As we’ve flagged in recent weeks, an end to the conflict in the Middle East should see many foreign stock markets outperform the US. Lower oil prices reduce global inflationary pressures, give central banks room to ease policy, and tend to benefit oil-importing economies, particularly in emerging markets, more than the US, which exports oil. Last week’s tape delivered exactly that, with Asia leading the Go Global trade higher.

Here's more:

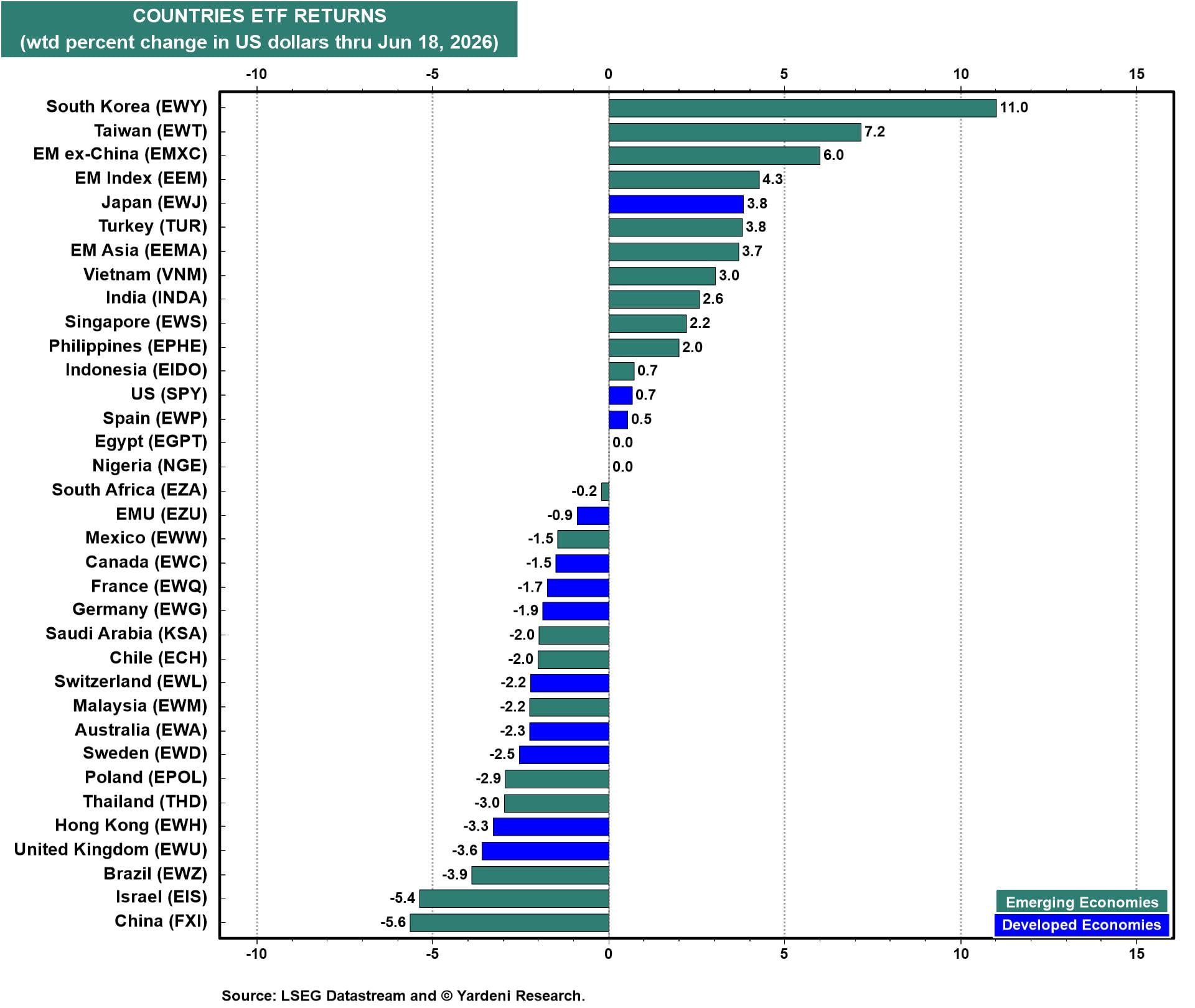

(1) Stay Home vs Go Global. EM ex-China (EMXC) dominated the week as the peace dividend filtered through to the regional names most exposed to lower energy prices and the AI capex cycle. The semiconductor trade continues to lead, which is why Korea and Taiwan sit at the top of this week's leaderboard. Korea led with an 11.0% gain for the week, with Taiwan, EM ex-China, the EM Index, Japan, and EM Asia all up between 3.7% and 7.2% (chart). External to Asia, moves were modest in either direction. The US SPY rose 0.7%, while China was the worst in the panel at -5.6%.

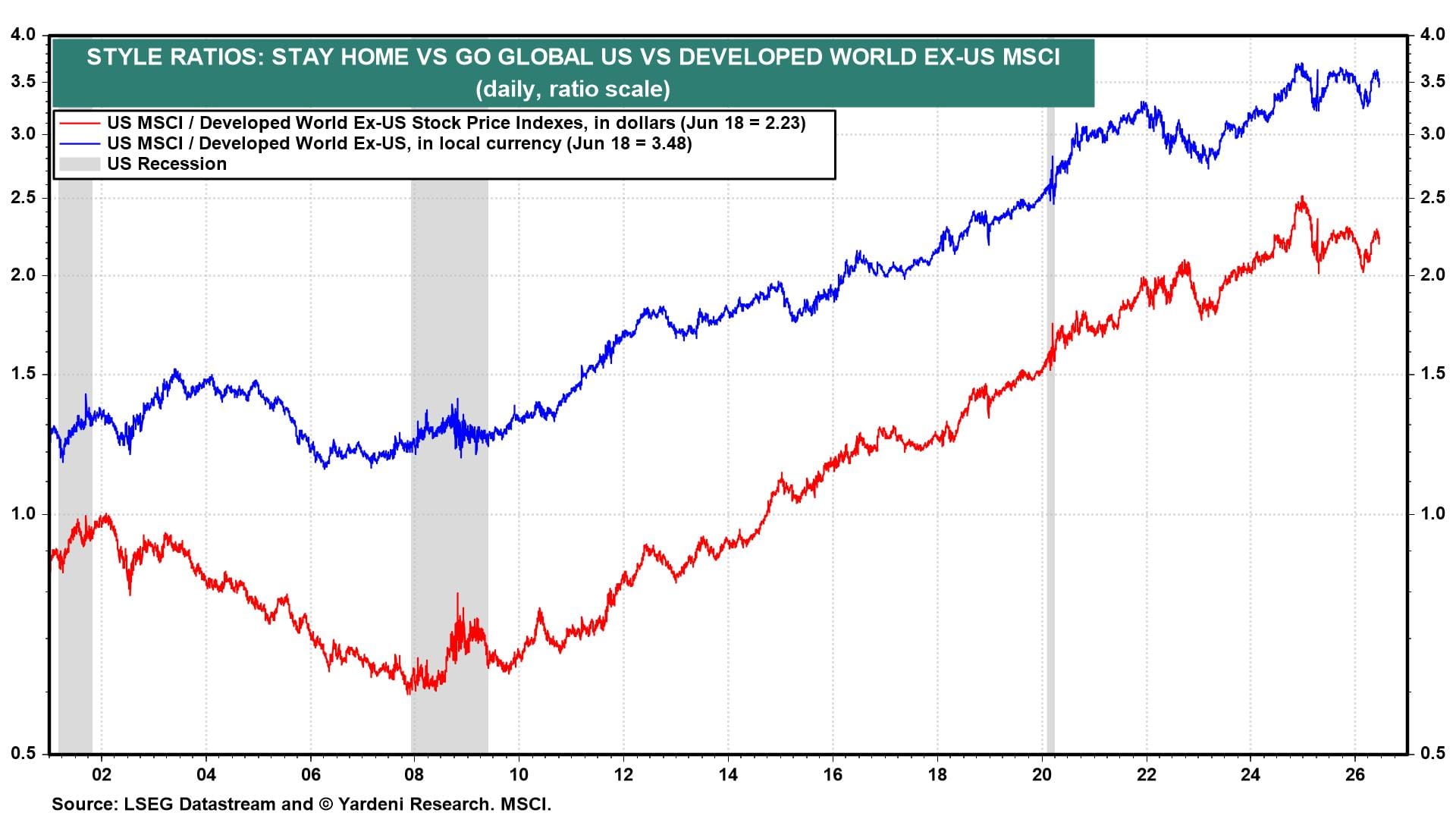

The US MSCI outperformed the Developed World Ex-US MSCI from 2010 to 2024. Since then, they have performed about the same (chart).

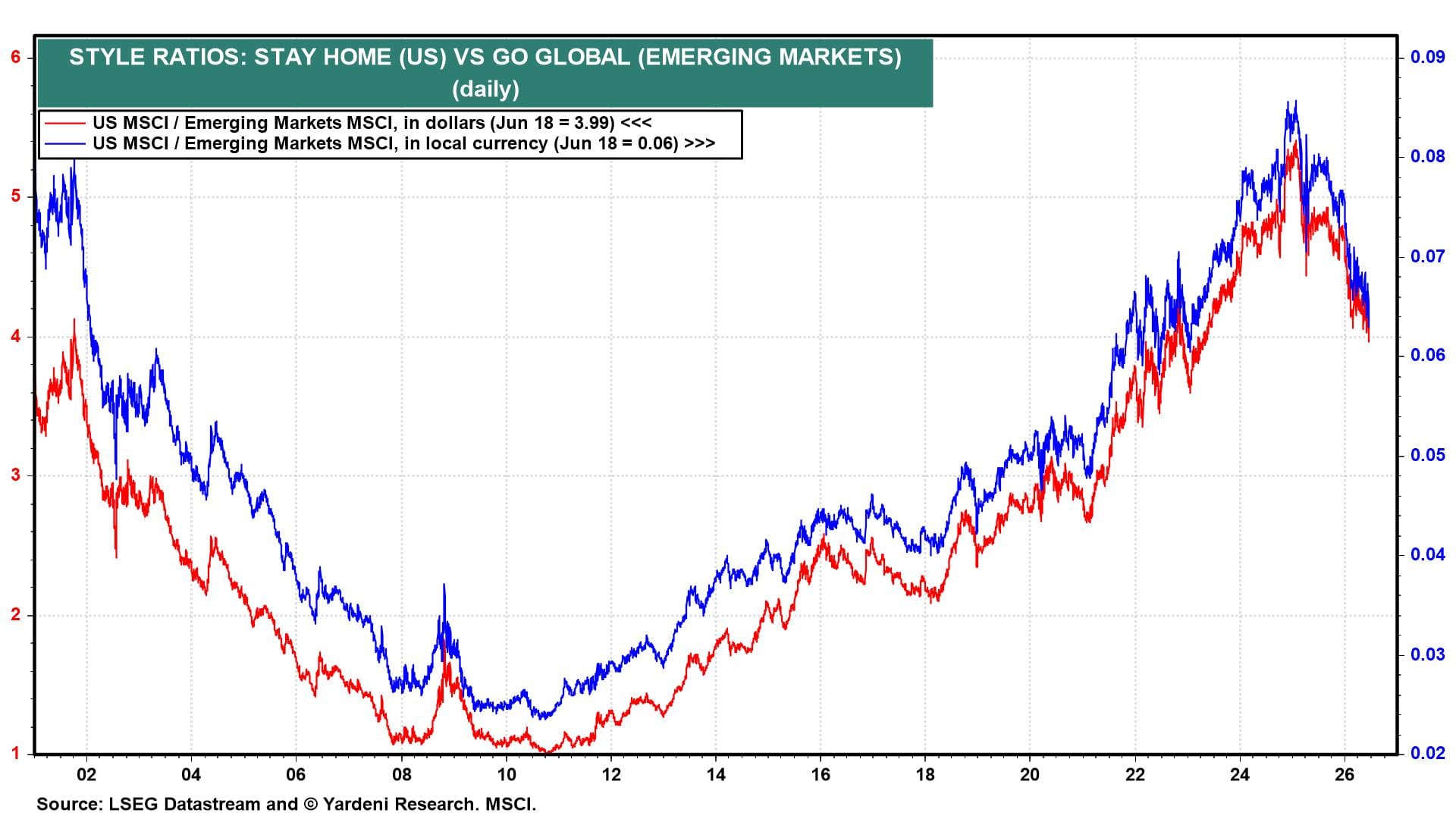

Emerging markets are doing the heavy lifting for Go Global (chart).

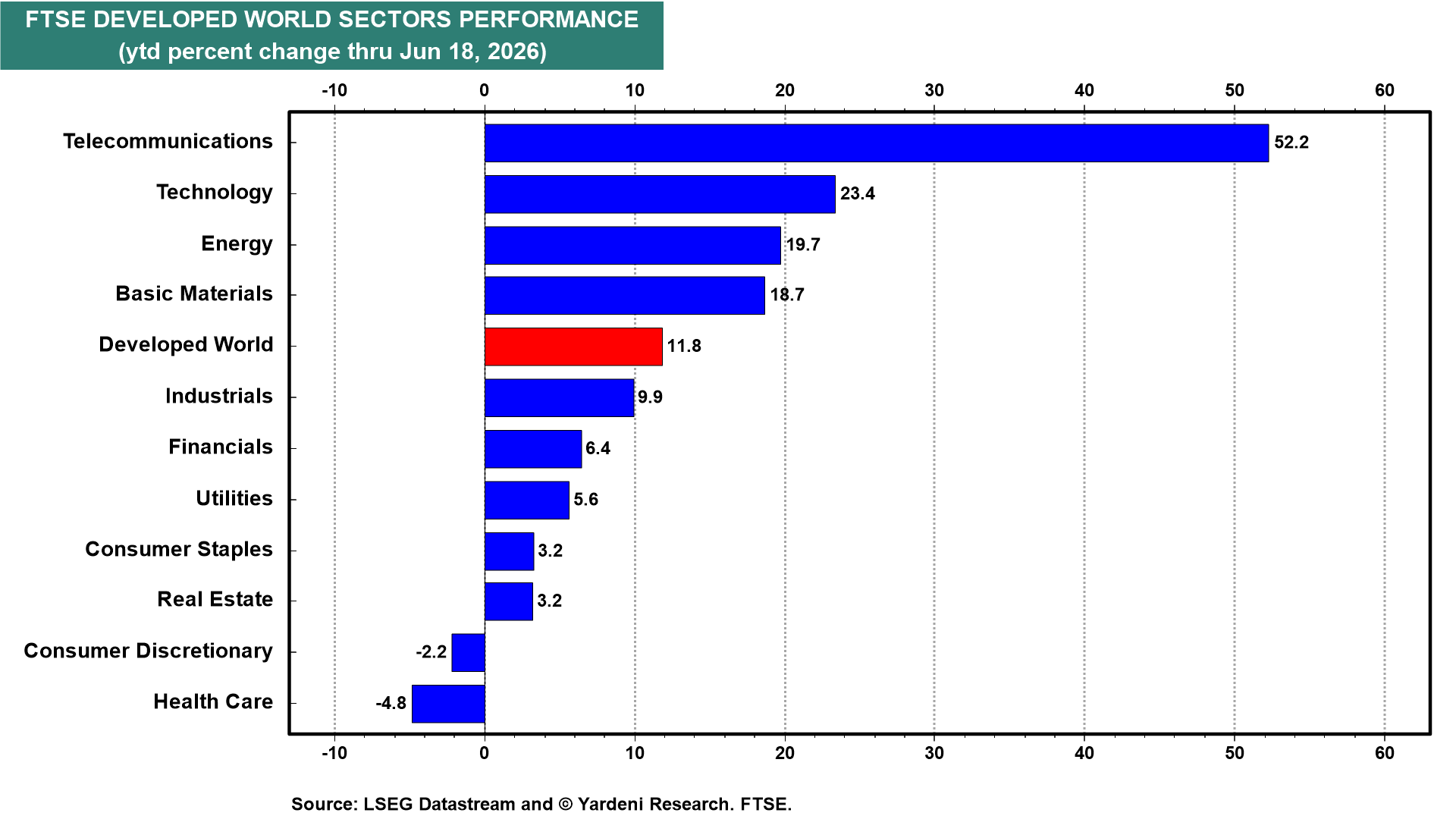

(2) Sectors. In the Developed World, Telecom is up 52.2% ytd, Tech 23.4%, Energy 19.7%, and Basic Materials 18.7% (chart).

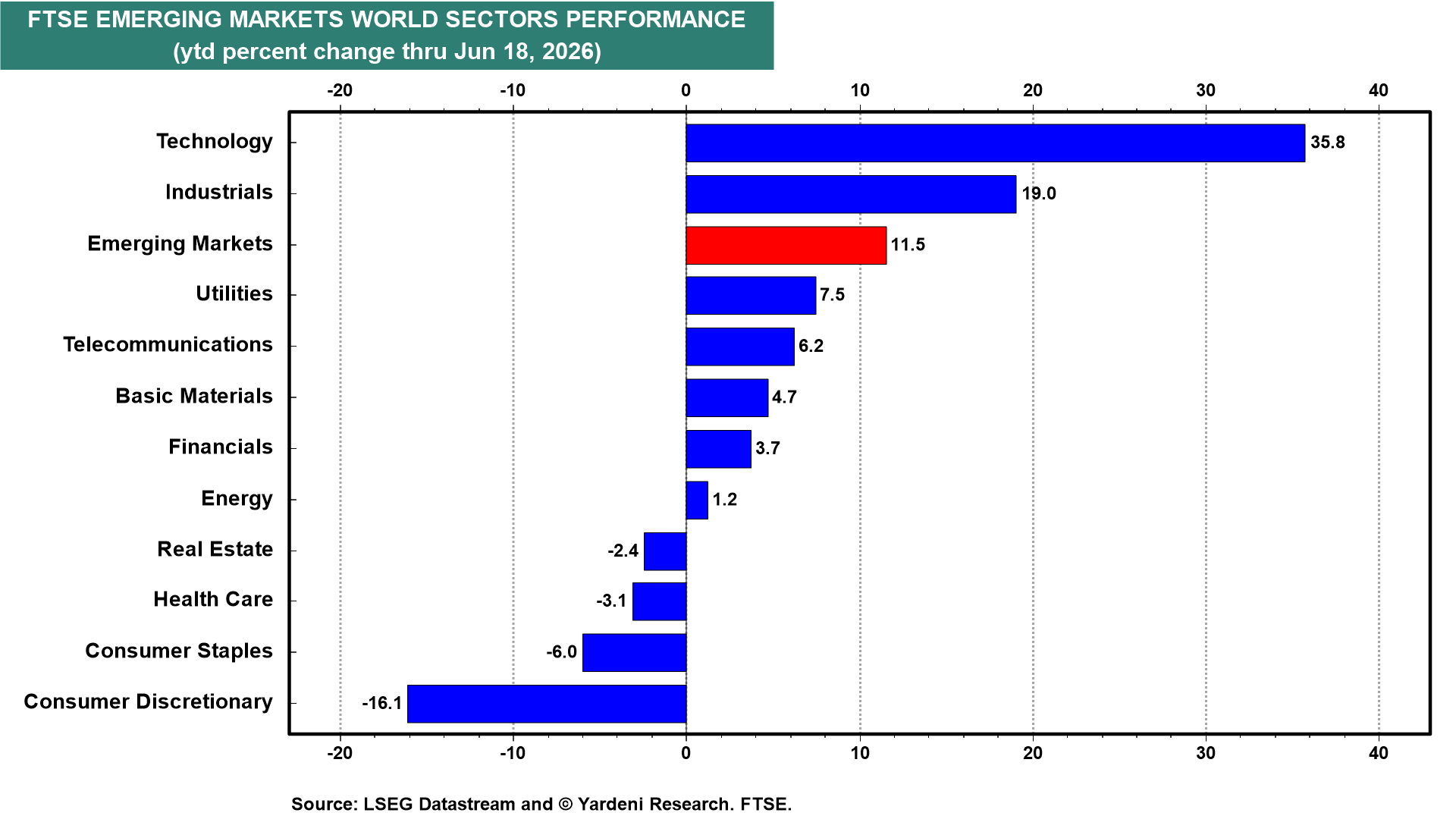

In the Emerging Markets, Tech is up 35.8% ytd, followed by Industrials, up 19.0% (charts).

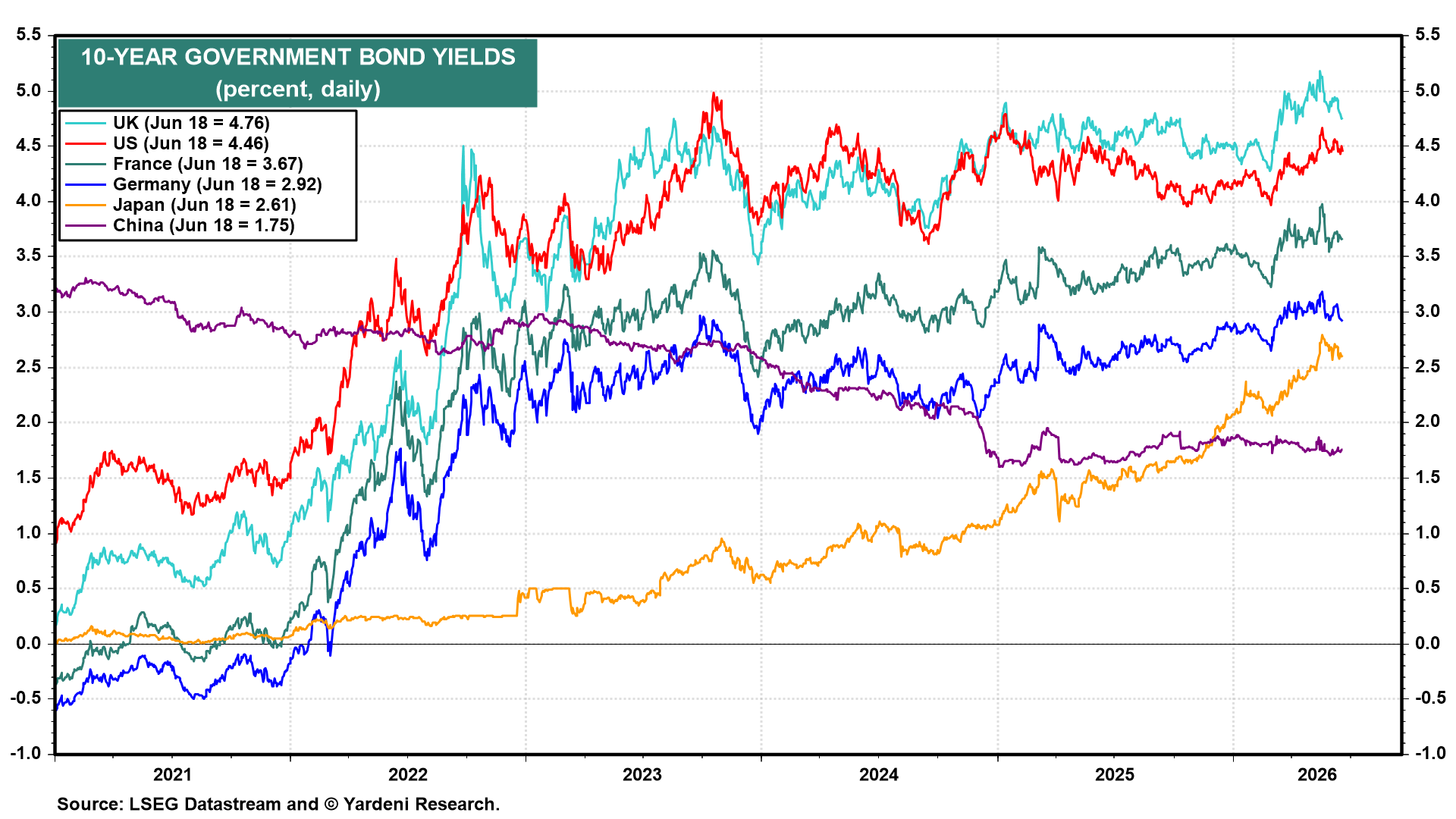

(3) Yields. Sovereign bond yields are easing on hopes that the ceasefire holds. The US 10-year is at 4.46%, down from the May peak (chart). Falling oil prices give central banks room to lean dovish where the data permit.

(4) Forex. The US dollar index rallied to 100.8 after the FOMC’s hawkish reset reinforced the rate-differential advantage in its favor (chart). Dollar strength supports the Stay Home trade at the margin and is a near-term headwind for the price of gold.

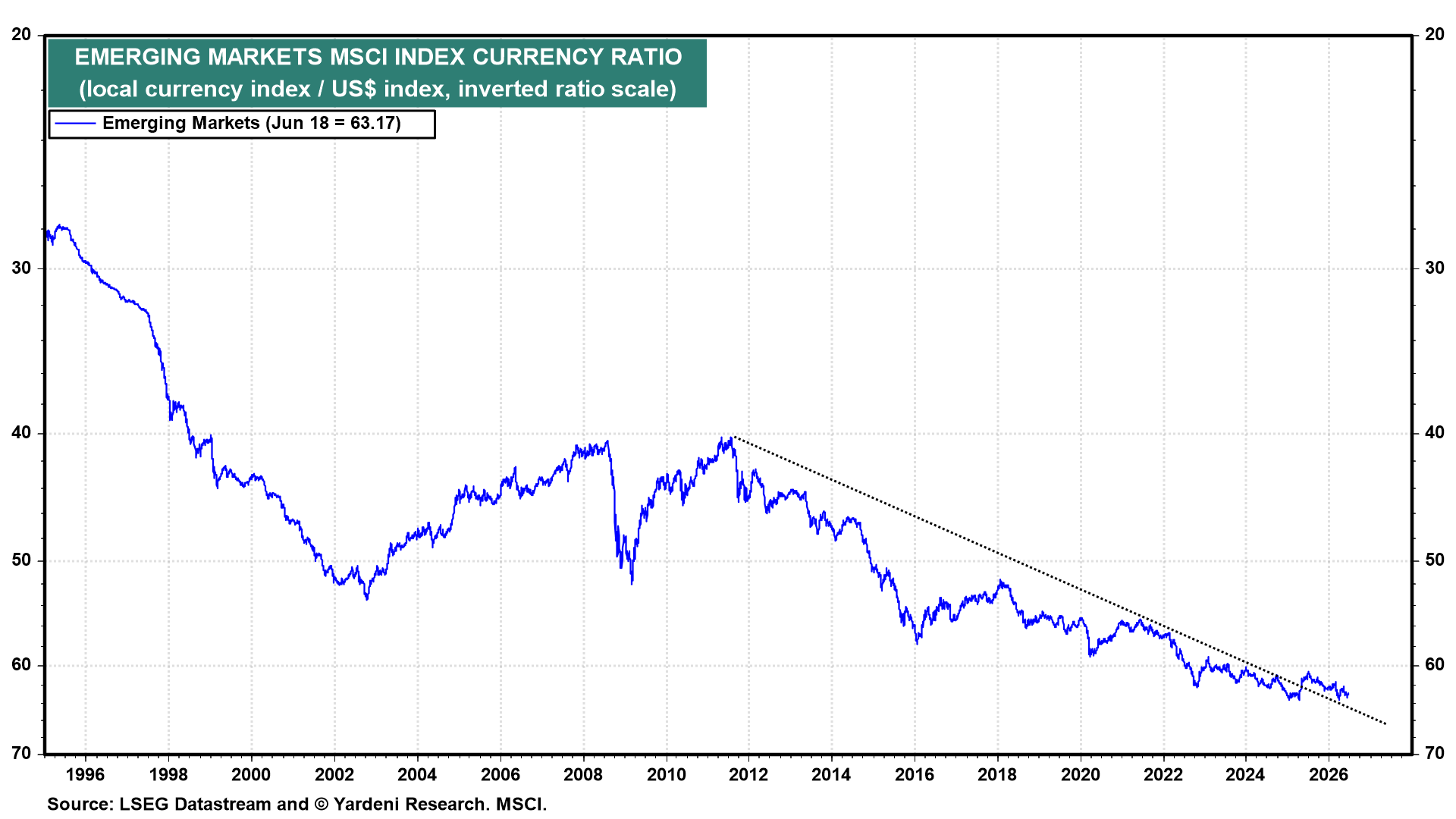

The EM MSCI currency ratio is at 63.17, still pinned near the bottom of its multi-decade downtrend (chart). EM equities are outperforming despite the currency headwind.

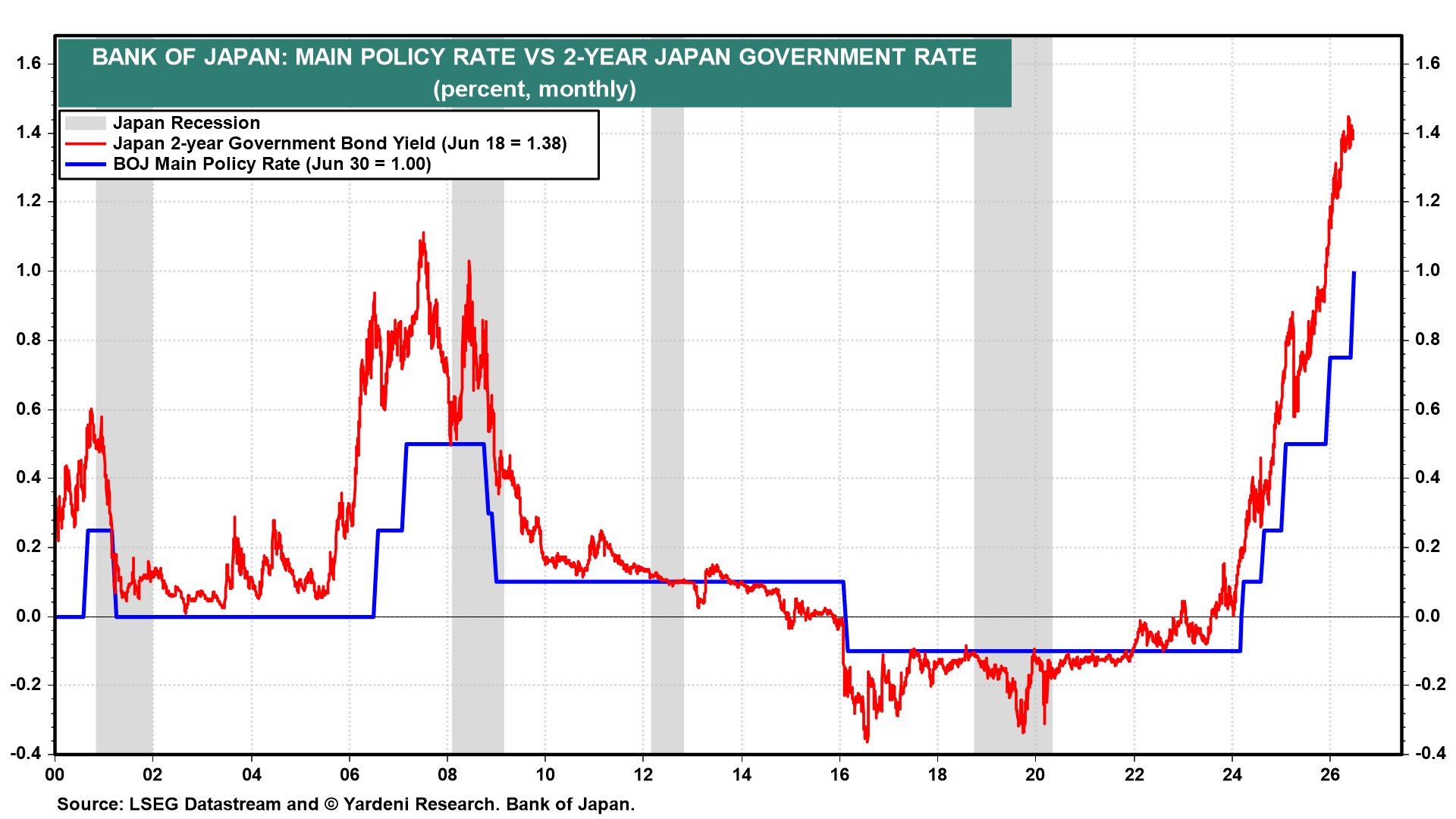

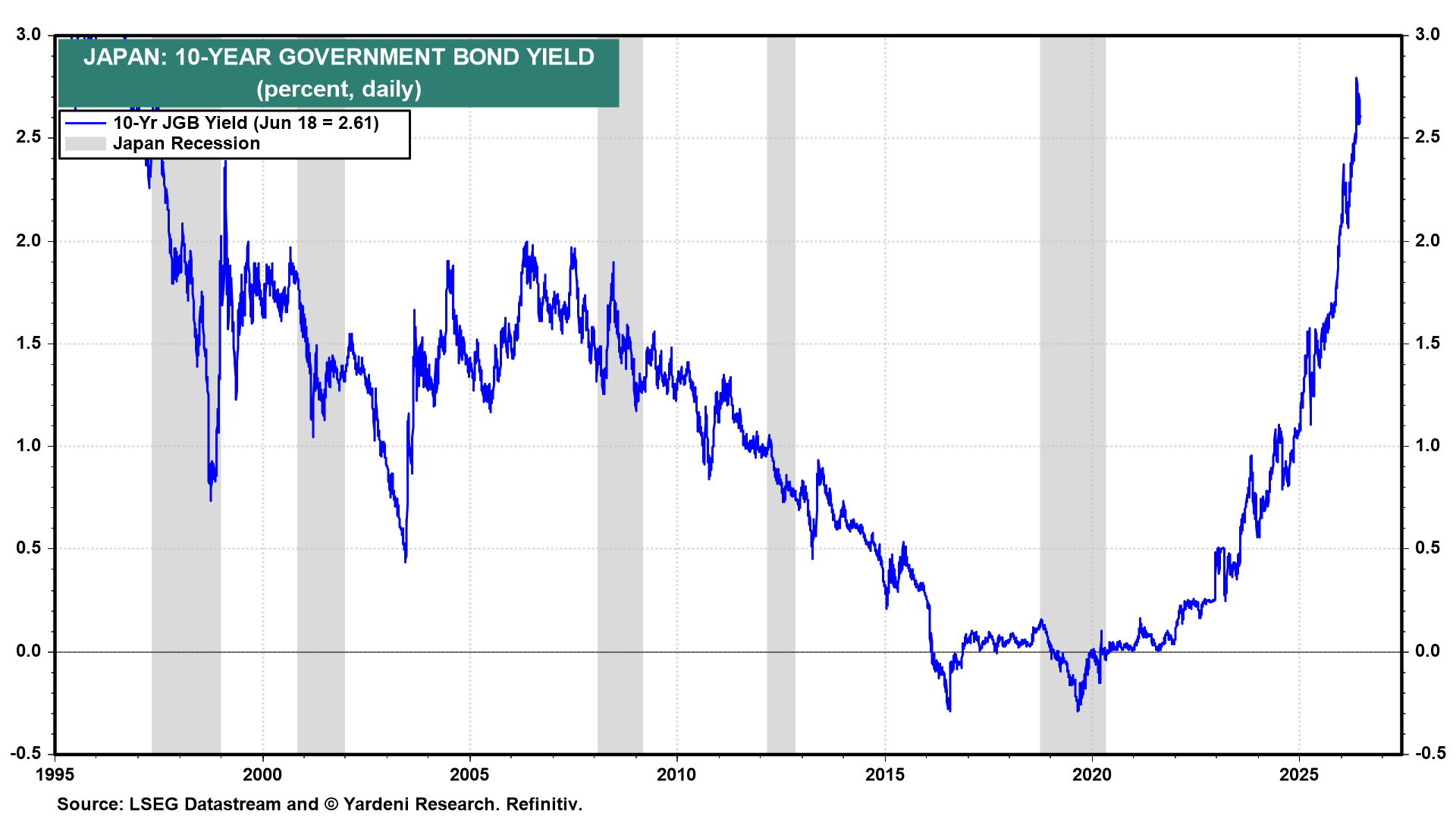

(5) Bank of Japan. Following the BOJ’s latest rate hike, the main policy rate is at 1.00%, with the 2-year JGB yield at 1.38% pricing in roughly two more hikes from here (chart).

The 10-year JGB is at 2.61%, off its recent peak but still at multi-decade highs (chart).

Yet the yen is at 160.86 against the dollar and looks ready to break through 160 despite the BOJ's tightening (chart). Intervention risk continues to surface. A weak yen is a problem that the BOJ can’t ignore much longer.

We are sticking with overweighting Go Global, with Asia ex-China leading the way.