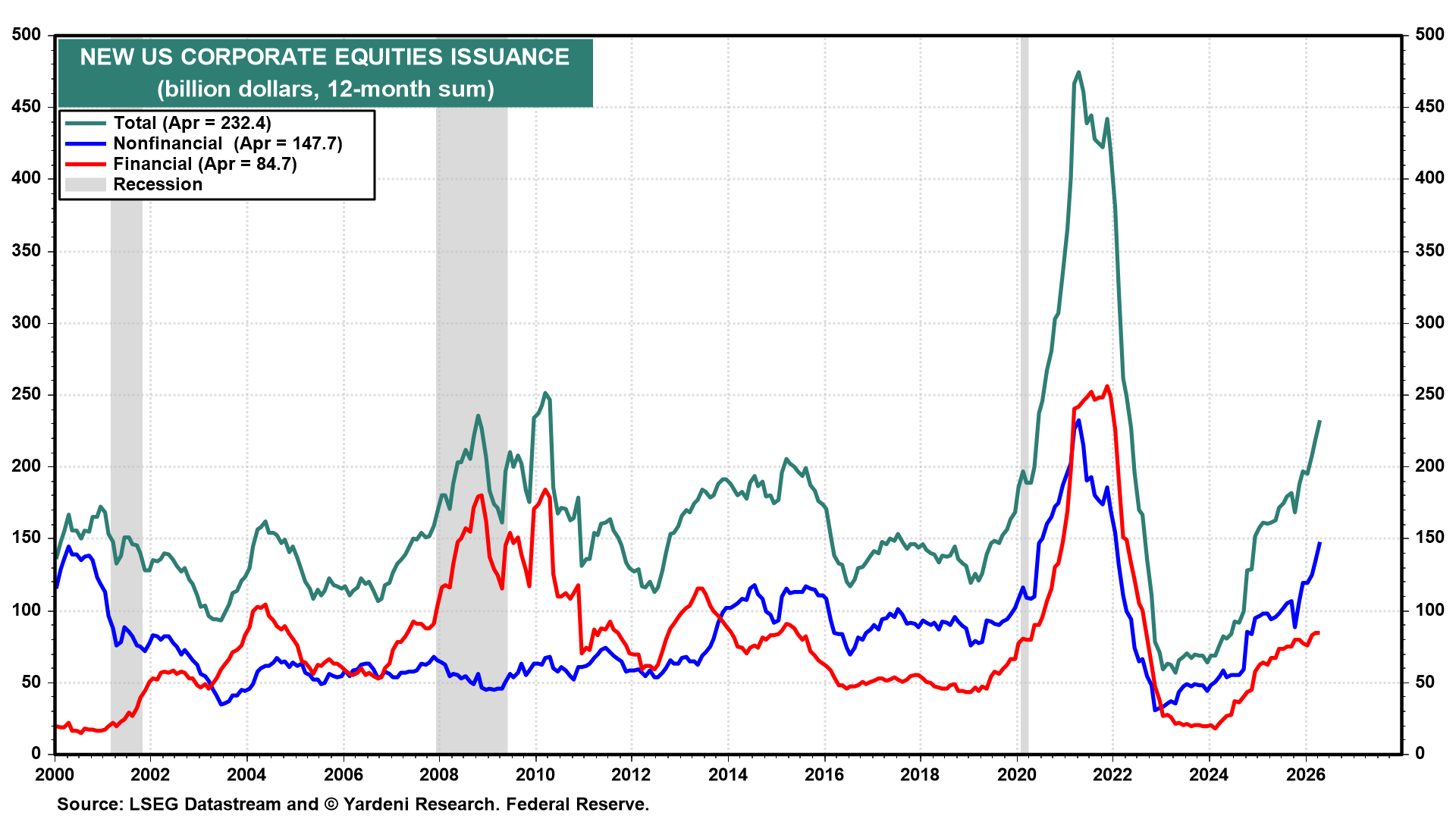

(2) Equity IPO market. In any event, the AI-3 should have no trouble raising $200 billion in the IPO market, which has financed $232 billion in new equity issuance over the past 12 months through April (chart). During 2021, more than $450 billion was raised with equity IPOs.

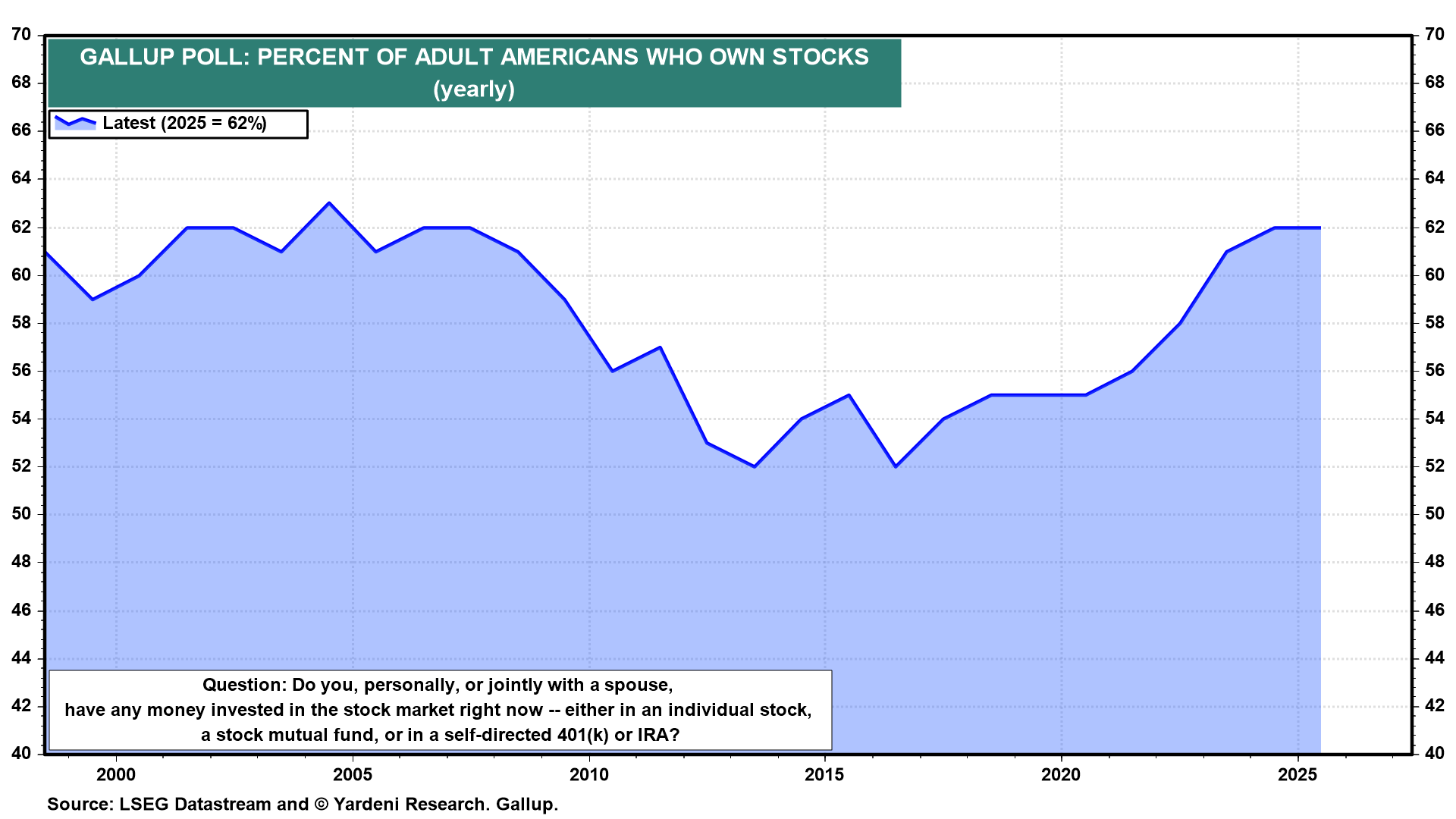

(3) Retail investors. The AI-3 IPOS could attract new retail investors into the stock market. Lots of Americans are already in the market. Last year, 62% of adult Americans owned stock, according to Gallup (chart).

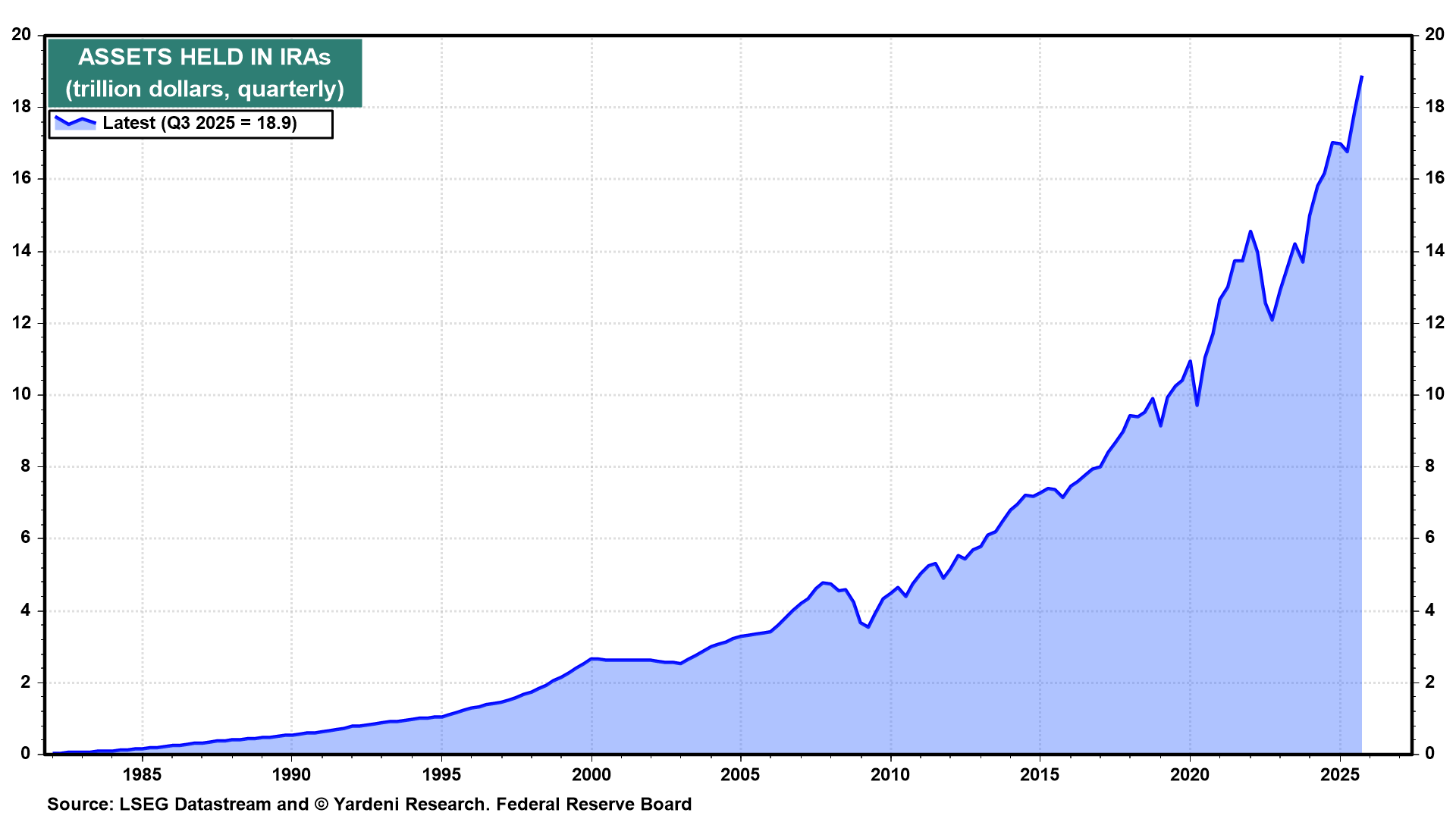

That's not surprising given that assets held in IRAs probably exceed $20 trillion currently (chart).

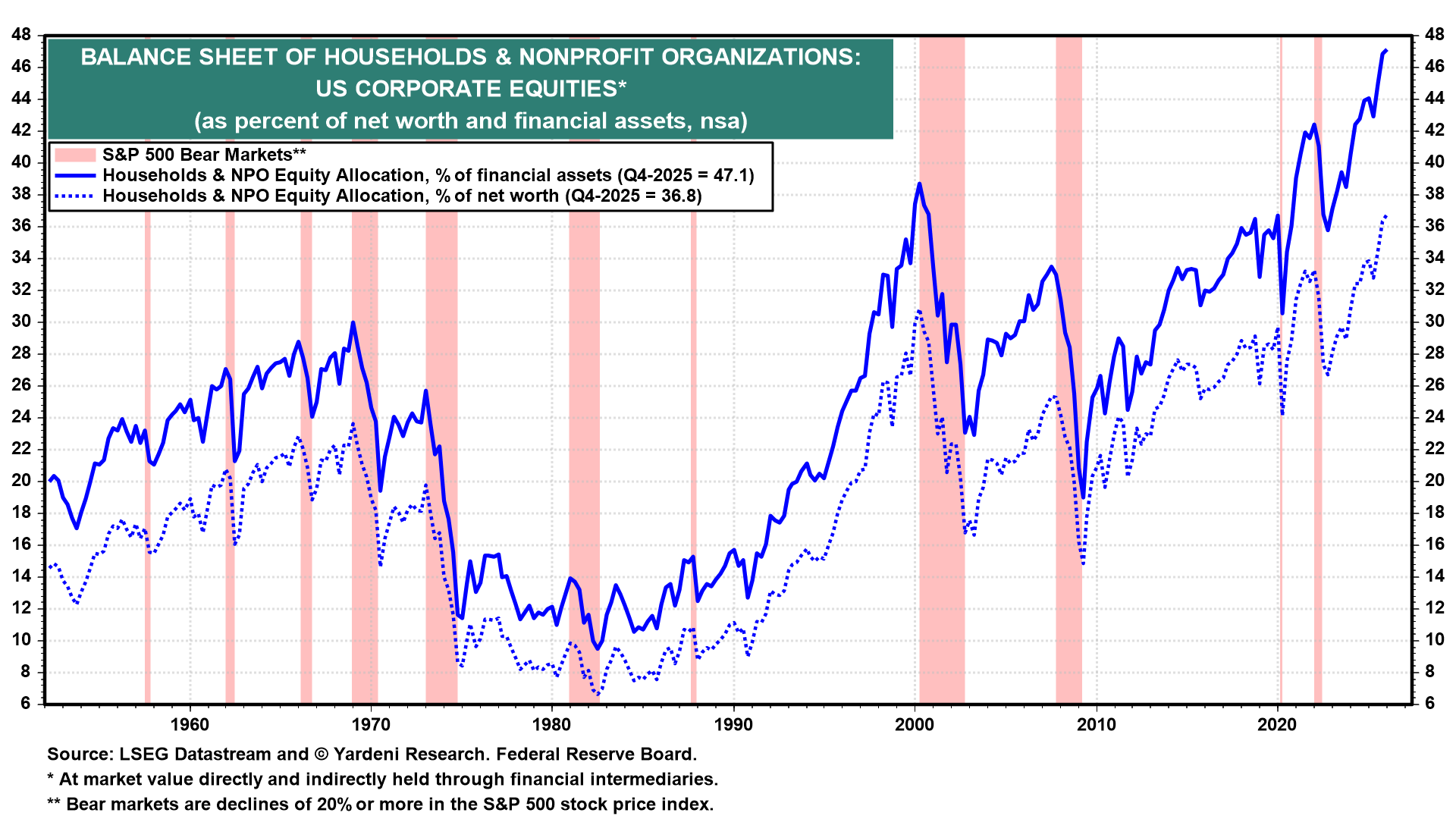

At the end of last year, households (including nonprofit organizations) held a record 36.8% and 47.1% of their net worth and financial assets in equities, respectively (chart).

(4) Wall Street's games. The index providers are rewriting their playbooks to accommodate new entrants to public markets. S&P Dow Jones is considering cutting the S&P 500's seasoning requirement for mega-caps from 12 months to six and waiving the four-quarter GAAP profitability gate that has been in place since 2002. Further, the Nasdaq cut its inclusion window from 90 trading days to 15, effective May 1.

Bloomberg Intelligence estimates S&P 500 funds would need to absorb 19% of SpaceX's public float within six months, with the Russell 1000 and Nasdaq-100 funds absorbing another 24%. Float at the IPO will be roughly 4.3%, as noted above. This is forced buying colliding with a very limited supply. (Where is the SEC?)

Allocation conventions are bending too. We have already personally received emails from our brokers inviting us to participate in the SpaceX IPO. Retail involvement of this scale is unusual.

(5) Burning cash faster than rocket fuel. The combined 2025 losses of the AI-3 topped $25 billion. SpaceX lost $4.9 billion last year. Much of its projected valuation is based on a $22.7 trillion enterprise AI market that does not yet exist as a revenue source. There has been no proof of concept for launching data centers into space.