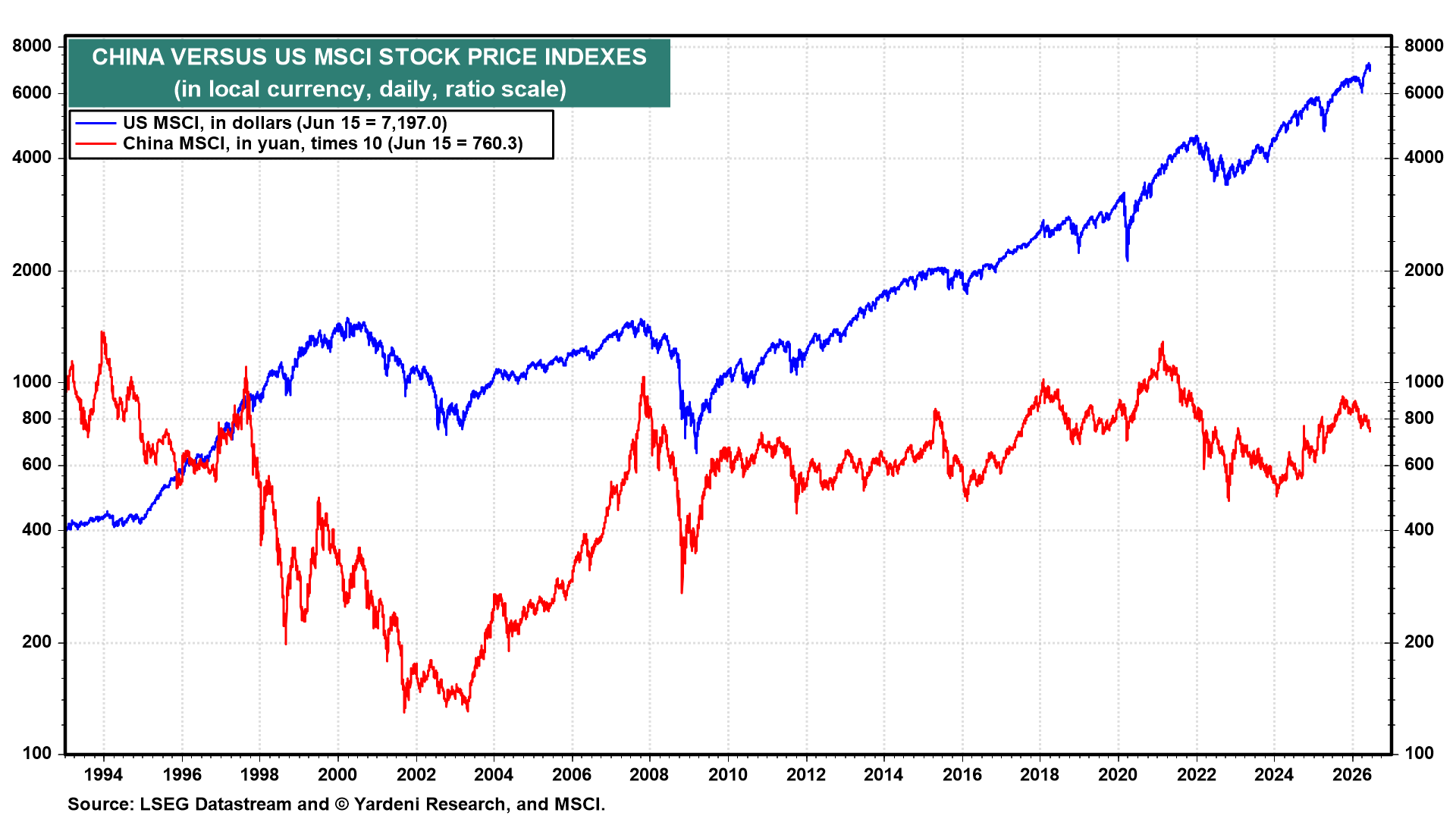

China has accomplished a great deal over the past few decades, transforming from a poor, insular, and rural economy to the world's second-largest economy. Its transformation has been hailed as an economic miracle. Yet this miracle hasn't been reflected in China's stock market. The China MSCI stock price index has been flatlining since the end of the Great Financial Crisis (GFC) in 2010. Over this same period, the US MSCI has increased sevenfold (chart)!

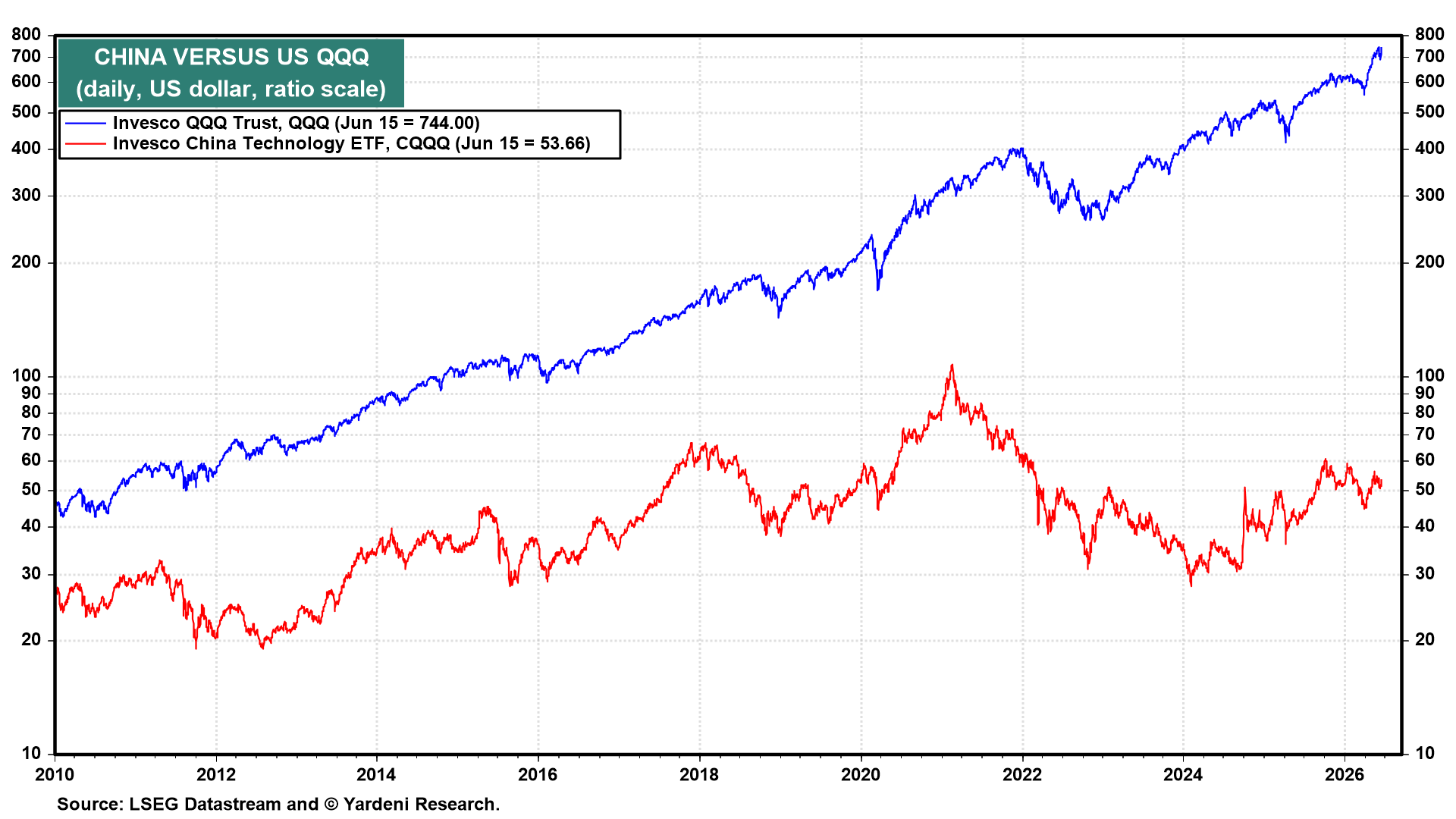

The same underperformance is visible in the Invesco China Technology ETF (CQQQ), which has been flat since the GFC (chart). Over the same period, Invesco's QQQ ETF--which tracks 100 of the largest US domestic and international non-financial companies listed on the Nasdaq Stock Market based on market capitalization--is up seventeenfold!

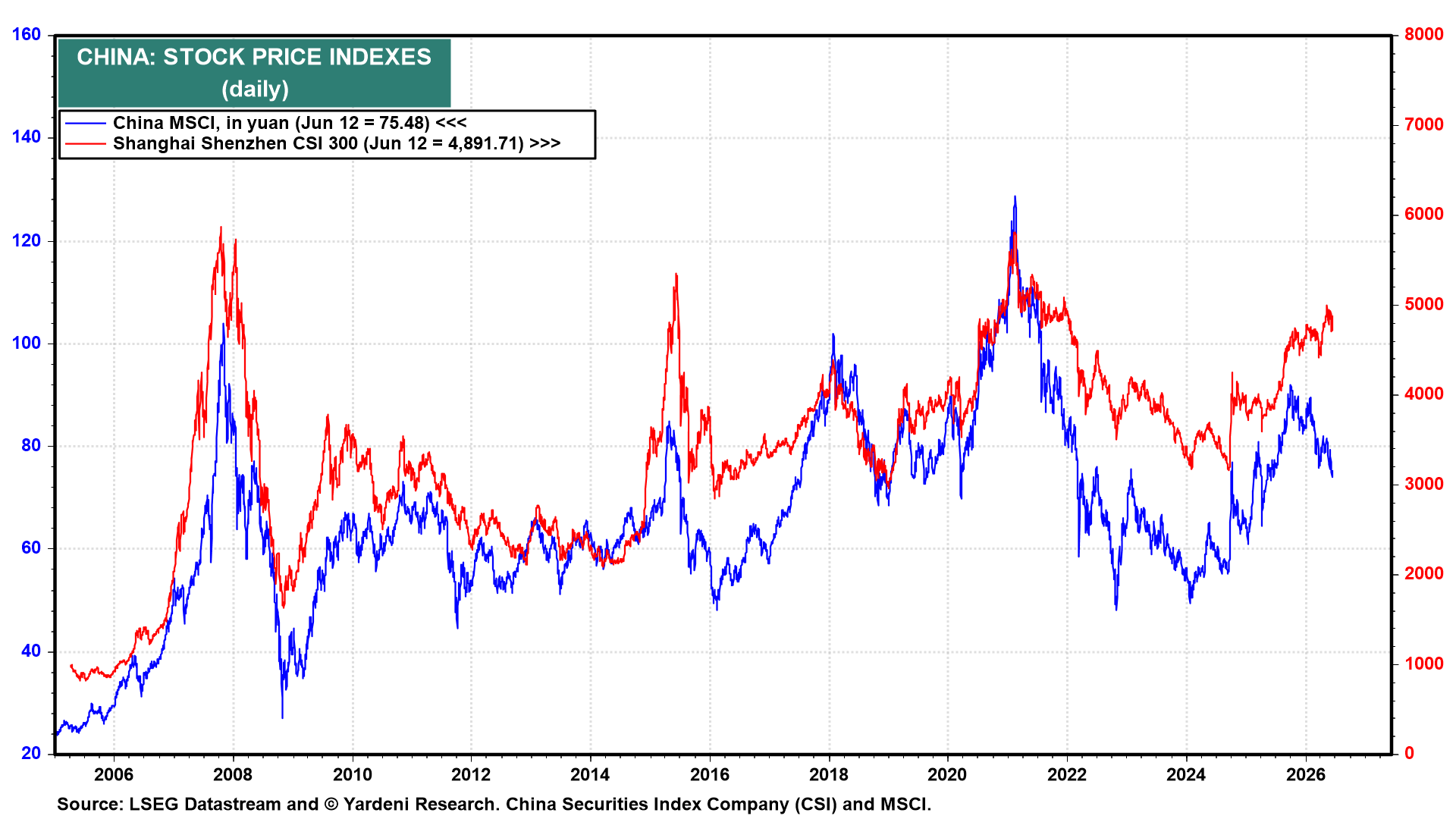

Meanwhile, the other major Chinese benchmark stock market indexes show that Chinese equities have been good for short-term trading, but not for long-term investing (chart).

Let's have a closer look at some of the fundamentals that account for the underperformance of Chinese stocks compared to US stocks:

(1) Why China lacks mojo. The divergence has occurred because China has an authoritarian command economy, while the US has an entrepreneurial capitalistic economy. US entrepreneurs are far freer to innovate, take risks, and prosper. Their Chinese counterparts operate under a government that tightly limits their freedom to run their enterprises optimally and to accumulate private wealth (and power).

Much of China's prosperity since the 1970s occurred during periods when the government allowed capitalism to flourish. Under President Xi Jinping, the government increasingly imposed authoritarian and arbitrary economic policies to maintain its control and to limit the power of entrepreneurs.

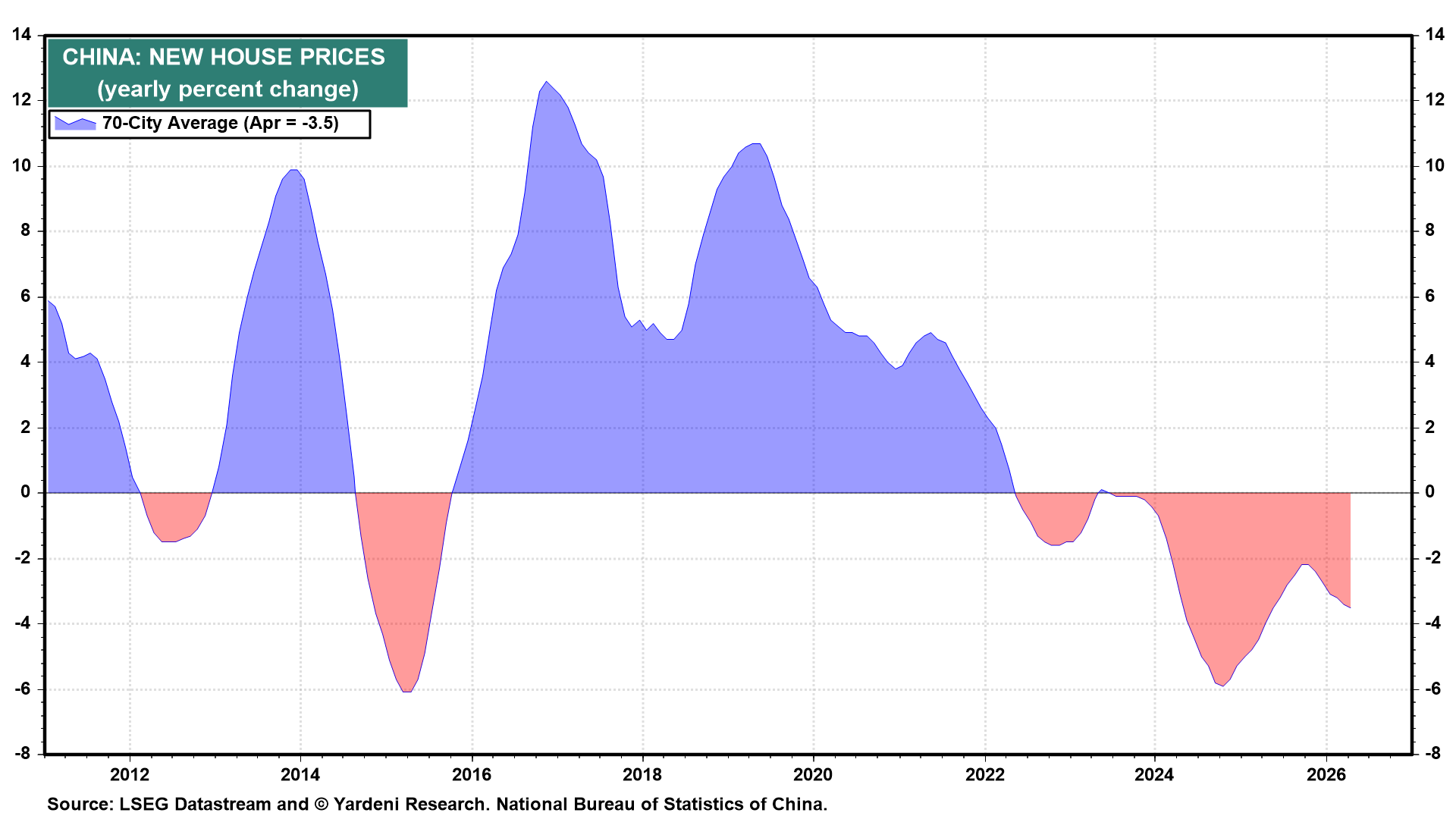

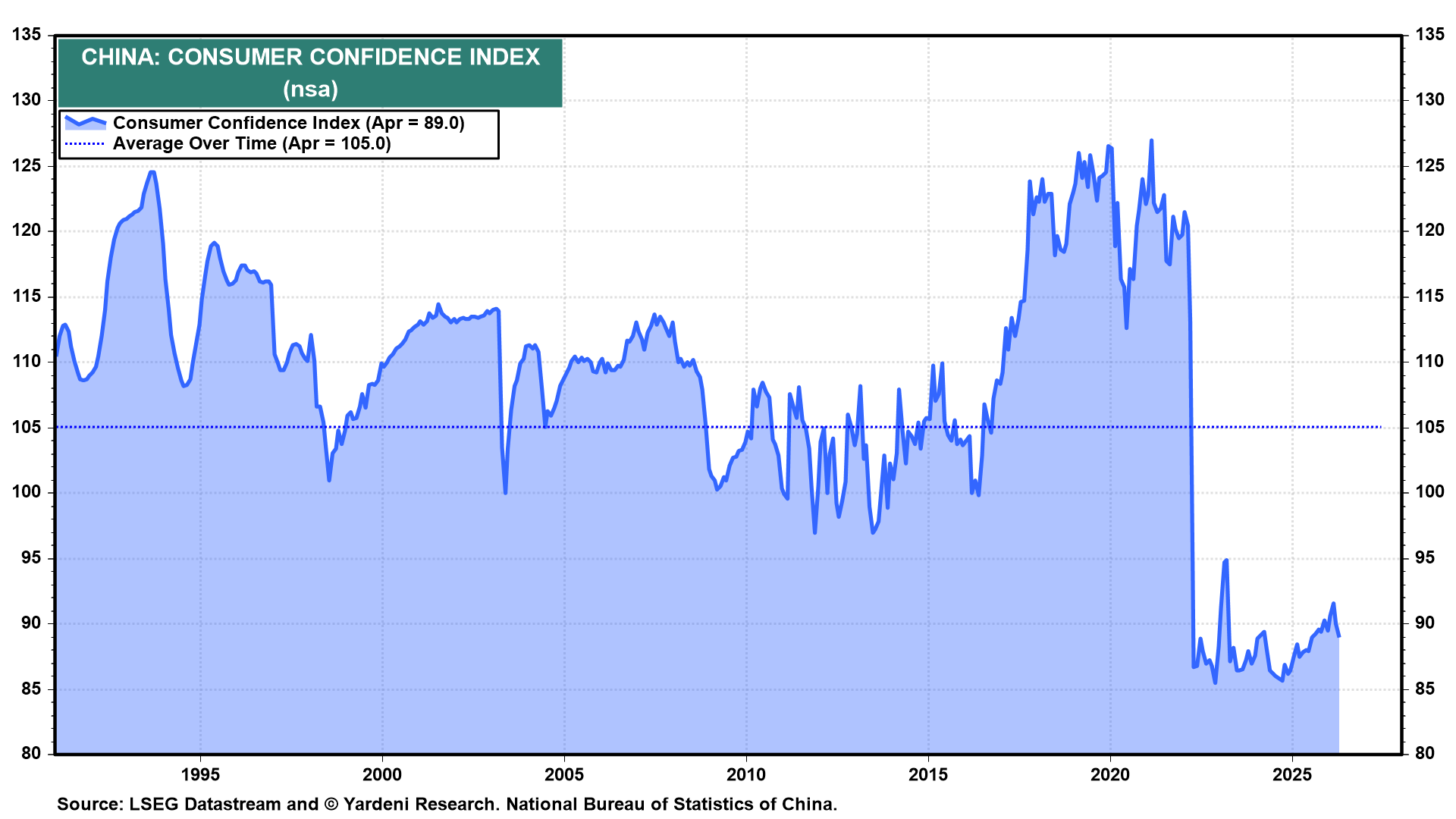

On the other hand, the government did nothing to stop the formation of a huge speculative bubble in the property market during the 2010s. When it burst, it caused a huge negative wealth effect that has been depressing consumer confidence and spending in recent years (charts).

Consumer confidence crashed during the pandemic in China and has yet to recover (chart).

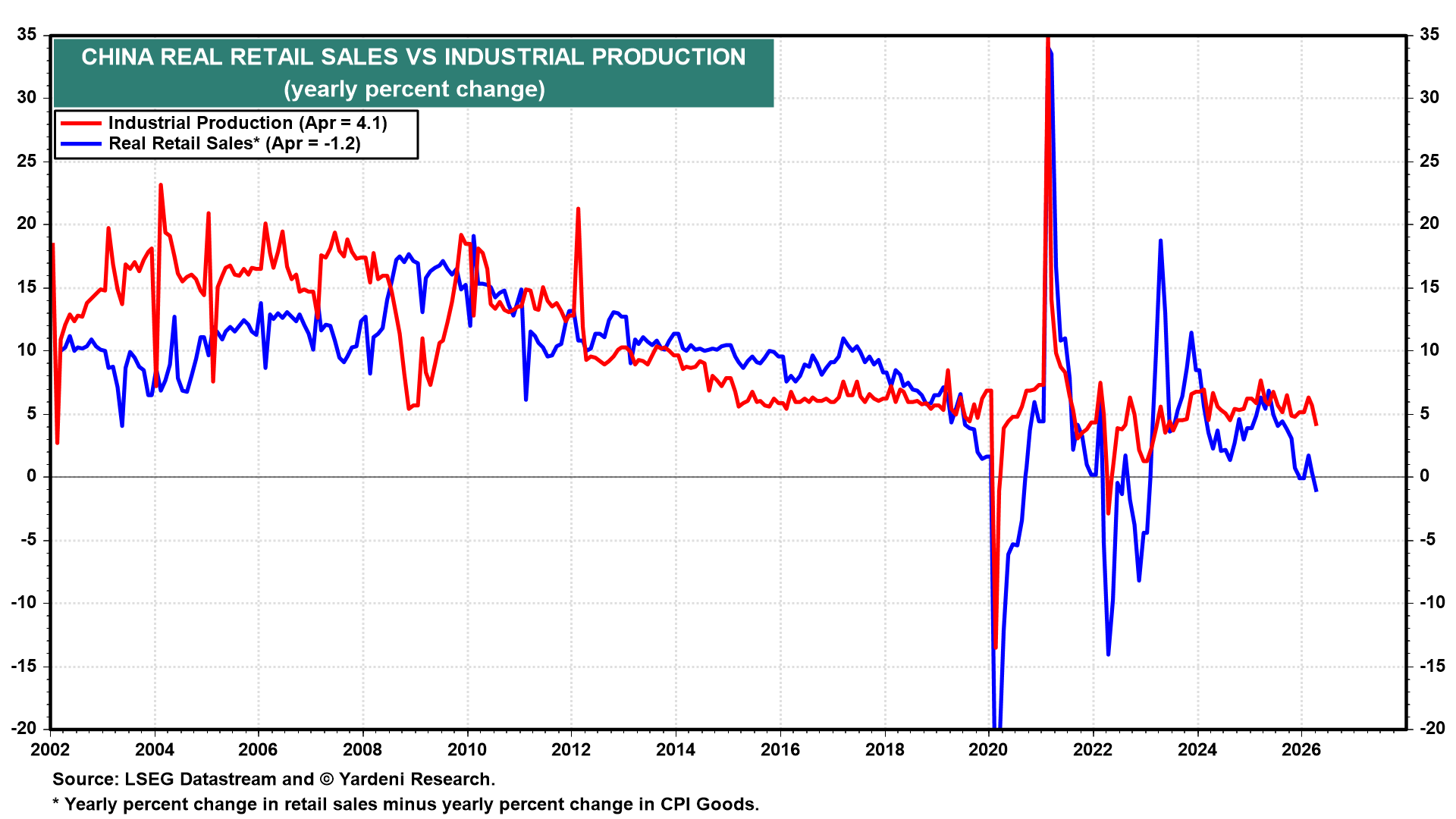

That negative wealth effect is evident in China's real retail sales growth, which has been declining on a y/y basis in recent years and was down -1.2% in April (chart). This is the first time real retail sales growth has been negative when excluding the pandemic years. Sluggish domestic demand has, in turn, created significant excess industrial capacity. Industrial production rose 4.1% y/y in April.

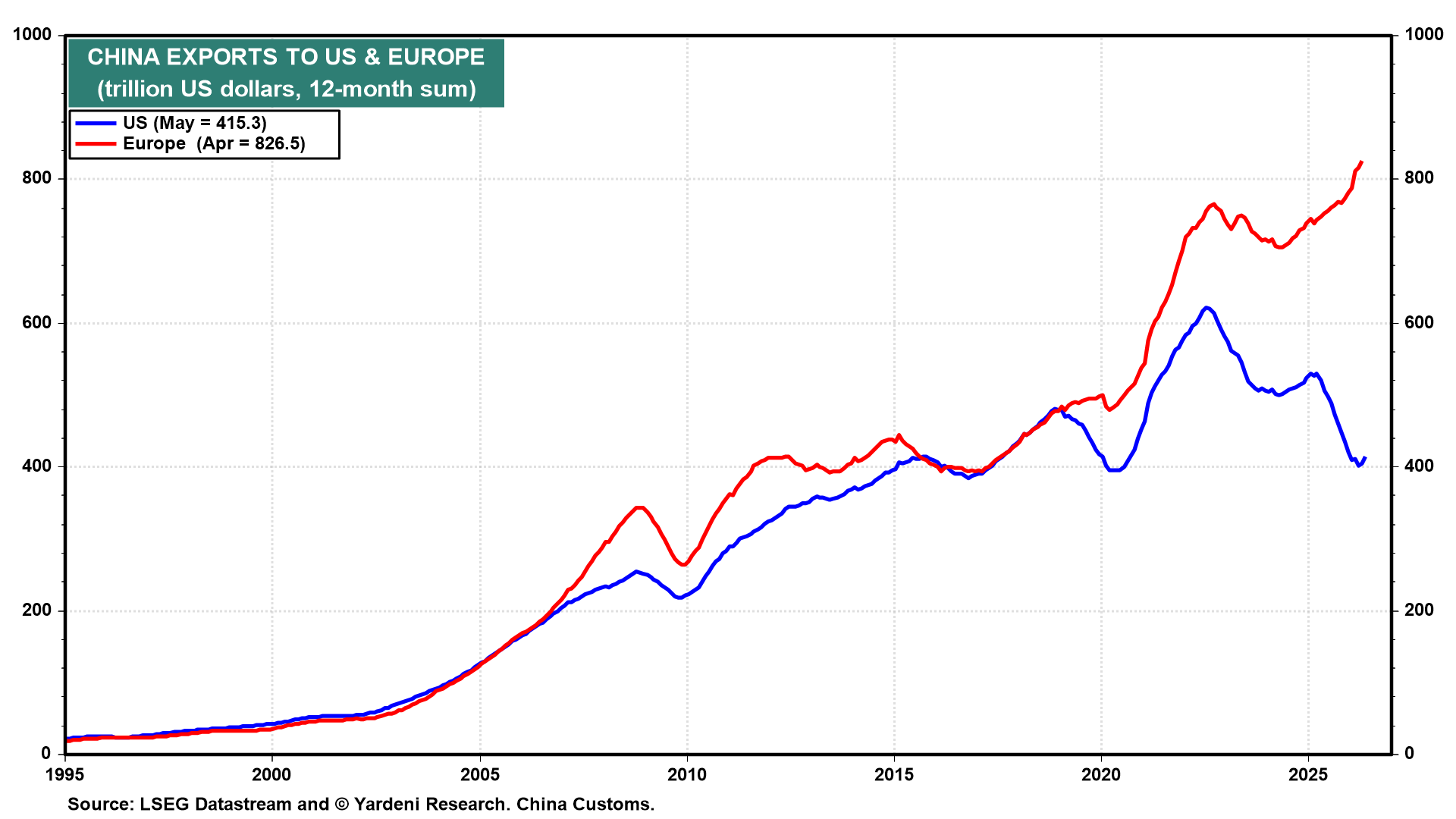

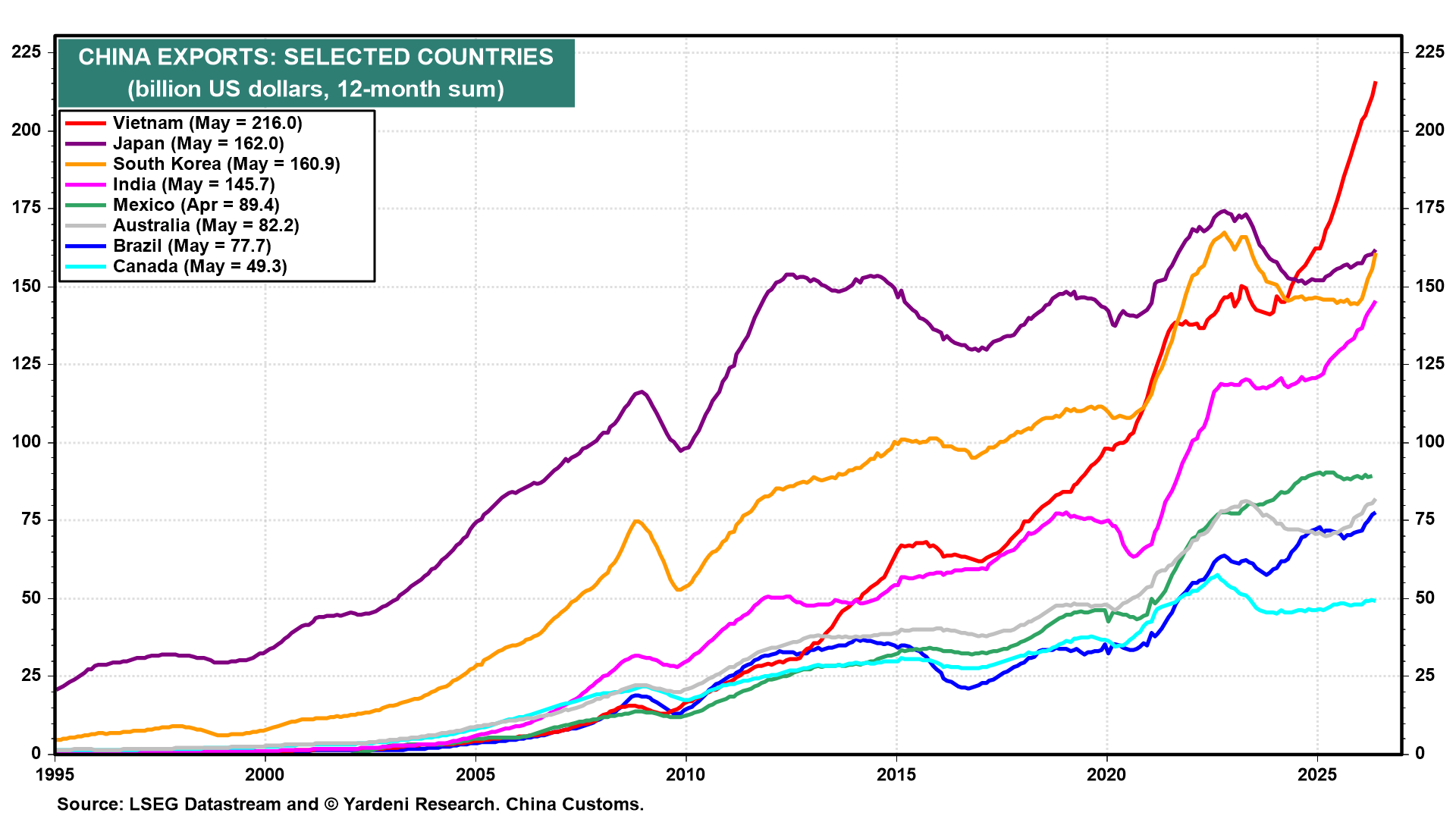

To absorb that excess capacity, China has been aggressively increasing exports to Europe. Meanwhile, US tariffs have significantly curtailed Chinese exports to the US in recent years(chart).

Chinese manufacturers have been circumventing US tariffs by routing shipments through countries with lower tariffs, particularly Vietnam (chart).

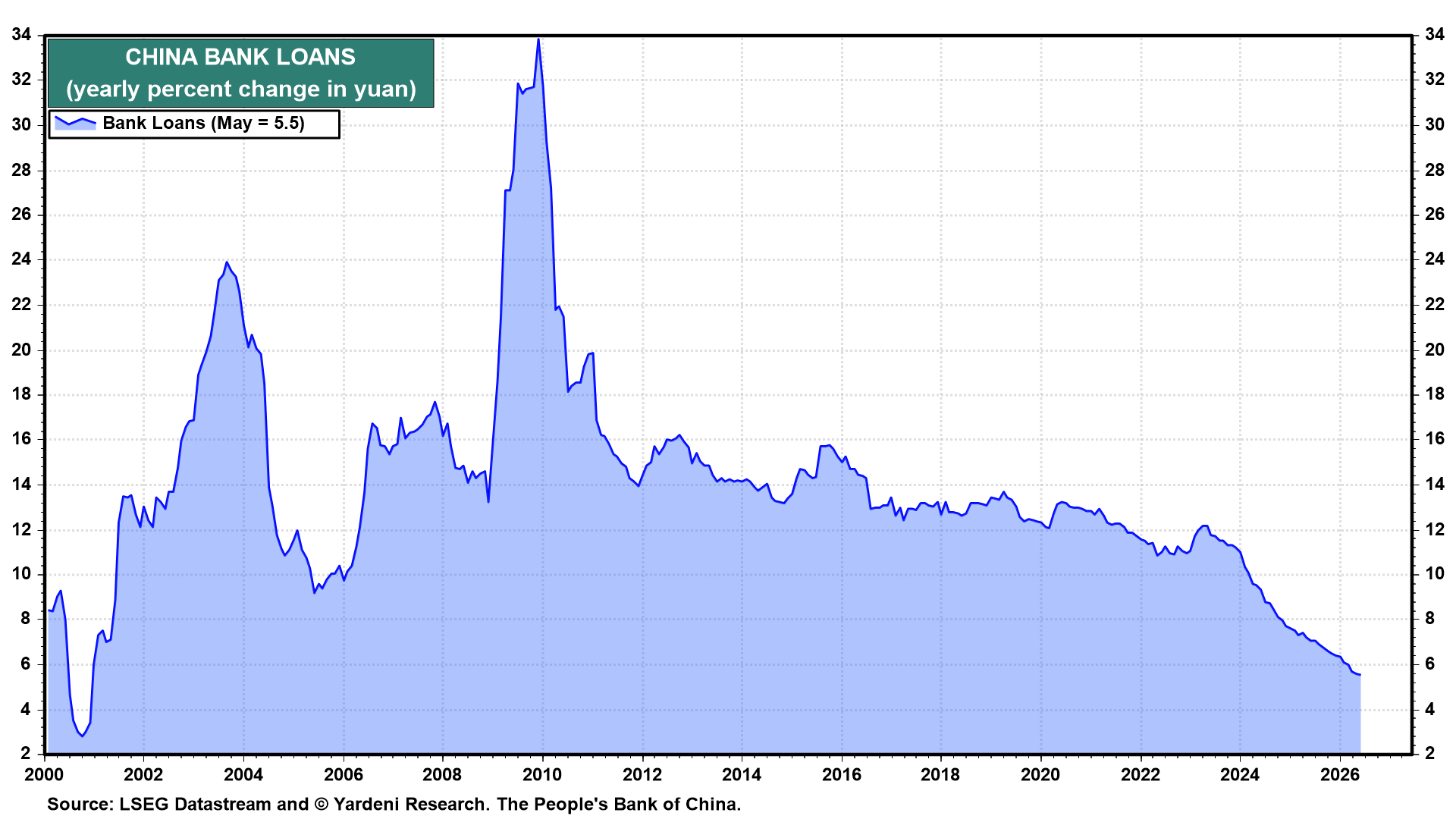

The weakness in China's domestic demand is further confirmed by bank loan growth, which dropped to 5.5% y/y in May, the lowest since 2001 (chart).

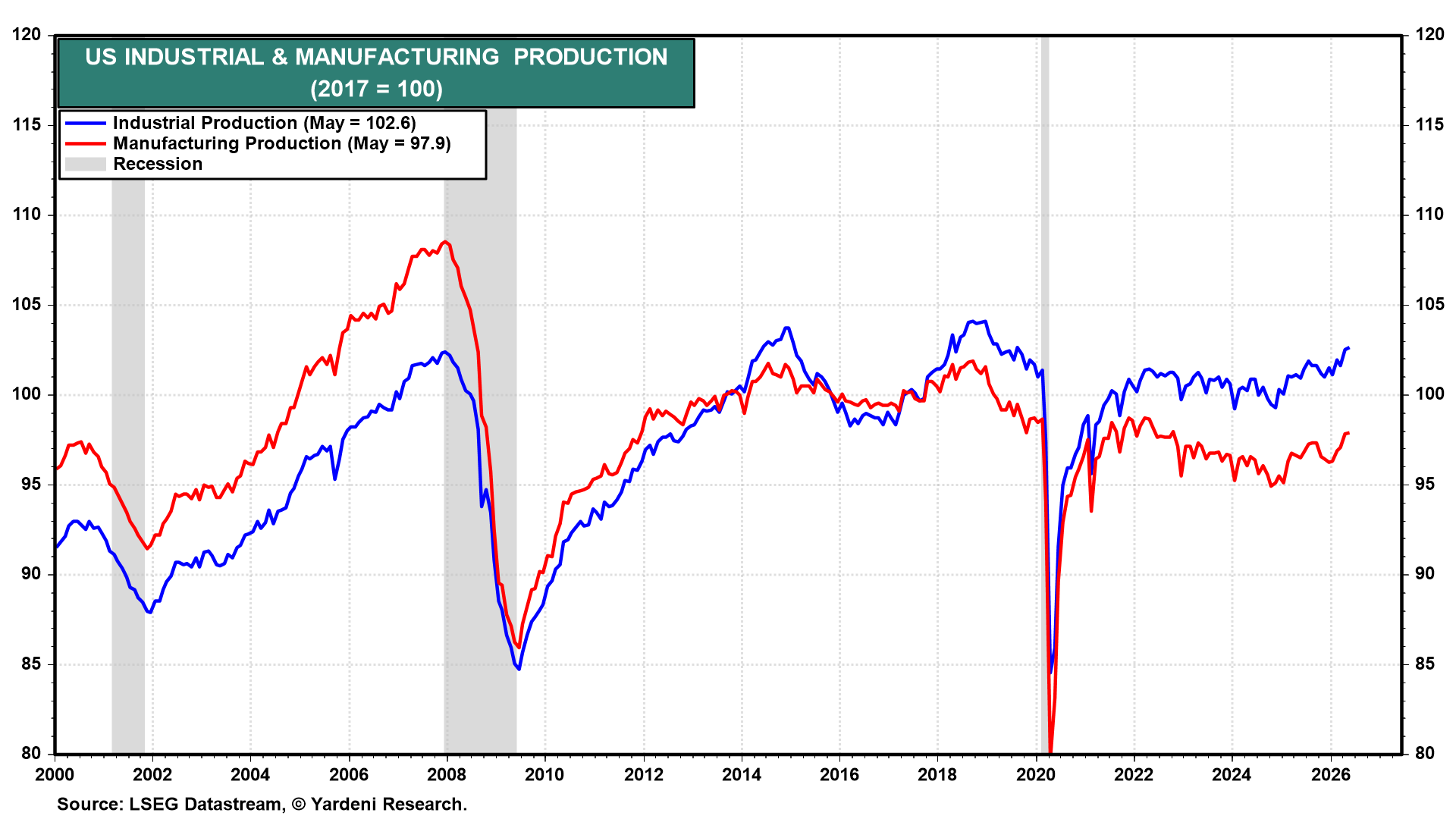

(2) Why the US has exuberance. Today's US industrial production report for May shows some of what's fueling exuberance in the US. After stagnating for much of the pandemic, industrial production has been rising since mid-2024 (chart).

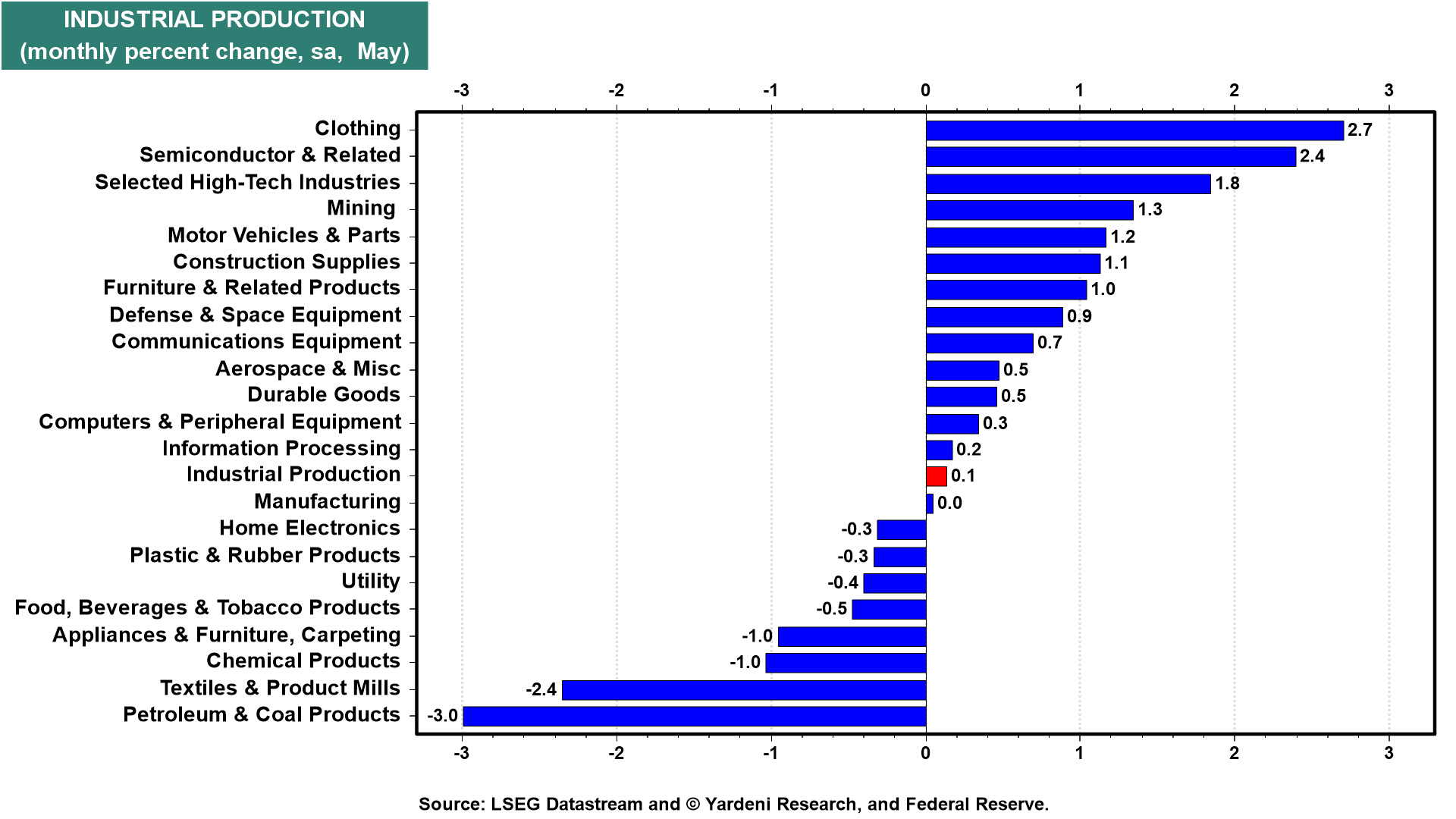

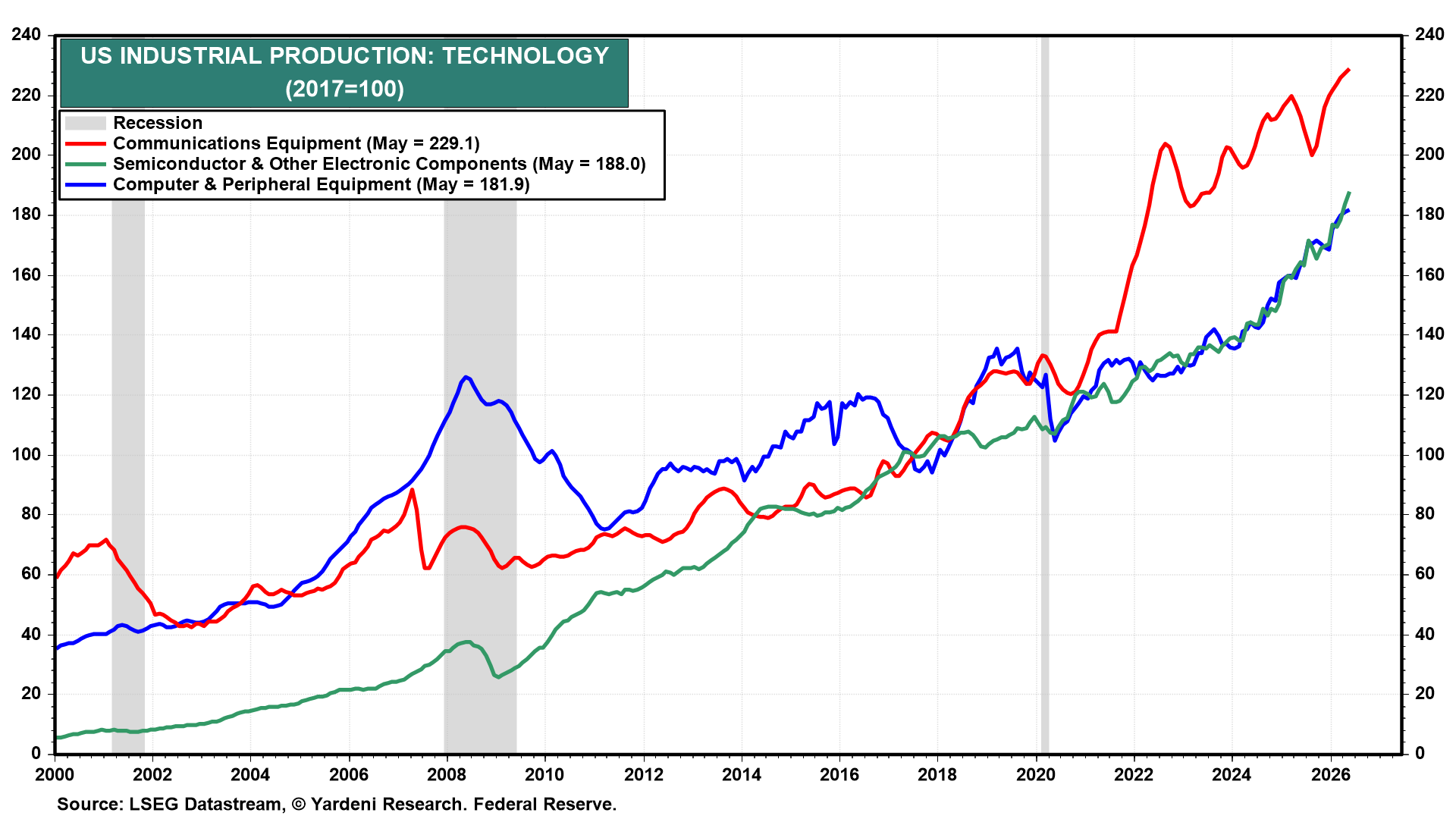

While the 0.1% m/m gain in May was modest, the AI buildout is a durable secular tailwind that should keep industrial production on an upward trajectory. The industry breakdown confirms the AI footprint, with semiconductors and other technology industries among the primary growth drivers (chart).

The AI buildout is a crucial driver of the US economy. Since the release of ChatGPT in late 2022, industrial production of technology has accelerated meaningfully (chart).

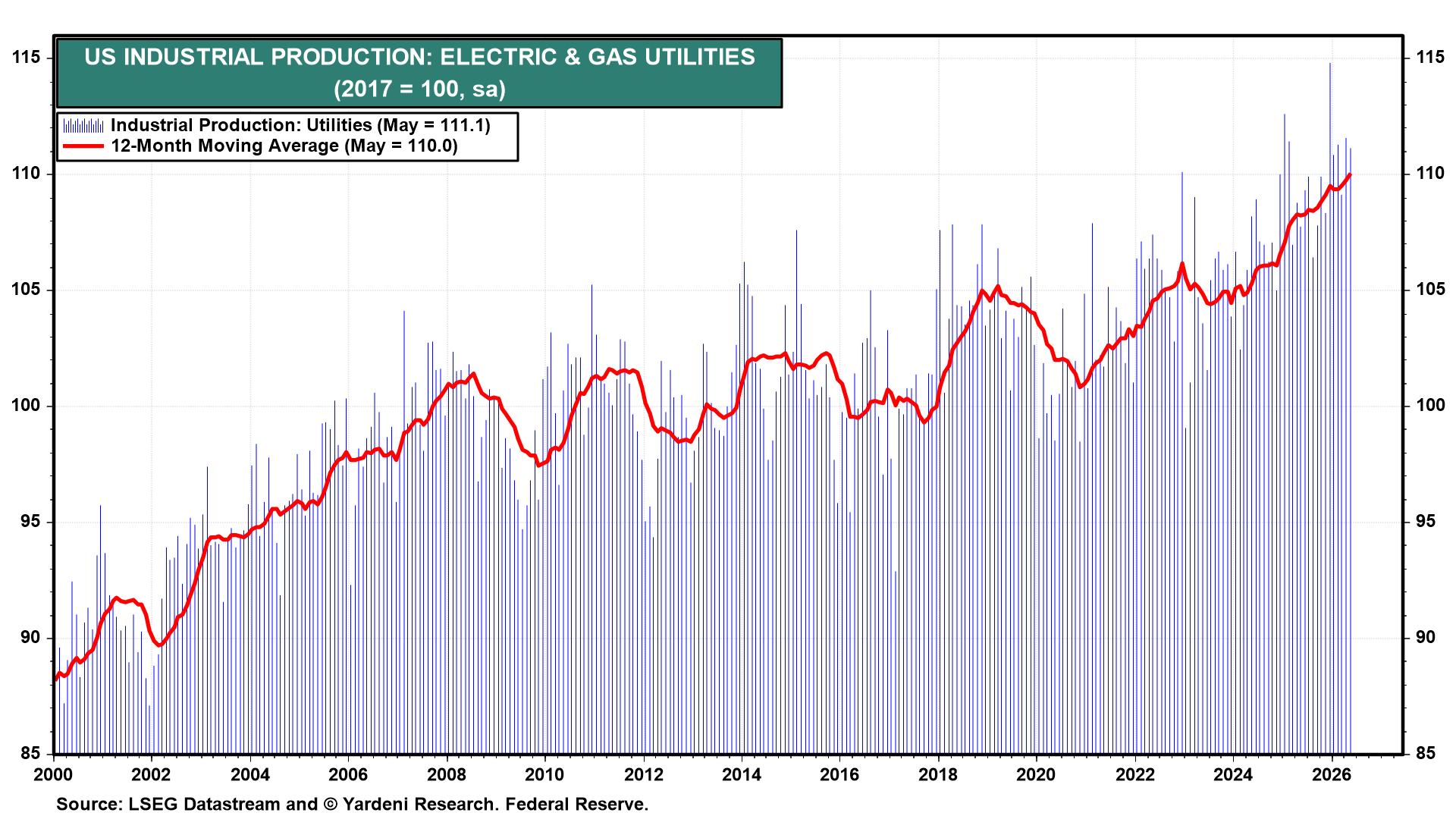

Two additional secular tailwinds reinforce the sunny economic outlook. First, electricity and gas utilities' output will continue to grow rapidly to meet the power needs of AI data centers (chart).

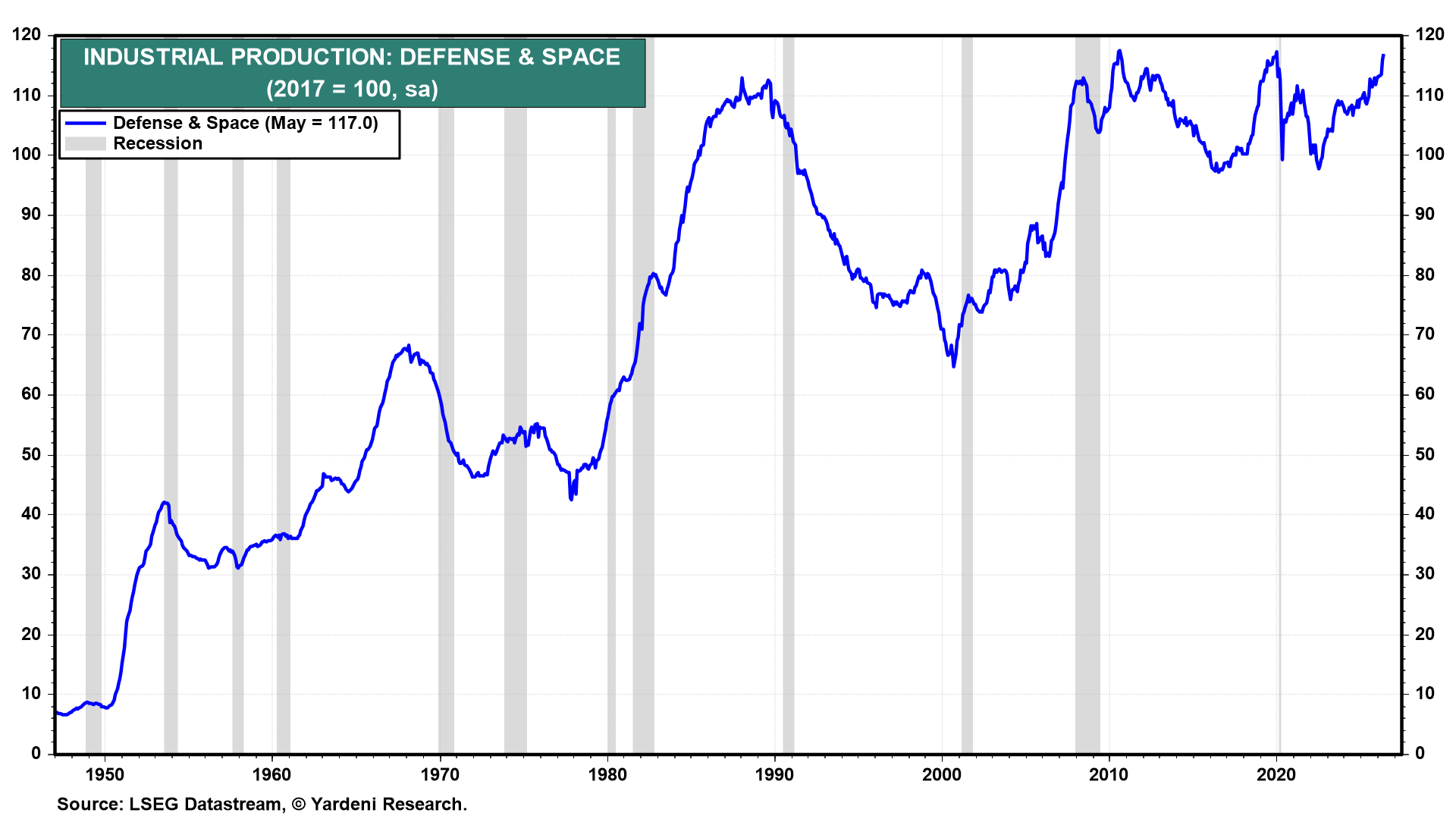

Second, the Trump administration is seeking to expand defense spending from $1 trillion this year to $1.5 trillion next year. Armaments must be replenished following recent military operations, and the relentless pace of technological advancement in the defense sector will be a persistent driver (chart).