The week ahead is chock-full of labor market indicators. In addition, nine Talking Fed Heads on the Federal Open Mouth Committee are on the speaking circuit, with Williams, Bowman, and Goolsbee coming up twice. Despite the elevated oil prices, the stock market continues to levitate to new highs. The price of a barrel of West Texas Intermediate crude hit $110.10 intraweek and closed on Friday at $102.48. Brent crude hit as high as $120.65 during the week and closed at $108.72. The S&P 500 finished the week at another record high regardless.

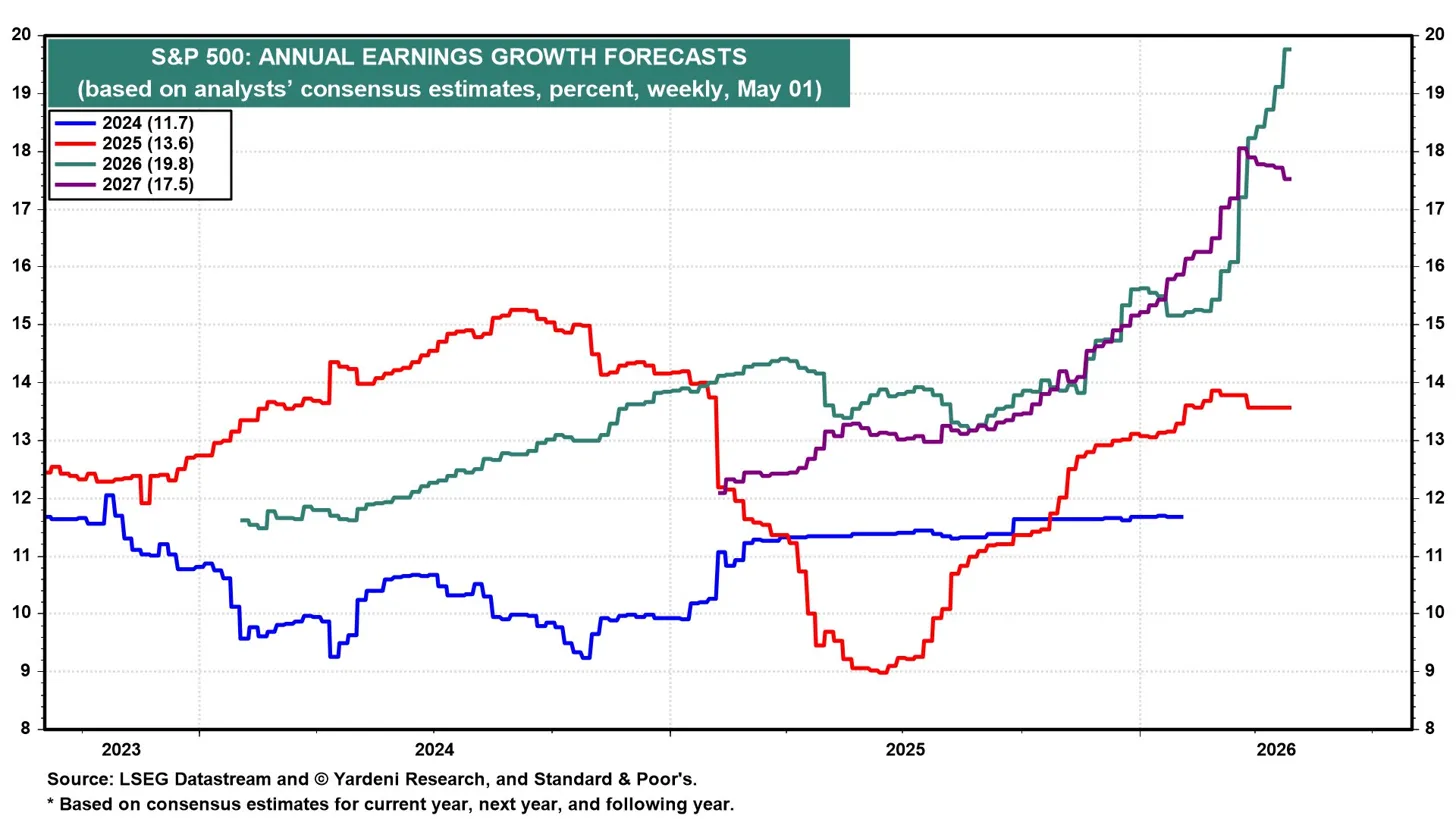

The Q1 earnings reporting season is going strong. Roughly 44% of S&P 500 companies reported results last week. Big names scheduled to report this week include Palantir, AMD, McDonald's, and Arm. The industry analysts' consensus forecast for S&P 500 companies’ aggregate earnings growth in 2026 has climbed to 19.8%, well above the 11.7% and 13.6% figures posted in 2024 and 2025 (chart). The double-digit marathon should continue in 2027, with the analysts collectively forecasting a 17.5% gain. They certainly are in sync with our Roaring 2020s narrative!

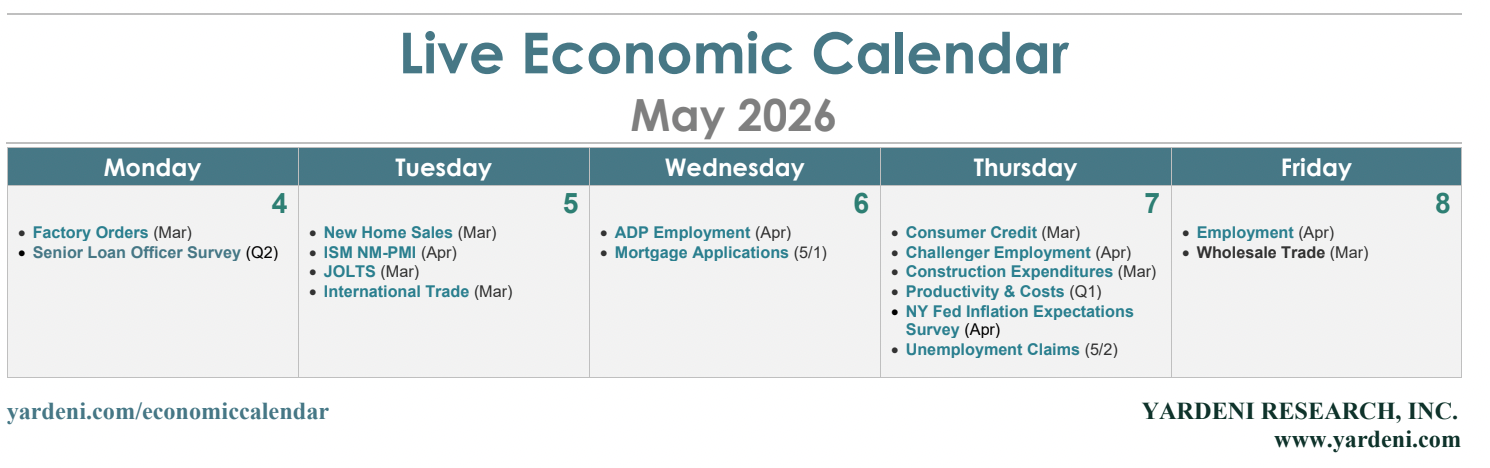

With that said, let's take a look at the key releases most likely to shape investors' thinking on business activity, the state of the consumer, the labor market, and inflation this week:

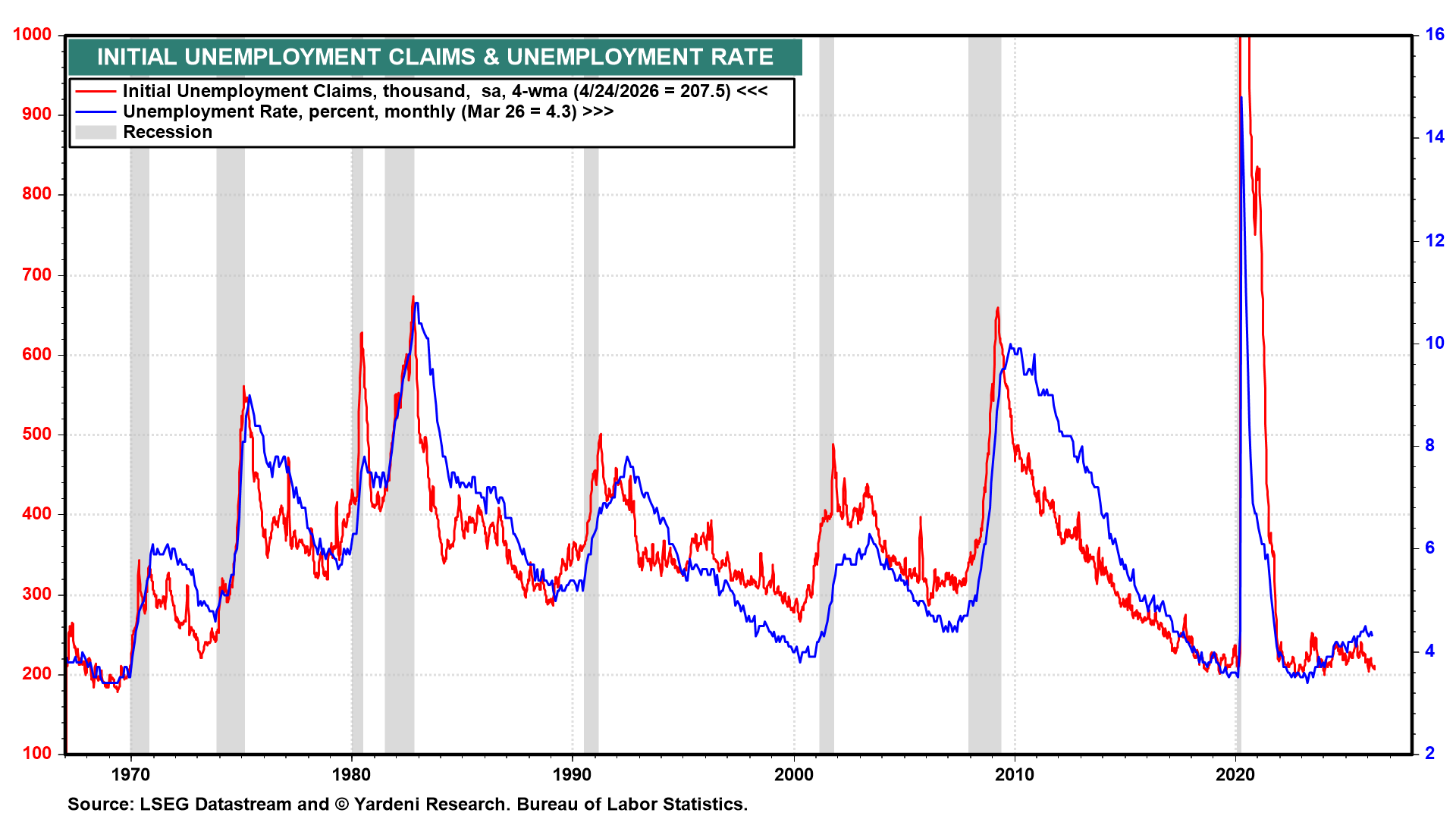

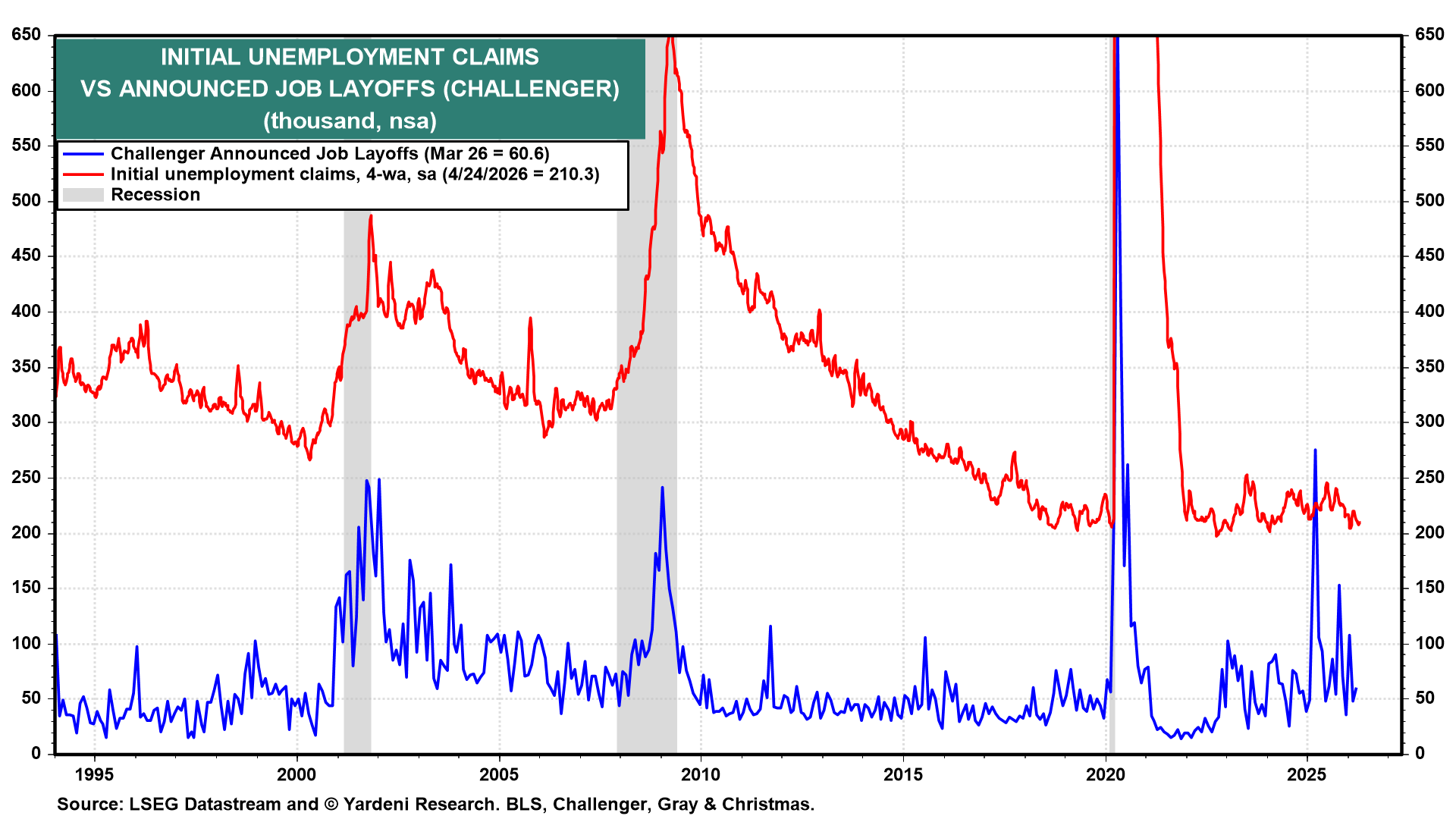

(1) Employment. April's employment report (Fri) is the headliner for the week. The unemployment rate is likely to tick down to 4.2% based on its relationship with initial unemployment claims (Thu), which have been falling in recent weeks (chart).

Jobless claims also suggest that the Challenger measure of layoffs (Thu) remained low in April (chart).

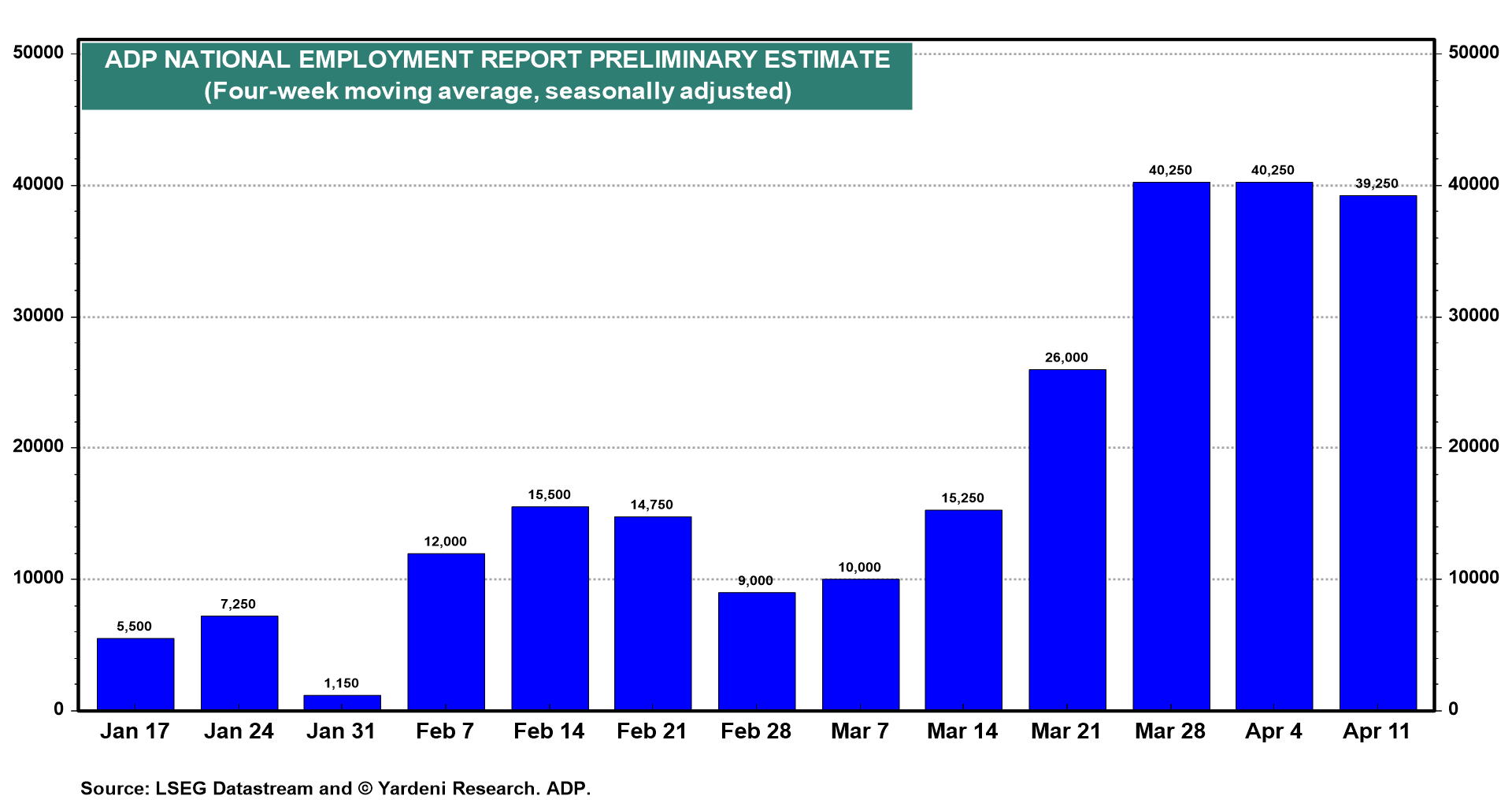

The ADP weekly employment report suggests that the monthly report (Wed) for April will show a solid increase in private industry payrolls (chart).

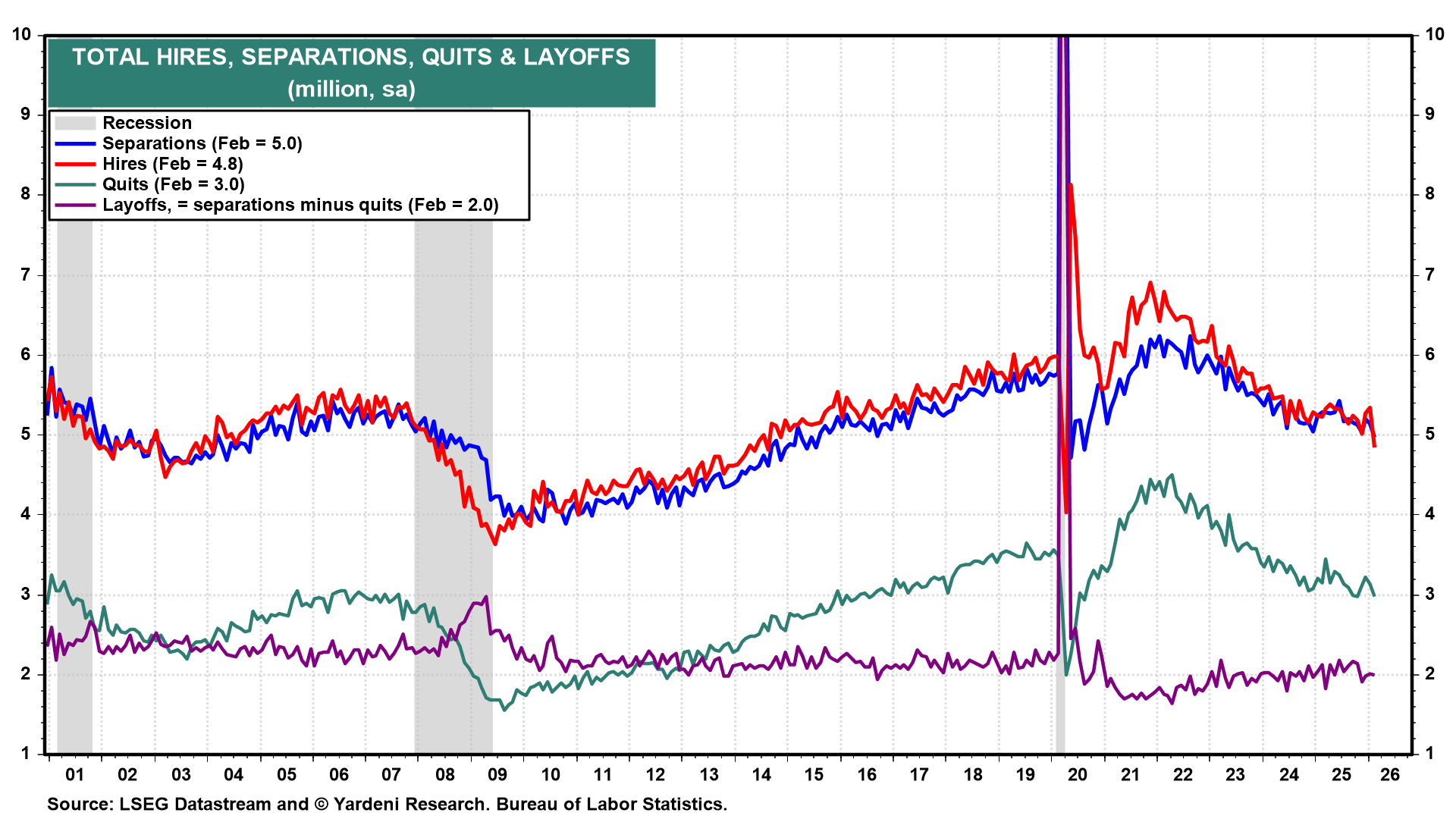

March JOLTS data (Tue) are unlikely to differ much from February's results (chart). We do expect to see more job openings and hiring activity in April based on the recent decline in jobless claims and increase in ADP weekly payrolls.

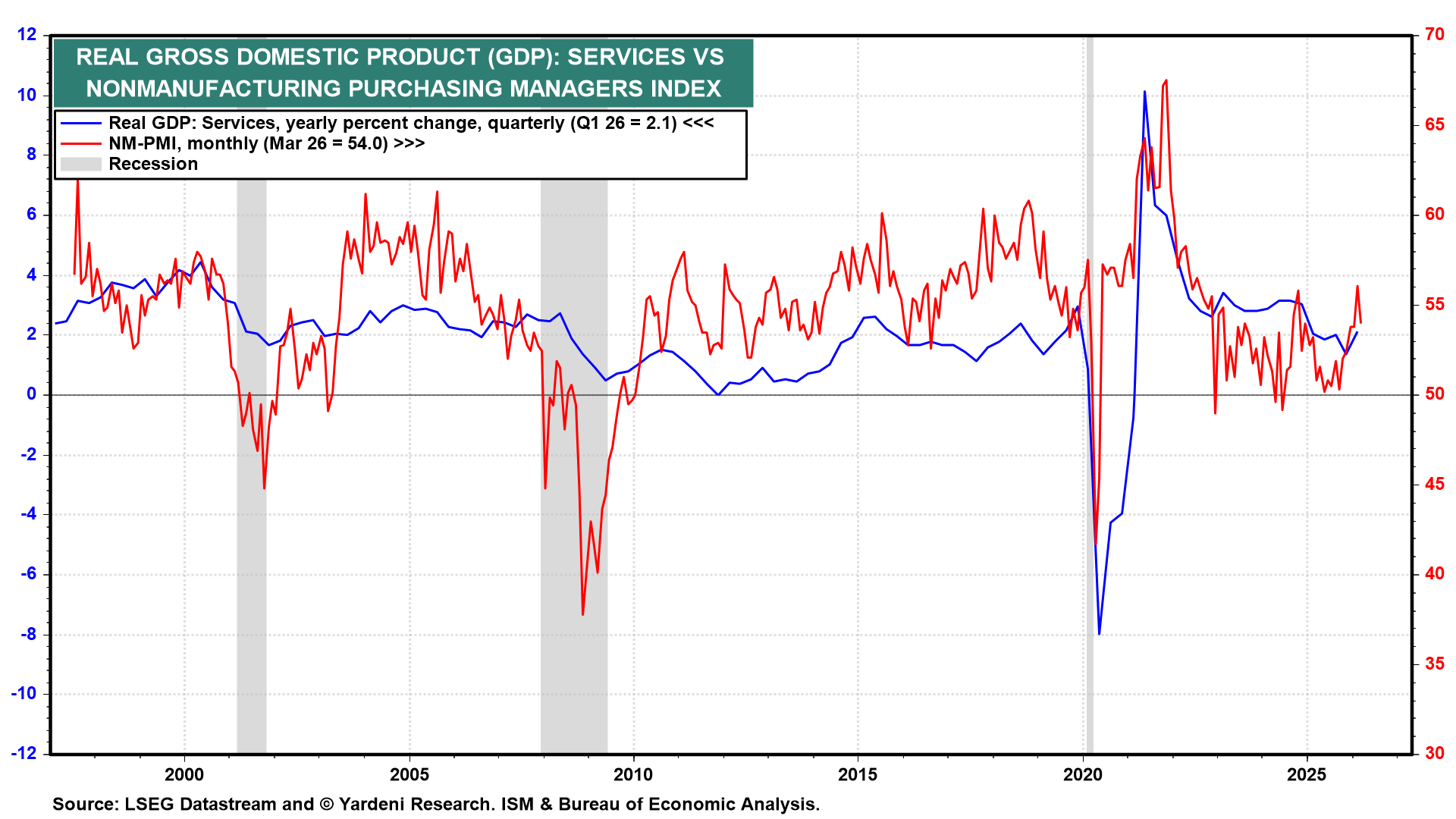

(2) ISM NM-PMI. April's ISM NM-PMI (Tue) should remain solidly above 50.0, confirming the strength posted during February and March. Real services GDP grew 2.1% y/y in Q1, and the recent NM-PMI readings are consistent with continued expansion (chart).

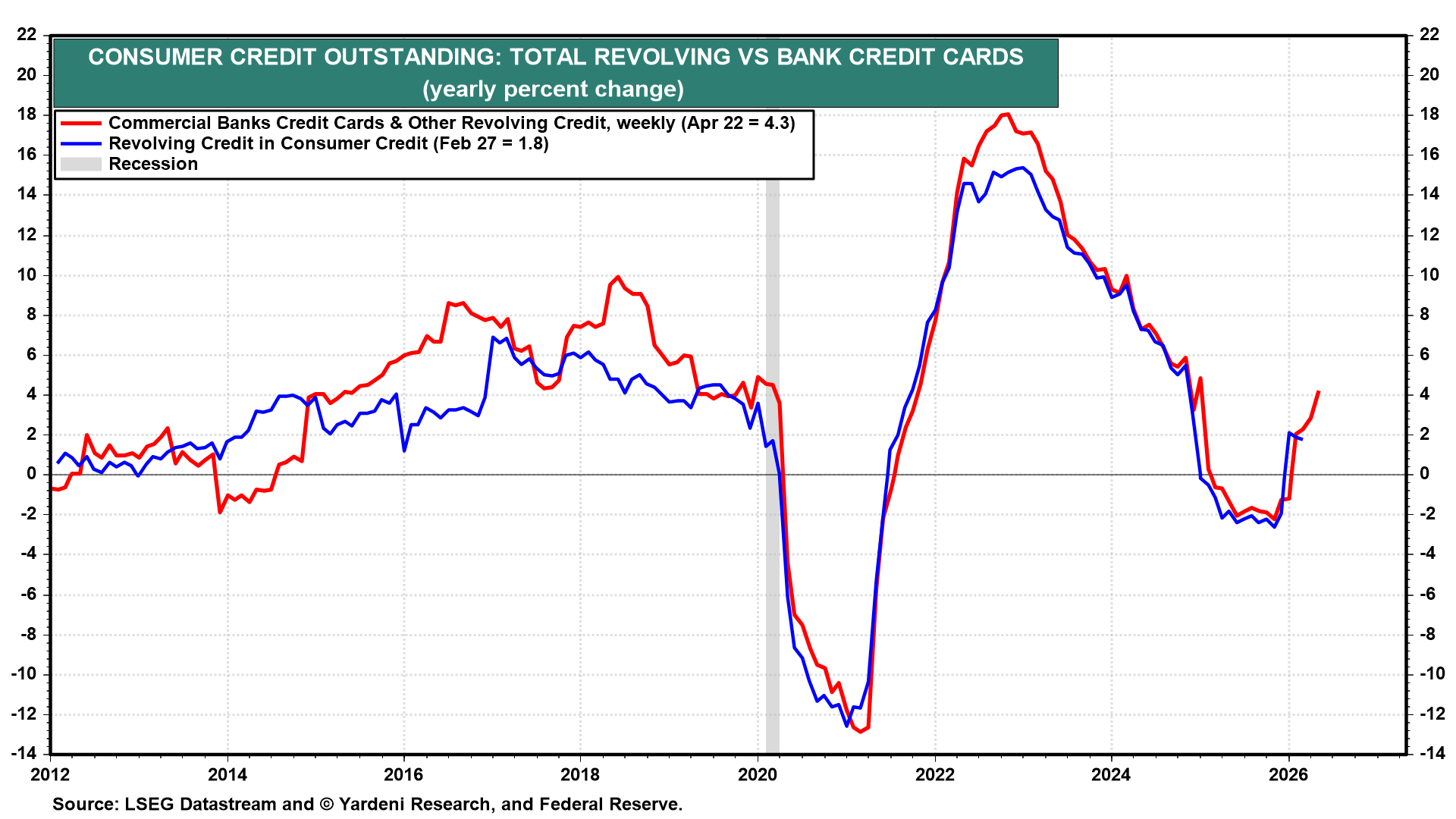

(3) Consumer credit. March consumer credit (Thu) data are likely to show a strong increase in revolving credit, based on comparable weekly data for commercial banks (chart).

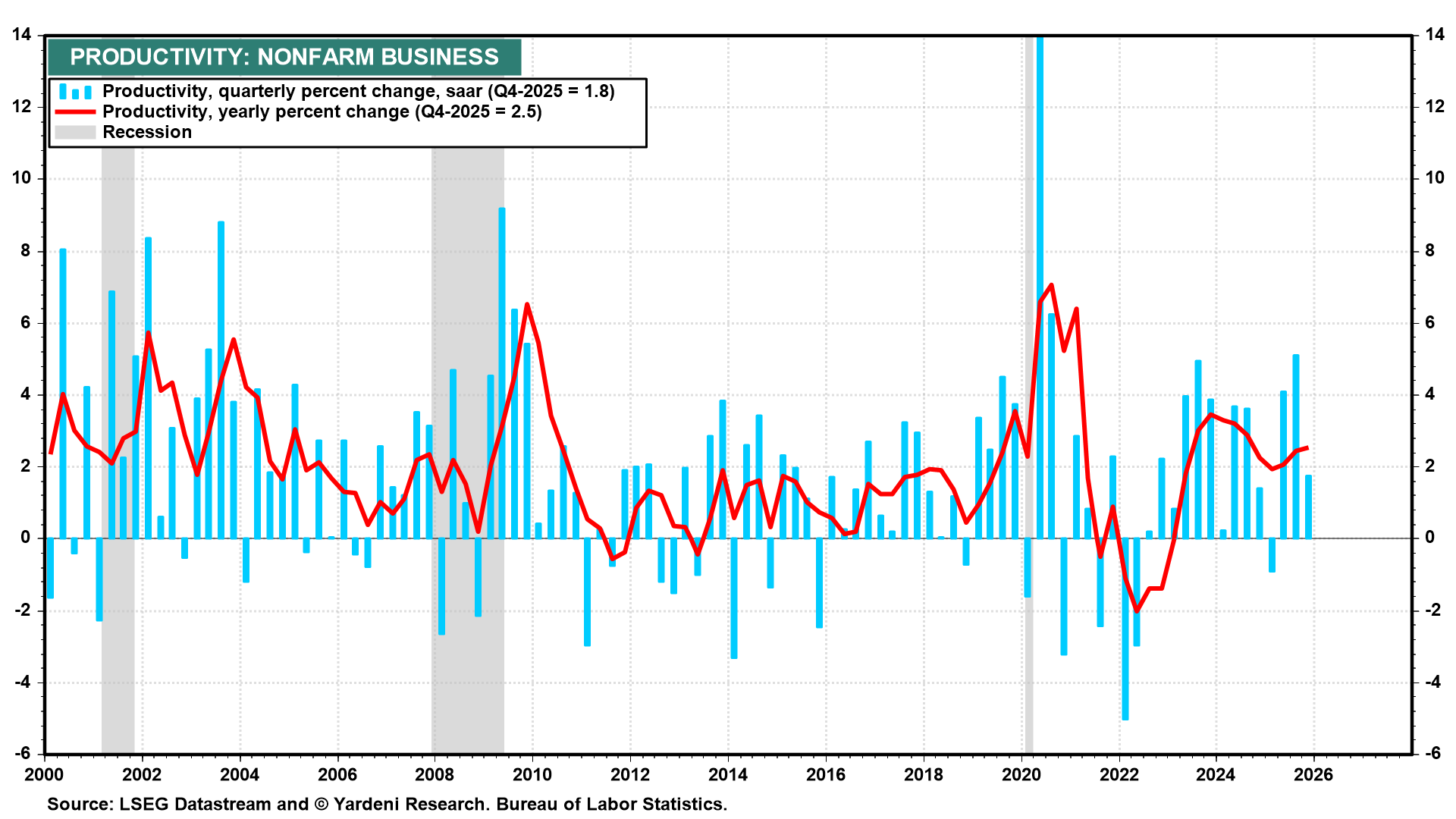

(4) Productivity and unit labor costs. Q1-2026 nonfarm productivity (Thu) should show a weak increase close to the 1.8% q/q (saar) gain during Q4-2025 (chart).

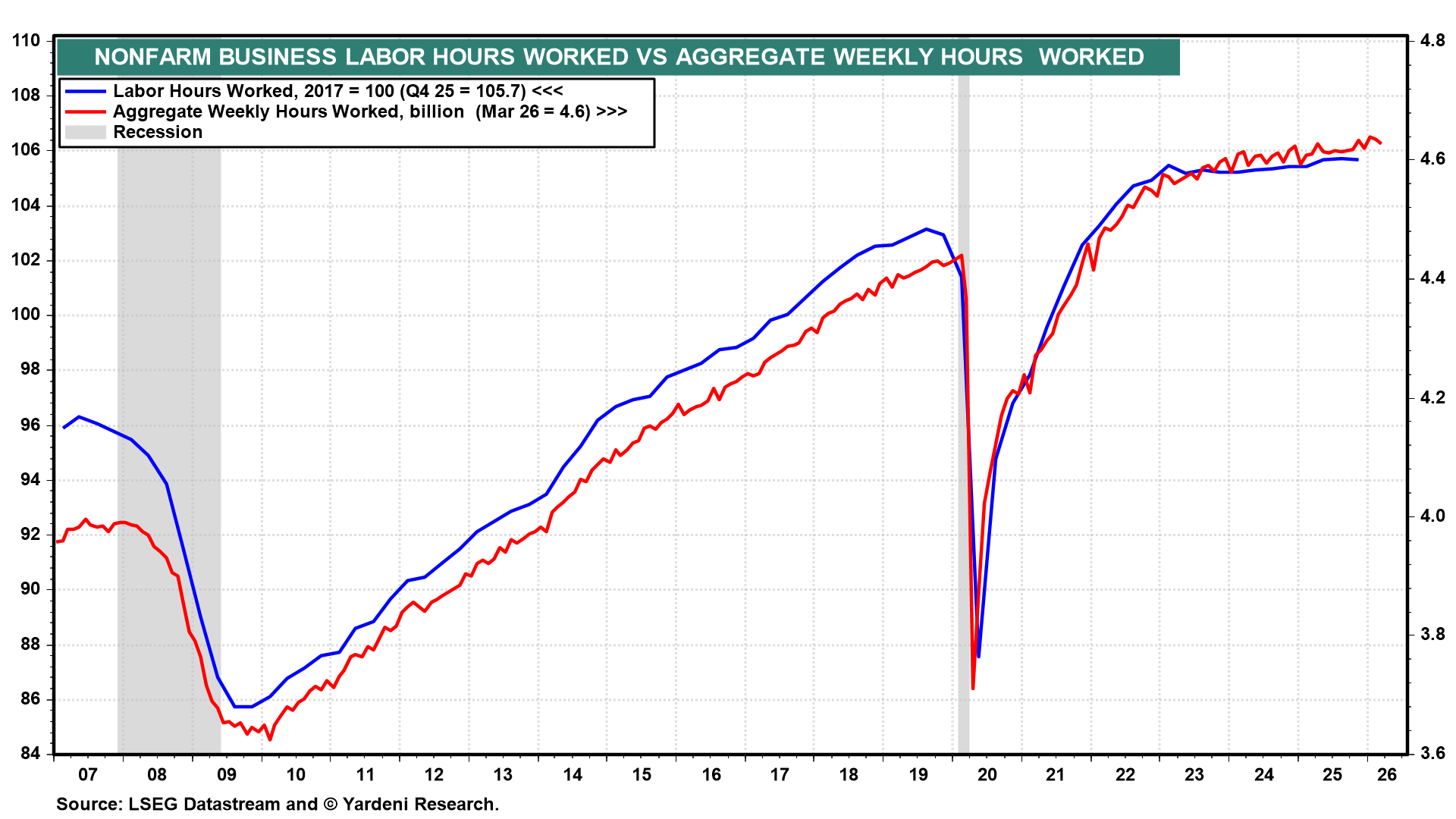

Real GDP rose 2.0% during Q1, while labor hours worked increased by much less (chart). That implies that productivity rose by less than 2.0%.

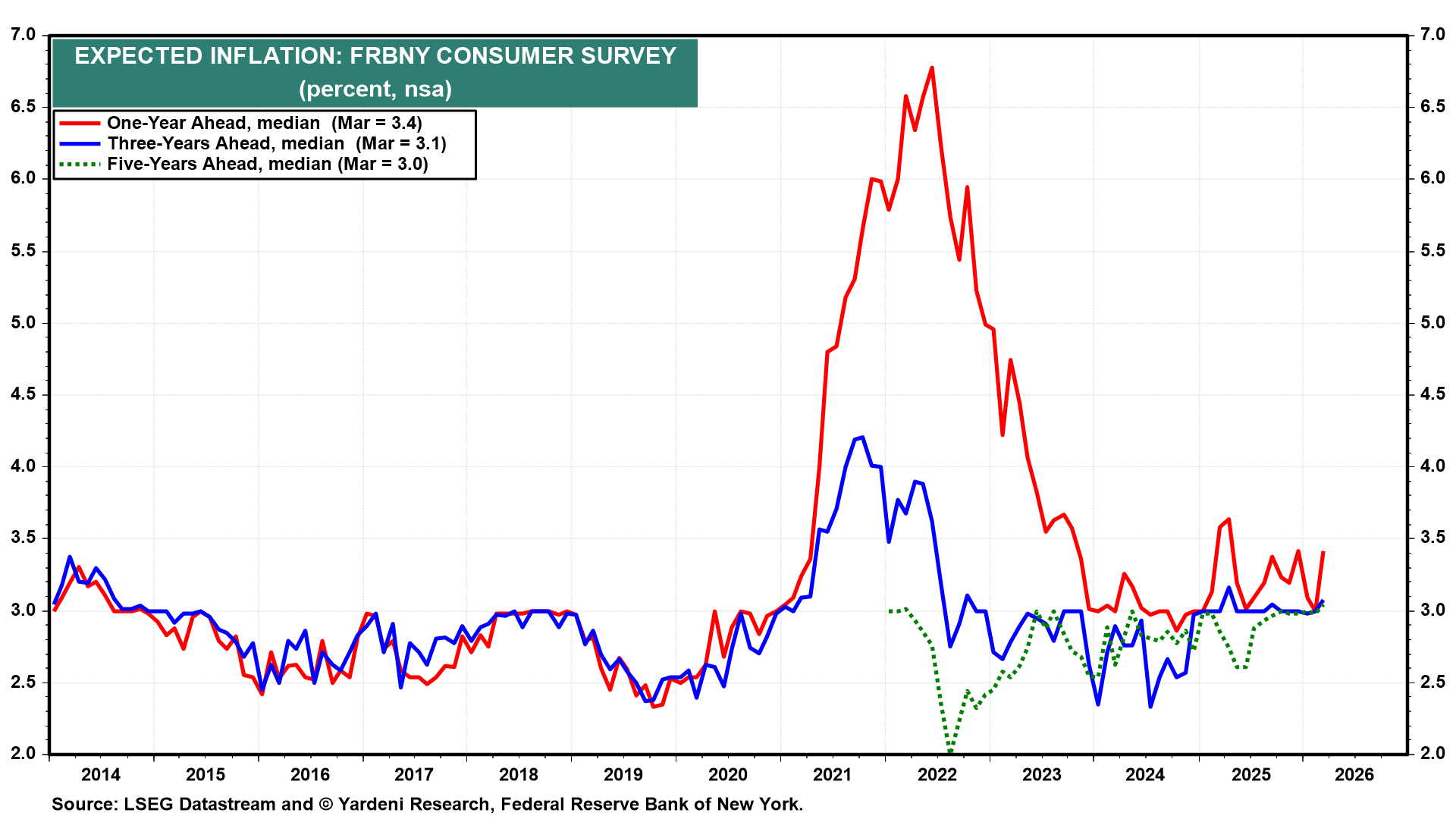

(5) NY Fed inflation expectations. The NY Fed's Inflation Expectations release (Thu) for April is likely to show a jump in the year-ahead measure closer to 4.0%, up from 3.4% in March (chart). That should reflect higher gasoline prices.