Fed Chair Kevin Warsh has often said that the members of the Federal Open Mouth Committee should talk publicly less often. He wants the Fed to follow the financial markets rather than the other way around. Yet, two weeks after his first press conference as Fed chair on Wednesday, June 17, he is scheduled to appear on a policy panel on Wednesday, July 1, at the annual ECB Forum on Central Banking.

Investors will be following closely what he has to say. They did the same during his presser. They heard him mention "price stability" eight times. In effect, he reiterated the final sentence of the June 17 FOMC statement: "The Committee will deliver price stability." In his prepared comments for his presser, he said, "We recognize that inflation has been running well ahead of the Fed’s long-stated inflation goal of 2 percent that’s been going on for more than five years."

We anticipated that the FOMC would pivot from its easing bias to a tightening bias at the June meeting. However, we were surprised by Warsh's hawkishness. After all, President Donald Trump picked him to replace Fed Chair Jerome Powell because he publicly backed the president's call for the Fed to lower the federal funds rate (FFR).

Yet the White House didn't call out Warsh for his hawkish stance during his presser. When asked for his reaction, Trump said Warsh is "fantastic" and stated, "I want him to do whatever he wants." Speaking at the Economic Club of New York on June 23, Treasury Secretary Scott Bessent responded to a question about Warsh saying, "Warsh will optimize the path for inflation and economic growth. He will be independent and do what he wants."

We believe that there is a new Treasury-Federal Reserve Accord aimed at lowering the 10-year Treasury bond yield. Bessent and Warsh are working as a team. They seem to have convinced the president that the best way to lower borrowing costs is to talk tough about bringing down inflation and to hike the FFR if necessary. That should lower bond yields, stimulating the economy.

Consider the following:

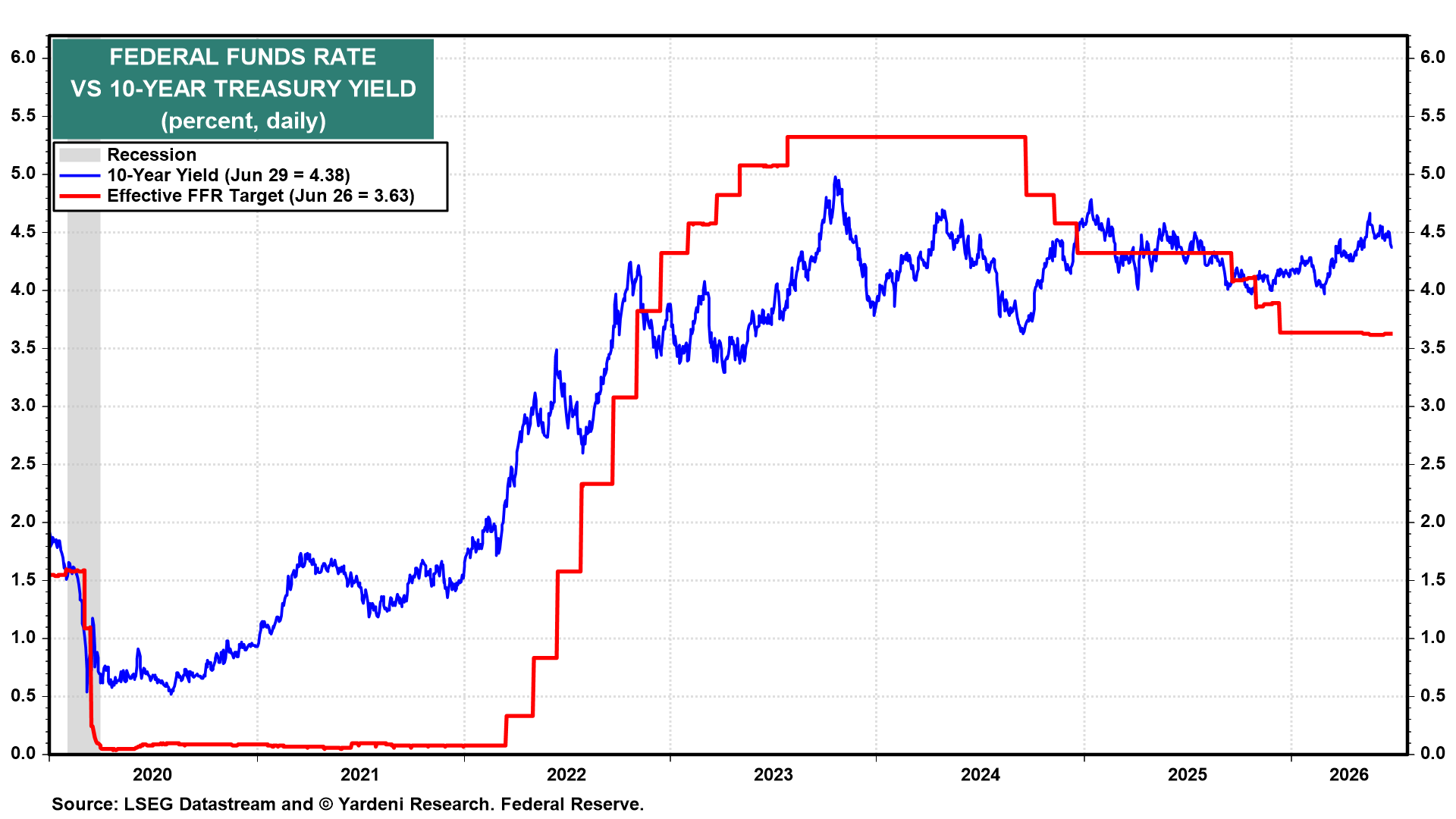

(1) Bond Vigilantes. Easing monetary policy does not always result in lower borrowing costs. When the Fed started its latest rate-cutting cycle during September 2024, we warned that easing into a resilient economy with entrenched inflationary pressures would incite the Bond Vigilantes. It did. Since then, the policy rate has fallen 175bp, yet the 10-year Treasury yield has risen from 3.70% to 4.38% (chart).

Mortgage rates also rose, following the lead of the Bond Vigilantes rather than the Fed (chart).